Quick Breakdown

- Market makers are the reason most crypto tokens remain tradable. They provide liquidity, stabilise prices, and keep buyers and sellers on both sides of the market, particularly in low-liquidity environments where things could otherwise get very messy, very quickly.

- A review of more than 150 major crypto protocols found that fewer than 1% disclose anything about their market-making arrangements. One protocol did. The rest kept mum.

- That silence has consequences — for how prices are formed, for what retail investors actually understand about the markets they are participating in, and for how long regulators are willing to look the other way.

==

Every time you buy or sell a crypto token without the price lurching violently in either direction, there is a good chance a market maker had something to do with it. These firms sit quietly at the centre of crypto trading, providing the liquidity that keeps markets functional and ensuring there is always someone willing to take the other side of a trade. In illiquid markets especially, they play a critical load-bearing role.

What is far less visible is how those arrangements actually work. What are market makers being paid? What are they being given access to? What are they allowed to do — and when? A review of more than 150 major crypto protocols found that almost none of them are saying. Fewer than 1% disclose any terms related to their market-making agreements, even as those agreements quietly shape the price action that every trader in the market is responding to.

That gap between what is happening and what is disclosed is starting to attract attention.

Findings: Low Disclosure Rates Across Major Protocols

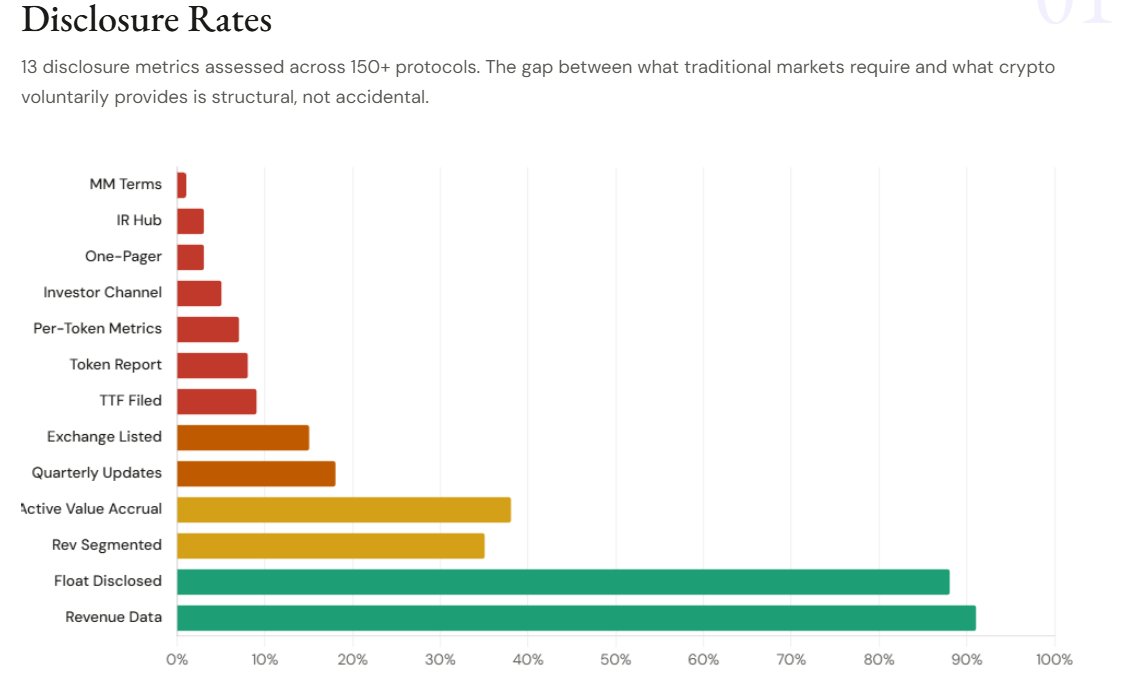

A review of over 150 major crypto protocols shows that transparency around market-making arrangements is extremely limited. According to research by crypto advisory firm Novora, fewer than 1% of protocols disclose any terms related to their market makers, even though these entities play a central role in shaping liquidity and price action across token markets.

