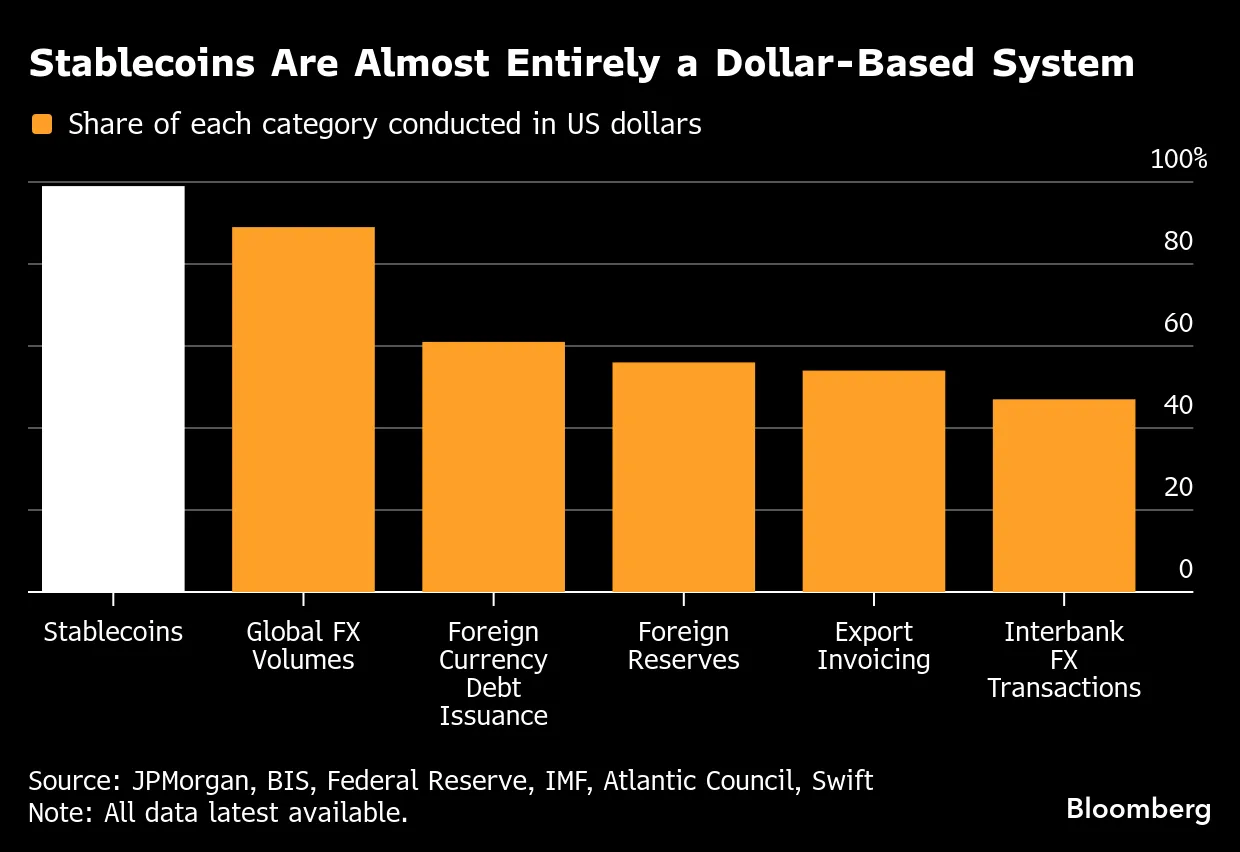

For now, the US dollar remains at the center of both traditional finance and crypto. Most stablecoins, like USDT and USDC, are backed by the dollar. In today’s crypto markets, these tokens are the main way value is measured, moved, and settled. Still, just because something is dominant now doesn’t mean it will stay that way.

Data from the IMF shows a gradual decline in the dollar’s share of global foreign exchange reserves over the past two decades, and while the dollar remains the largest reserve currency, diversification seems to be increasing. Countries are exploring alternatives not because the dollar has failed, but because reliance on a single system creates risk.

This shift, as we are witnessing here, is slow, but it is structural, and while crypto does not operate in isolation, if global finance moves toward a post-dollar economy, crypto will reflect that transition.

