Quick Breakdown

- Stablecoins are now widely used for payments and settlements, and transaction volumes reached $33 trillion in 2025, which is attracting major players like Stripe, Visa, Mastercard, PayPal, and Western Union into the space.

- Traditional payment companies have advantages in global reach, user trust, and regulatory compliance, giving them a strong position as they build stablecoin-based systems on top of existing financial networks.

- However, their growing involvement also raises concerns about centralization, reduced competition, and possible control over transaction flows, which could reshape how open and permissionless stablecoin systems remain in the future.

In 2025, stablecoins reached $33 trillion in transaction volume, an impressive +72% YoY. Something interesting is happening. Traditional payment giants are getting into the space and beginning to leverage blockchain technology for settlement. Western Union is testing blockchain-based settlement systems to find faster, cheaper ways to move money globally. Stripe has acquired Bridge to improve stablecoin adoption for businesses.

Mastercard is building out its own infrastructure strategy through its planned acquisition of BVNK to connect blockchain rails with traditional banking systems, while Visa has already settled over $225 million in stablecoin volume. PayPal has launched its own stablecoin, PYUSD, which is now integrated into payments across its wallet and merchant network.

These moves raise a key question: are traditional payment giants about to dominate the stablecoin market?

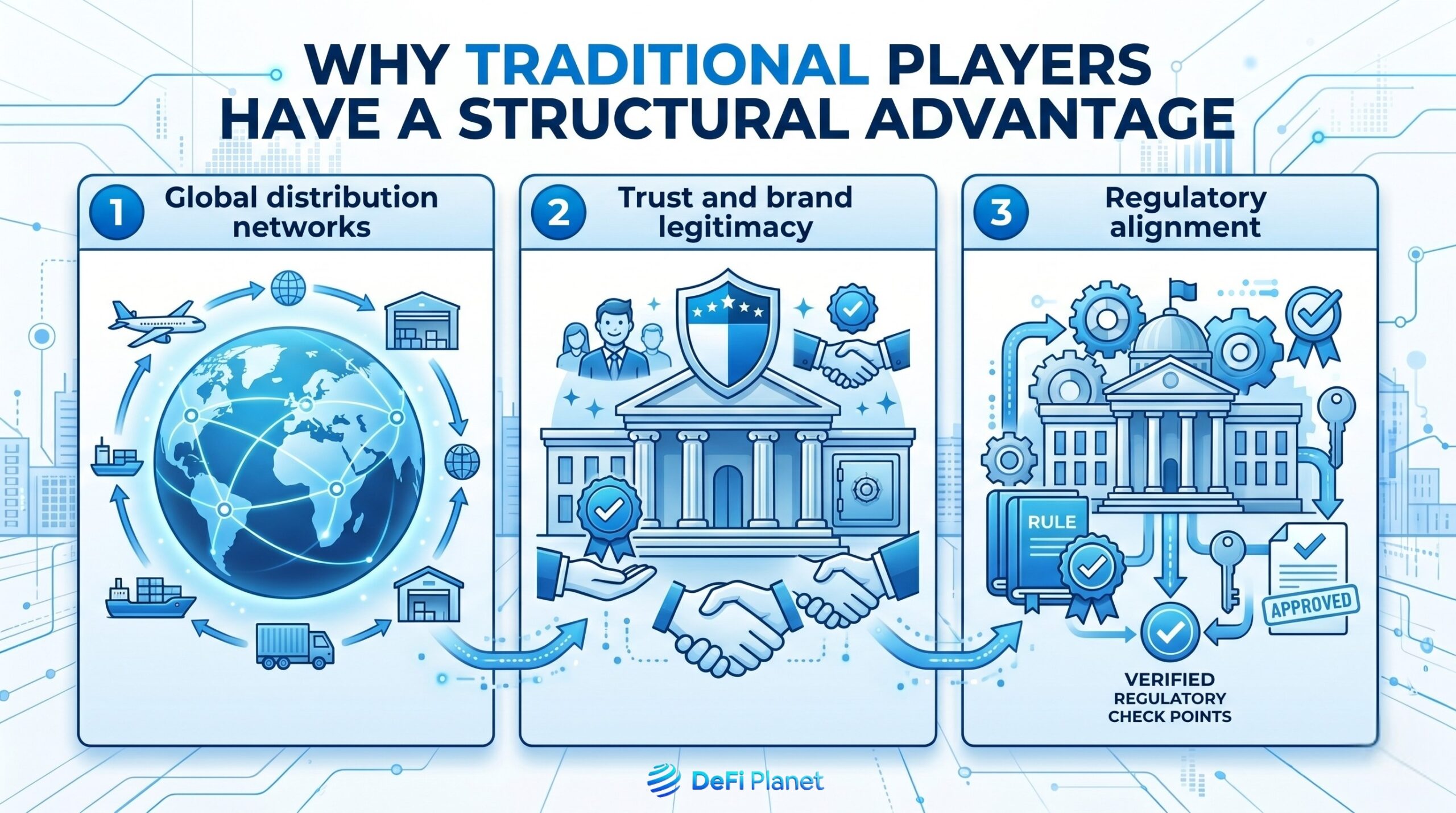

Why Traditional Players Have a Structural Advantage

These traditional payment fintech companies aren’t just adopting stablecoins randomly. They are adopting from a place of built-in advantages that come from years of operating global financial systems, strong trust, and close relationships with regulators.

Global distribution networks

Fintech companies already have payment systems that work across hundreds of countries. They are connected to millions of merchants and billions of users through cards, remittance services, and payment rails. This gives them instant reach, while new crypto-native firms usually have to build their networks from scratch.

Trust and brand legitimacy

People are generally more comfortable using well-known financial brands that are regulated and established. Companies like banks and major payment processors are seen as safer, especially for moving large amounts of money. In contrast, crypto-native platforms often face more skepticism from everyday users.

Regulatory alignment

Traditional players already follow strict rules around identity checks, anti-money laundering (AML), and financial reporting. Because of this, they can work more easily with governments and banks when launching new products like stablecoin payments. Crypto-native firms often need extra steps to meet the same standards.

