Quick Breakdown

- Over 80% of UK 16- to 25-year-olds know about cryptocurrencies, with Bitcoin more recognized than ISAs or savings bonds, showing a “crypto first, TradFi second” shift.

- Government restrictions, like banning crypto political donations, combined with complex rules, create a potential clash between high youth demand and tightening UK crypto regulations.

- Simplified regulated entry points, clear guidance, education, fintech-regulator partnerships, and incentives can convert enthusiasm into safe, lawful adoption, but only if designed to match how young people engage with crypto.

Crypto is becoming very familiar to young people in the UK. Over 80% of 16- to 25-year-olds now know about digital assets like Bitcoin and Ethereum. For many, crypto is their first real introduction to money, investing, and taking financial risks, rather than traditional banking products.

Awareness of traditional financial products like Individual Savings Accounts (ISAs) remains relatively low among young people in the UK, while interest in crypto continues to rise. This suggests that many young people may be encountering financial concepts through newer digital assets before fully understanding traditional finance.

Yet this enthusiasm faces a potential roadblock: tightening UK crypto regulations aimed at protecting democracy, investors, ensuring compliance, and maintaining market stability.

A critical question then emerges: can this high level of interest among youth actually translate into crypto adoption, or will regulatory challenges slow the next generation’s participation in the digital assets market?

Crypto, Youth, and Politics: Navigating a New Regulatory Environment

Coinbase’s VP of international policy, Tom Duff Gordon, noted that the UK is “sitting on an estimated 1.3 million new voters” as plans move forward to lower the voting age to 16. He noted that crypto is quickly becoming a topic that political parties need to address.

Research shows that young people care about crypto in politics: nearly half said they would trust a party more if it understood crypto and blockchain, and 26% said they were more likely to support a party that backed pro-innovation crypto policies.

Among under-25s, Bitcoin is now more widely recognized than any ISA, savings bond, or other traditional savings product, with 65% awareness making it the most familiar financial product in this group.

At the same time, the UK is taking action to limit crypto’s political influence. The government has banned crypto donations to political parties, with Secretary of State Steve Reed saying:

“This Government will do whatever is necessary to protect our democracy. Foreign interference and dirty money are menacing the integrity of our elections. A ban on cryptocurrency donations is vital. The UK will now be a world-leader in stamping out this growing threat to freedom, and we will stop hostile foreign states and others who want to weaken and exploit the UK by stoking division and hatred. It is our patriotic duty to safeguard the British people’s right to freely choose their own government.”

That puts crypto policy on a potential collision course with the current donations moratorium and could lead to a demand-regulation clash.

Bridging the Gap: Aligning Youth Crypto Demand with Regulation

As UK youth show soaring interest in digital assets, the challenge is converting awareness into safe, legal crypto adoption that works within the country’s tightening regulatory framework.