Stablecoins as the Transmission Layer

Stablecoins are not just digital dollars; they are the infrastructure through which value moves across crypto, and this is what makes stablecoin adoption very important. It is not just about holding value, but about settlement.

Today, more than 70% of trading on centralized exchanges uses stablecoin pairs. In DeFi, stablecoins are common for lending, collateral, and providing liquidity, so they’ve become the main way to move assets around.

If the main reference currency changes, the whole system has to adjust. The real question isn’t whether stablecoins will still matter, but what will back them. People often forget how deeply stablecoins are built into the system. They aren’t just stored in wallets; they’re always moving through liquidity pools, margin systems, derivatives, and arbitrage trades. This constant movement is what makes them so important.

In many ways, stablecoins function closer to wholesale financial infrastructure than retail money, and you will find that oftentimes, they are used by market makers to balance books across venues, by protocols to maintain peg stability, and by traders to manage exposure in real time. Remove or weaken the dominant stablecoin layer, and liquidity does not disappear; it fragments.

This is where the idea of a post-dollar economy comes in. If the main currency changes, everything built on top of it has to adjust. Pricing, collateral, and risk models all depend on the base currency. Moving away from the dollar wouldn’t just mean new stablecoins; it would mean rethinking how value is measured and moved throughout the system.

That is why stablecoin adoption is less about preference and more about coordination, and we see that the market converges on what works best for settlement. Today, that is the dollar, but tomorrow, it may not be singular.

Can Dollar-Backed Stablecoins Maintain Dominance?

Dollar-backed stablecoins have strong advantages; they benefit from deep liquidity, established trust, and integration across exchanges and protocols. USDT and USDC are already embedded in trading infrastructure, DeFi systems, and payment flows with powerful network effects, making it such that the more a stablecoin is used, the more useful it becomes.

However, these advantages depend on the continued dominance of the dollar, and in a post-dollar economy, two challenges emerge. First, geopolitical risk increases; countries may prefer settlement systems that reduce exposure to US financial oversight.

Second, diversification becomes rational, i.e, if global trade shifts toward multiple currencies, relying solely on dollar-backed stablecoins becomes inefficient. This does not mean dollar stablecoins disappear; it just means their relative dominance could decline.

What keeps dollar-backed stablecoins strong isn’t just liquidity—it’s also habit. People price risk, track performance, and manage portfolios in dollars. This creates momentum, so even if new options appear, it’s hard to switch. But this momentum fades if incentives change. If more trade settles in euros, yuan, or other currencies, demand for those stablecoins will grow, and liquidity will spread out.

There is also a structural limit to how far dollar-backed systems can expand globally because, as stablecoins grow, they begin to mirror traditional financial influence, and this increases the likelihood of regulatory pushback, especially from regions seeking monetary independence.

At the same time, competition does not need to fully displace dollar stablecoins to be impactful. Even a partial shift toward multi-currency crypto reduces their dominance and introduces fragmentation into liquidity.

This fragmentation has consequences; it changes how capital moves, how arbitrage operates, and how risk is managed. Instead of a single dominant settlement layer, the market begins to operate across multiple parallel systems, such that in that environment, the advantage shifts from scale alone to interoperability. The stablecoins that succeed will not just be the most liquid. It will be the most adaptable within a multi-currency crypto framework.

That is the real challenge for dollar-backed stablecoins, not whether they remain relevant, but whether they can remain central in a system that is no longer built around a single currency.

The Rise of Multi-Currency Stablecoin Systems

A likely outcome is that multi-currency crypto systems will grow. Instead of one main stablecoin, the market could shift to a mix of currency-backed assets, like euro-pegged, yuan-pegged, and other regional stablecoins.

We can already see this shift starting. Euro-backed stablecoins exist, even if their market share is small, and some regions are testing local currency stablecoins to support their own financial systems. The main reason is to match real-world trade flows. If global trade uses more currencies, settlement systems will follow, creating demand for multi-currency crypto solutions where users can trade in different currencies without leaving the blockchain.