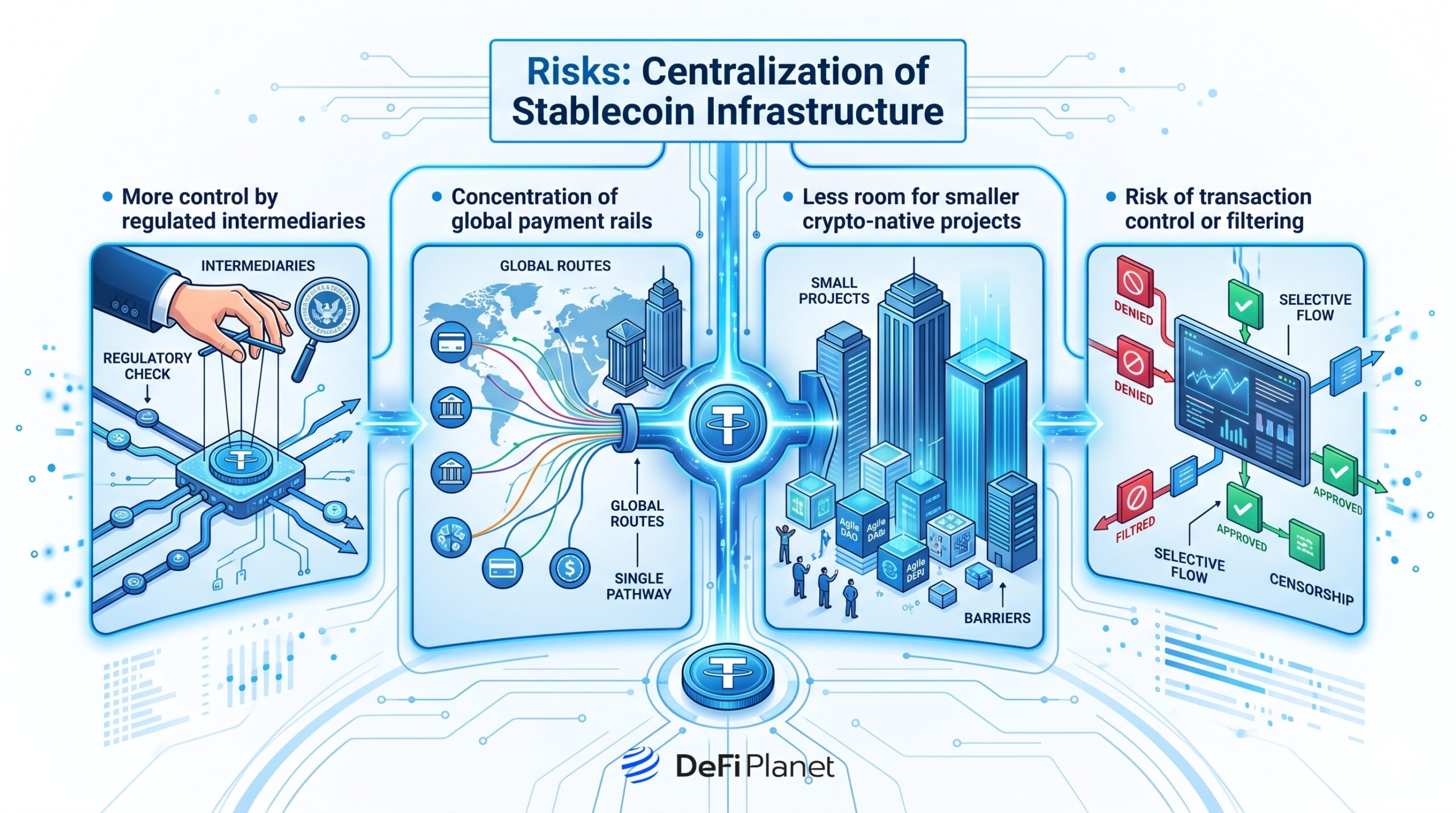

Risks: Centralization of Stablecoin Infrastructure

As traditional payment giants adopt stablecoins, control of the system may move away from open crypto networks and into the hands of a few large, regulated companies.

More control by regulated intermediaries

Instead of stablecoins being issued and managed across decentralized crypto systems, more activity could shift to large fintech companies. This means fewer independent players and more reliance on a small group of regulated institutions. This reduces the open nature of how stablecoins were originally designed to work.

Concentration of global payment rails

If a few large companies control the most stablecoin payment infrastructure, they could end up becoming the main channels through which money moves globally. This can make the system more efficient, but it also reduces competition and spreads control into fewer hands. Over time, this could make it harder for new users to build alternative payment networks.

Less room for smaller crypto-native projects

Smaller crypto companies may struggle to compete with large firms that already have users, capital, and regulatory approval. This could slow down innovation in the broader crypto ecosystem. It may also push smaller teams to rely on partnerships rather than build independent systems.

Risk of transaction control or filtering

Regulated companies may be required to block or restrict certain transactions based on laws or compliance rules. While this improves regulation, it also introduces the possibility of censorship or limits on how freely money moves. This could change how “permissionless” stablecoin adoption and usage feel in practice.