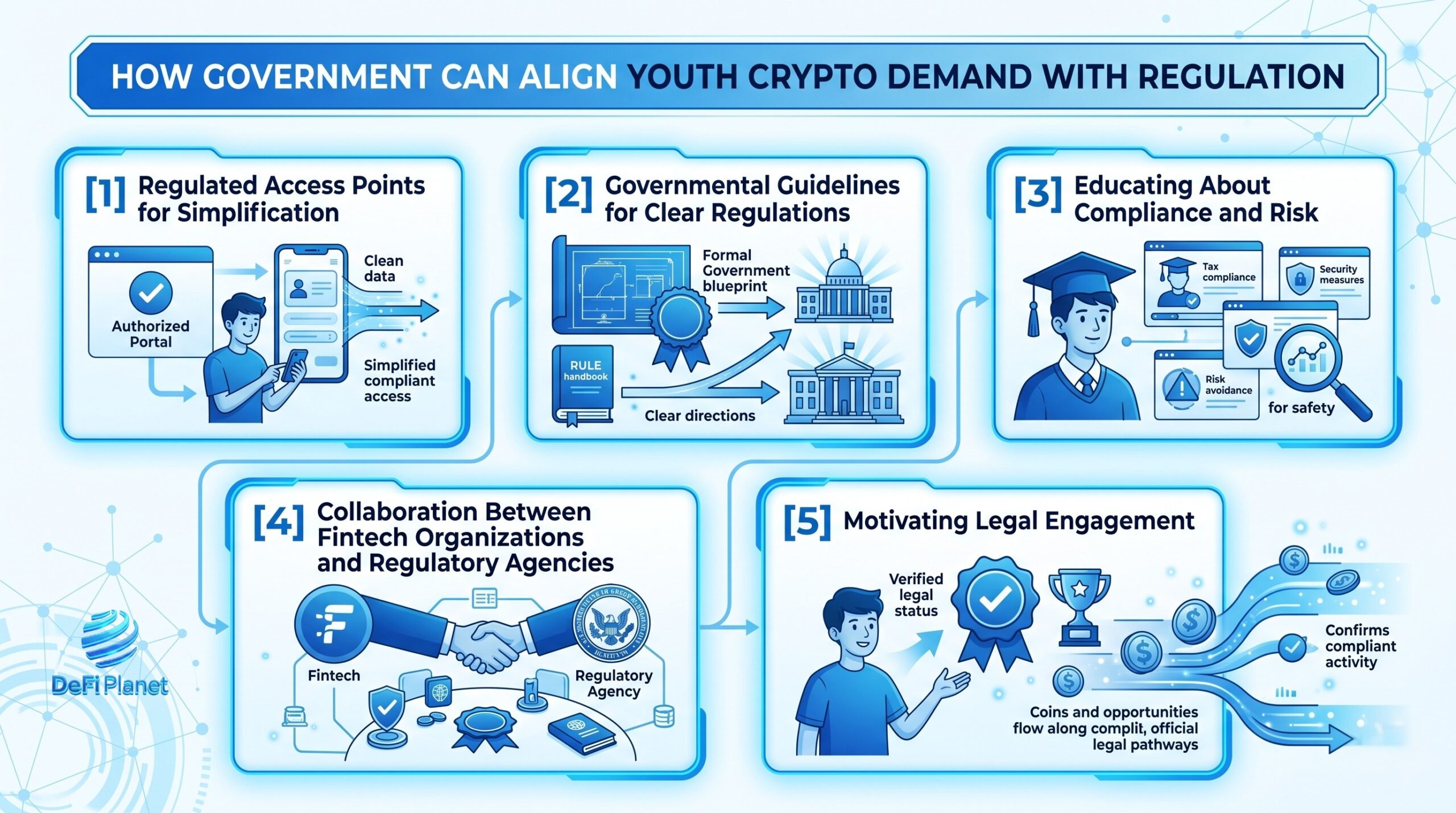

Regulated access points for simplification

The primary issue most youth face is the element of complexity. The traditional crypto wallets and exchange accounts might seem intimidating for them, and the legal aspects create another layer of difficulty. Providing FCA-regulated wallet services or exchange-traded funds would give youth access to the market in a regulated way.

These products handle all security, storage, and regulatory considerations, and the young investors can then concentrate their efforts on learning about cryptocurrency and its investment opportunities.

Governmental guidelines for clear regulations

Crypto regulations might be confusing to the youth, which makes them wary of following the law. The government can provide some much-needed clarity by formulating straightforward guidelines regarding trade activities, KYC requirements, and cryptocurrency-based politics.

These guidelines will give the platform providers a framework to offer a regulated product, and the investors will be made aware of their rights and responsibilities.

Educating about compliance and risk

Schools, universities, and other institutions should inform children about cryptocurrency trading in accordance with UK laws, including taxes and anti-money laundering procedures.

Learning about the importance of compliance and proper investment behaviour will allow young people to act responsibly and build their bridges between theory and reality.

Collaboration between fintech organizations and regulatory agencies

Innovation should not necessarily contradict regulations. Collaborations among fintech organizations, banks, and regulatory agencies could produce pilots and sandbox projects that would enable youth to legally invest and learn.

Motivating legal engagement

Youngsters will likely engage if there is something they can gain from it. The use of tax benefits, rewards programs, and easier access to regulated cryptocurrency will help incentivize youngsters to become involved. The incentives offered motivate them to act in accordance with the guidelines laid down.

Can These Solutions Really Bridge the Demand-Regulation Gap?

The recommendations present a framework for turning the interest of the UK’s youth in cryptocurrency into safe and legal crypto adoption. However, are they sufficient to reconcile the gap between the high level of demand and more stringent regulation?

Using regulated products like FCA-approved wallets and ETFs gives the young the possibility to safely and legally trade cryptocurrencies. Even if regulated products are easier to use than privately managed wallets and exchanges, they depend on the accessibility and attractiveness of those products. Otherwise, some of them will switch back to unregulated products.

Regulatory guidelines can reduce the uncertainties, but only when they are effectively communicated. In case they are difficult to understand, outdated, or not clear, they might act as barriers. For that very reason, the regulators need to collaborate with the educational sector, fintech players, and social media platforms.

Collaboration between fintech and regulators represents an ideal compromise. Sandbox programs let youth experiment safely, building confidence in legal channels. However, these efforts need to be scaled up fast enough to keep up with demand; otherwise, they might remain niche and fail to compete against non-regulated services.

Incentives may help with crypto adoption, but they are not a solution. Incentives will be most effective if attached to real value, such as loyalty points for increased investment or tax breaks. Small, temporary incentives may not be enough to beat the allure of unrestricted platforms.

These approaches can resolve the dilemma of demand versus crypto regulations, provided that they are employed correctly in relation to cryptocurrency usage among younger generations. In case they are not applied correctly, the hype will continue to be held back by the regulations.

Is a Demand-Regulation Clash Inevitable in the UK?

The test of the UK crypto atmosphere will be determined by how young people utilize legal and regulated platforms for investment purposes. Simply increasing crypto awareness will not be enough. The key will be the appeal, accessibility, and competitiveness of such opportunities compared to unregulated methods.

Ultimately, a demand-regulation dilemma need not occur, but it is still possible. Yet the conclusion to be drawn is that through coordination and effective strategy, the UK can avoid such an issue from developing.

If done well, it is possible for a high demand level to result in a market that achieves both innovation and regulation, thus circumventing the problem altogether.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this piece? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.”