Euro and Yuan Stablecoins: Potential and Constraints

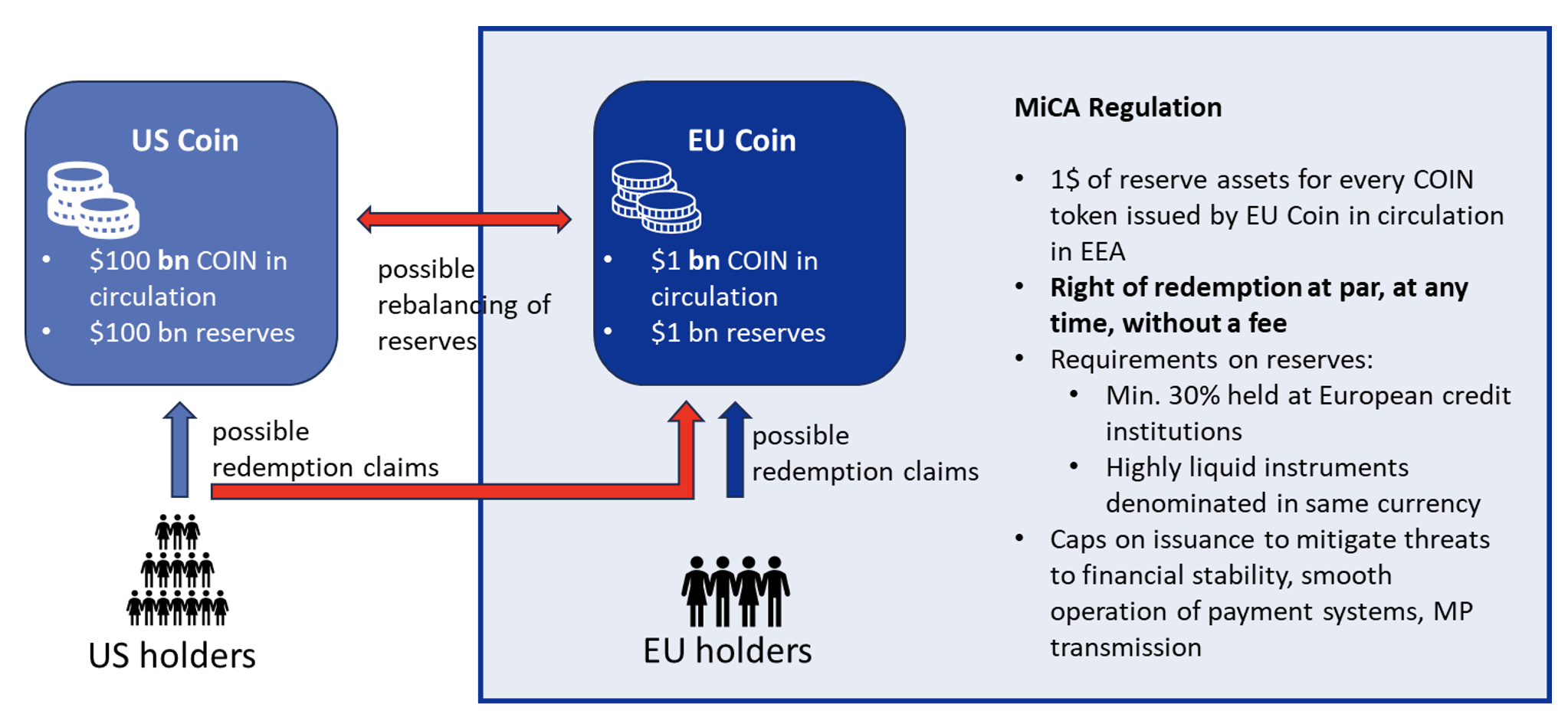

Euro-backed stablecoins have a clear use case in Europe, especially under regulatory frameworks such as MiCA. They offer compliance advantages and align with regional financial systems. However, their growth is limited by liquidity, and compared to dollar stablecoins, euro stablecoins have significantly lower trading volume and integration. Yuan-backed stablecoins face a different challenge because China has focused more on central bank digital currency development rather than open stablecoin ecosystems. The digital yuan is being tested in domestic and cross-border payments, but it operates within a controlled framework.

This creates a tension because, on one hand, yuan-based systems could gain traction in global trade, and on the other hand, their integration into open crypto markets may remain limited. This suggests that multi-currency crypto will not be evenly distributed, with some currencies scaling more effectively than others.