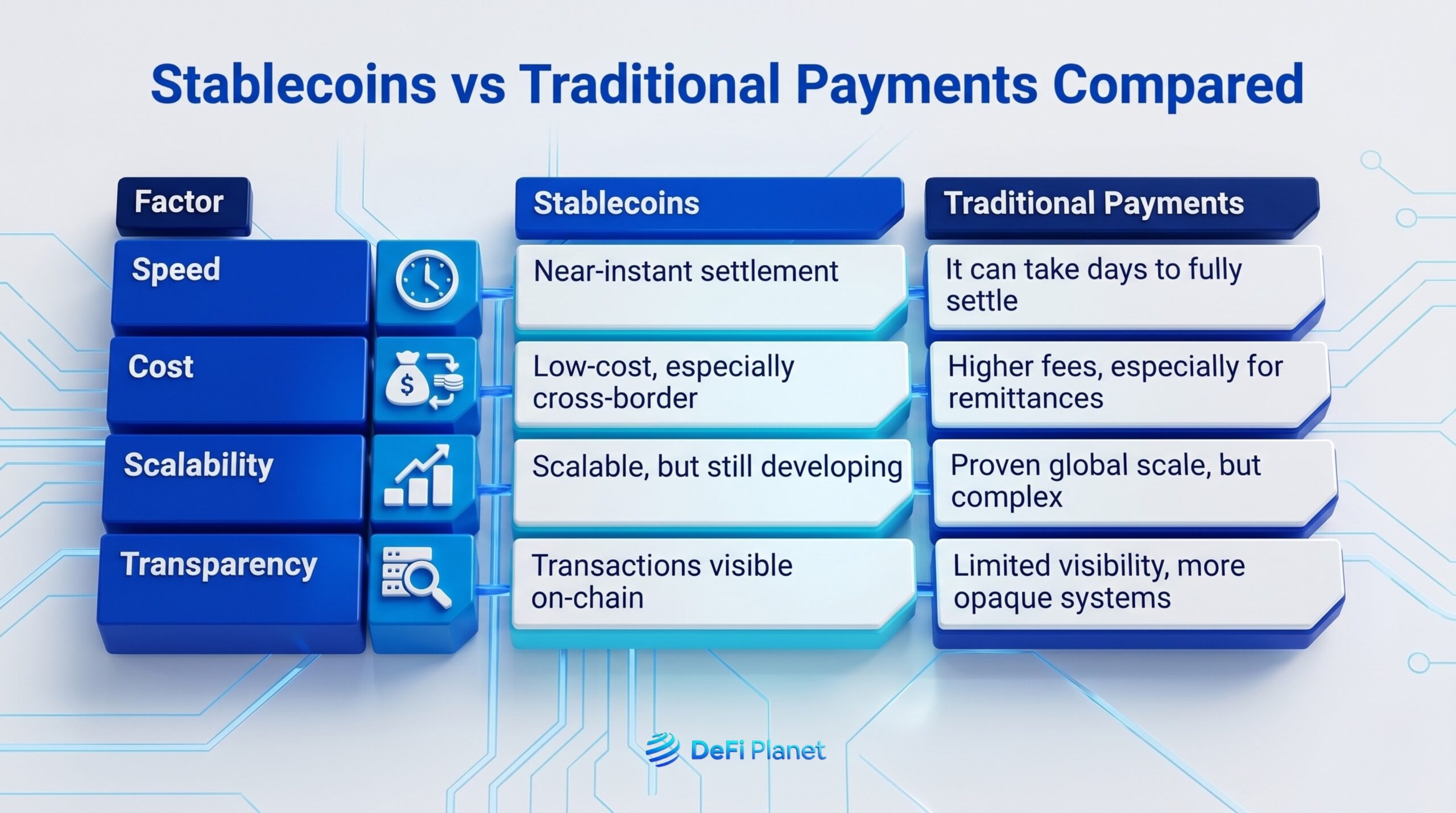

Stablecoins vs Traditional Payment Systems

Stablecoins and traditional payment systems move money in very different ways, and each has clear strengths and weaknesses depending on speed, cost, scale, and transparency.

Speed

Stablecoins can move money almost instantly because transactions are processed on blockchain networks without waiting for multiple intermediaries. Traditional systems often take longer because payments pass through several banks and clearing systems before they are fully settled.

Cost efficiency

Sending money with stablecoins is usually cheaper, especially across borders, because fewer middlemen are involved. Traditional payment systems often include multiple fees, which can make transfers, especially international ones, more expensive.

Scalability

Traditional payment systems have already proven they can handle global demand, supporting millions of transactions daily, but they rely on complex and sometimes slow infrastructure. Stablecoins are designed to scale easily, but the supporting systems are still improving and not yet as stable at a global level.

Transparency

Stablecoin transactions can be tracked on public blockchains, making it easier to verify the movement of funds. In traditional finance, many processes happen behind the scenes, so users have less visibility into how and when transactions are completed.

The Bank vs Crypto-Native Stablecoin Debate

Stablecoin adoption is creating a clear divide between traditional banks and crypto companies, especially in the U.S., where regulators are trying to decide how these assets should be treated.

One of the biggest disagreements is whether stablecoins should offer interest (or yield) to users. Banks argue that once stablecoins start paying yield, they begin to look like bank deposits, but without the same rules and protections.

Bank of America CEO Brian Moynihan warned that yield-bearing stablecoins could pull up to $6 trillion out of the banking system, which could reduce how much banks can lend and increase borrowing costs.