The study covered a broad cross-section of the industry — decentralized exchanges, lending platforms, perpetual futures protocols, Layer-1 and Layer-2 networks, bridges, and centralized exchange tokens, with projects ranging from roughly $40 million to $45 billion in fully diluted valuation. Novora applied a straightforward binary test: either a protocol disclosed its market-making relationships or it did not. It also cross-referenced public analytics platforms including Artemis, Token Terminal, Dune, DefiLlama, and Blockworks Research to check for any supporting third-party data.

According to Novora founder Connor King:

“This is the single most consequential transparency gap in the industry. In traditional markets, material agreements like these are disclosed. In crypto, every market participant operates without this information.”

Out of the entire dataset, only one protocol, decentralized liquidity platform Meteora, was found to publicly disclose details of its market-making arrangements, referencing them in its 2025 Annual Token Holder Report.

One.

The key takeaway is that while the infrastructure for tracking on-chain activity is widely available, disclosure of the actual agreements shaping liquidity is almost entirely absent.

Key Risks from Hidden Market-Maker Activity

When market-making arrangements are not disclosed, the risks involved include:

Price manipulation

This is the most direct risk. Market makers can place large buy or sell orders that signal strength or weakness in a token. If those signals do not reflect genuine market sentiment, retail traders are reacting to a picture that has been painted for them, not one that reflects reality.

Information asymmetry

Market makers are often privy to developments that the wider market is not — upcoming token unlocks, supply changes, shifts in protocol activity. With that knowledge, they can position themselves ahead of price movements that other participants will only understand after the fact.

Liquidity creation

Then there is the question of what liquidity in the order book actually represents. Retail investors looking at a token’s trading depth may assume that buying or selling will be relatively straightforward. In practice, that depth may be a function of market-maker activity that could be withdrawn at any time, under terms nobody outside the arrangement can see. Investors often only discover this when the die is cast.

Loss of trust in token prices

All of this feeds into something harder to quantify but just as damaging: the erosion of trust. When people cannot see how liquidity is being managed, they start to wonder whether prices are real. That doubt tends to surface during the moments of high volatility when confidence in the market matters most and it tends to linger.

Why Regulators Are Starting to Pay Attention

Crypto markets have grown too large and attract too much retail and institutional capital for regulators to continue treating market-making as a background detail. The question of how token prices are formed and who is shaping them without disclosure is becoming a mainstream regulatory concern.

The investor protection argument is straightforward. If a token’s price stability depends on undisclosed market-making activity, retail investors have no way of properly assessing the risk they are taking on. They are making decisions based on incomplete information, and in most financial markets, that is exactly the kind of situation regulators exist to prevent.

The market integrity argument is equally clear. Fair markets require equal access to material information. When some participants understand how liquidity is being managed, and others do not, the playing field is not level and regulators, across jurisdictions, have a long history of taking a dim view of that kind of asymmetry.

There is also the question of coordination. Undisclosed market-making arrangements can, in theory, be used to quietly align trading behaviour in ways that move prices in predetermined directions. Whether or not that is happening, the structure that would allow it to happen is already in place and that, increasingly, is enough to put it on a regulator’s radar.

What Regulatory Action Could Look Like

If regulators do move on this, the most likely starting point is mandatory disclosure. Crypto projects that enter into market-making arrangements could be required to publish the terms of those agreements — what incentives are involved, what responsibilities are attached, and what the market maker is and is not permitted to do. That alone would bring the industry closer to the standard that traditional financial markets already operate under.

A step further would be reporting requirements placed directly on market makers themselves, obligating them to report the liquidity they provide, the terms under which they provide it, and any material changes to those arrangements. This would give regulators visibility into how token liquidity is actually being constructed, rather than relying on project-level disclosure.

The most significant intervention would be reclassifying market-making as a regulated financial services activity. Under that framework, firms engaging in market-making would need proper licensing and would be subject to conduct, compliance, and risk management standards. It would be a significant shift but not an unprecedented one.

Will the Industry Act, or Wait for Regulators to Force the Issue?

That is the question the whole conversation eventually comes back to. Crypto markets have matured considerably, and with that maturity has come capital, attention, and scrutiny. The structures that were tolerable when the industry was small are harder to defend now that the stakes are higher.

At some point, the argument that hidden market-making arrangements are simply how things work will stop being a sufficient answer to regulators, to institutional investors, and to the retail participants who make up the bulk of the market. The only real question is whether the industry gets ahead of that moment or waits for it to arrive.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this piece? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}