What is becoming clearer is that adoption will follow economic gravity rather than technological availability. The euro has regulatory clarity and institutional backing, but it lacks the global trade dominance and capital market depth that give dollar-based systems their edge. Even within Europe, much of crypto liquidity is still denominated in dollars, creating a mismatch between regulatory alignment and actual usage.

For euro stablecoins to really grow, they need more than just regulatory approval; they need to be built into trading systems, derivatives, and DeFi liquidity pools. Without this, they’ll stay important in Europe but not globally. The yuan is different. It’s becoming more important in global trade, especially through deals with other countries, but its digital setup isn’t open. The digital yuan is tightly controlled, which limits how easily it can connect with other crypto systems.

This creates a structural divide; one system is open but lacks global scale, while the other has scale but remains closed. In a post-dollar economy, this divide matters; it suggests that no single alternative will fully replace dollar-backed stablecoins, but instead, different currencies will dominate in different contexts. Euro-based systems may grow within regulated financial environments, while yuan-based systems may expand in trade corridors aligned with China’s economic influence.

The implication for multi-currency crypto solutions for global trade is that fragmentation is not just likely, it is inevitable, and liquidity will tend not to converge around a single alternative. It will be distributed across multiple systems, each shaped by its own regulatory and economic constraints.

The Case for Currency Baskets

Another interesting possibility is basket-backed stablecoins. Instead of being linked to just one currency, these assets could be backed by a mix of currencies or even real-world assets. This would reduce reliance on any single monetary system.

Historically, this concept is not new; the IMF’s Special Drawing Rights function as a basket of currencies used for international reserves, and a crypto-native version of this model could emerge as a neutral settlement layer. For the future of digital payments in a post-dollar world, this model offers stability through diversification. However, it also introduces complexity because managing reserves across multiple currencies requires transparency, governance, and trust, and without these, adoption will be limited.

Beyond complexity, there is also the question of incentives; basket-backed systems are neutral by design, but neutrality can slow adoption. Market participants tend to prefer assets that align with their existing exposures. A trader operating in dollar markets prefers dollar-denominated assets, and a company trading in euros prefers euro stability. A basket sits in between, which makes it theoretically stable but practically less intuitive, and this creates a coordination challenge because for a basket-backed stablecoin to scale, multiple participants must agree on its usefulness at the same time. Without that shared adoption, liquidity remains thin, and thin liquidity undermines stability.

There is also the issue of governance; unlike single-currency stablecoins, basket systems require decisions about composition, weighting, and rebalancing. These decisions introduce a layer of human or institutional control that must be trusted because if governance is unclear or centralized, it weakens the very neutrality the system aims to provide.

At the same time, the long-term case for basket-backed assets remains strong, and as global finance becomes more multipolar, a neutral unit of account becomes more valuable. A well-designed basket stablecoin could reduce currency risk, smooth volatility across regions, and provide a common settlement layer for multi-currency crypto ecosystems.

In that sense, basket-backed systems are less about replacing existing stablecoins and more about complementing them. They could emerge as a higher-level settlement layer, sitting above individual currency stablecoins and enabling more efficient cross-border flows.

The idea of how stablecoins will respond to a declining US dollar becomes more concrete here, as the response is unlikely to be a single shift from one currency to another. It is more likely to be an expansion into multiple layers, where dollar, euro, yuan, and basket-backed systems coexist and interact. The challenge is aligning incentives, liquidity and trust at scale, and that is what will ultimately determine whether basket-backed stablecoins remain theoretical or become a core part of the future of digital payments in a post-dollar world.

Crypto-Native Settlement Systems

Beyond fiat-backed models, another possibility is that crypto-native assets could serve as settlement layers. Assets like Bitcoin or Ethereum are not tied to any national currency because they operate independently of traditional financial systems. This makes them attractive in a post-dollar economy scenario.

However, volatility remains a major constraint because, for settlement, stability is critical, and while crypto-native assets are valuable for storing value or securing networks, their price fluctuations limit their use as a primary medium of exchange. That said, hybrid models could emerge; for example, stablecoins could be backed partially by crypto assets or use algorithmic mechanisms to maintain stability.