On the other side, crypto firms see yield as a key feature that attracts users. Jeremy Allaire pushed back, saying interest payments help with user growth and engagement, and are not large enough to disrupt the broader financial system.

“They help with stickiness, they help with customer traction,” Allaire said, adding that interest itself is not large enough to undermine monetary policy.

Traditional financial institutions are concerned that, without proper oversight, stablecoins could operate like shadow banking systems, taking in funds without following the same safety standards.

Crypto companies argue that overly strict rules could limit what stablecoins can do and reduce their usefulness. From their perspective, features like yield, open access, and flexible design are what make stablecoins valuable in the first place. Restricting these features could make the system less competitive and slow down adoption.

Are Payment Giants Set To Take Over the Stablecoin Market?

It’s evident that the direction of the stablecoin market is starting to shift from open, crypto-native systems to platforms shaped by large financial companies. With the advantage of global reach, built-in users, and regulatory access, payment giants like Visa, Western Union, PayPal, and the likes are well-positioned to scale stablecoin usage faster than crypto-native firms and shape how these assets are used in real-world payments.

Whether they dominate the market or not will depend on regulation and market structure. If new rules favour large, regulated players, control will likely concentrate around them. If not, crypto-native platforms may still compete. It’s worth asking what the outcome of this will be. Power may eventually lean toward who controls the payment infrastructure, not just who issues the stablecoins.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this piece? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}