These systems aim to combine decentralization with stability, though past failures have shown how difficult this is to execute.

Regulation Will Shape the Outcome

Regulation is a key factor in determining which models succeed, as Dollar-backed stablecoins are already under scrutiny. Governments are focusing on reserve backing, transparency, and systemic risk, and in Europe, MiCA is setting clear rules for stablecoin issuance. In the United States, discussions around stablecoin regulation continue to evolve.

In a post-dollar economy, regulatory alignment becomes even more important, and multi-currency systems will need to navigate multiple jurisdictions. This adds complexity but also creates opportunities for compliant innovation, and in the coming months, we will find that regulation will shape the structure of stablecoin adoption.

DeFi Will Accelerate the Transition

DeFi plays a critical role in this transition as it provides the infrastructure for multi-currency crypto solutions for global trade, and through decentralized exchanges, lending protocols, and aggregation platforms, users can move between different assets without relying on centralized intermediaries.

This makes it easier to adopt new stablecoins because if euro or yuan stablecoins gain traction, DeFi can integrate them quickly. Liquidity pools, yield strategies, and trading pairs can adapt in real time, and this flexibility is a key advantage.

This means the transition to a multi-currency crypto system can happen faster than in traditional finance.

Liquidity Will Determine Winners

In the end, the success of any stablecoin depends on liquidity. Users want assets that are easy to trade, widely accepted, and well integrated. Dollar-backed stablecoins lead now because they fit these needs. For other options to compete, they need similar liquidity.

This is not particularly easy because liquidity is not just about supply; it is about trust, infrastructure, and network effects. This is why the transition to a post-dollar crypto economy will likely be gradual rather than sudden.

What makes liquidity so difficult to replicate is that it compounds over time, and deep liquidity attracts more users, more users attract more integrations, and more integrations reinforce liquidity. This feedback loop is what has allowed dollar-backed stablecoins to entrench themselves across both CeFi and DeFi, and breaking that loop requires not just a better product, but a coordinated shift in behaviour across the entire market.

Even if a euro- or yuan-backed stablecoin has strong regulatory or institutional support, it still faces a cold-start problem. Market makers need reasons to provide liquidity. Exchanges need incentives to list and prioritize these pairs, and DeFi protocols need to add them to lending, collateral, and liquidity pools.

Instead of a single dominant pool of liquidity, capital may begin to split across several stablecoin systems. This shows a more diverse global economy, but it also adds friction. Cross-currency swaps get more complicated, spreads get wider, and capital becomes less efficient unless systems for working across currencies get better.

Another key factor is composability, because liquidity in DeFi is not static. It is reused, rehypothecated, and layered across protocols. Stablecoins that integrate seamlessly into this composable stack gain an advantage, and those that do not remain siloed, regardless of their underlying backing.

Trust also plays a central role; liquidity follows credibility because transparent reserves, reliable redemptions, and consistent peg stability are non-negotiable. Any instability, even temporary, can trigger rapid outflows and permanently damage adoption.

In this sense, liquidity is both a technical and psychological construct that reflects not just how much capital is available, but how confident participants are in using it. The implication is clear: the winners in a post-dollar economy will be the ones that can build, sustain, and defend liquidity at scale.

The Most Likely Outcome

The most likely outcome isn’t replacement, but expansion. Dollar-backed stablecoins will stay dominant for now, but their market share may drop as new systems appear. At the same time, multi-currency crypto will keep growing.

Different regions, industries, and use cases will choose different settlement assets, making the system more diverse. For digital payments in a post-dollar world, this means greater flexibility but also greater complexity.

The move toward a post-dollar economy is slow, but it’s already affecting global finance. Crypto isn’t separate from this change; it’s part of it.

Stablecoin use will keep growing, and over time, dollar-backed models will face more competition from multi-currency systems, basket-backed assets, and crypto-native options. There won’t be just one winner. Instead, several types of money will exist together on-chain, and that’s where the data suggests things are heading.

If that is the case, the real question isn’t whether the dollar loses its crown but what replaces it. Will it be one new system, or a whole new structure built on multi-currency crypto?

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this piece? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

“Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}