Last updated on March 6th, 2026 at 04:58 pm

There’s a familiar tension in today’s financial conversation: one side insists the future is decentralized, borderless, and permissionless; the other insists the future must be regulated, stable, and protected by mature institutions. It’s an easy debate to stage, and a convenient one, but it’s also incomplete.

Because in real life, most people aren’t ideologues. They’re just trying to move money around quickly, save without fear, invest without being misled, and access opportunities without needing the “right” passport or the “right” bank relationship.

DeFi and traditional finance (TradFi) aren’t solving different problems. They’re solving the same problems from opposite ends of the spectrum.

- DeFi excels at speed, composability, transparency, and innovation.

- TradFi (banks, fintechs, payment networks) is great at risk frameworks, consumer protections, regulatory compliance, and distribution at scale.

When these ecosystems remain isolated, both pay a price:

- DeFi struggles with mainstream trust, usability, and regulatory clarity.

- TradFi struggles with slow settlement, heavy overhead, fragmented rails, and limited experimentation.

So the real question isn’t whether they should collaborate. It’s: What kind of collaboration actually moves us forward—safely?

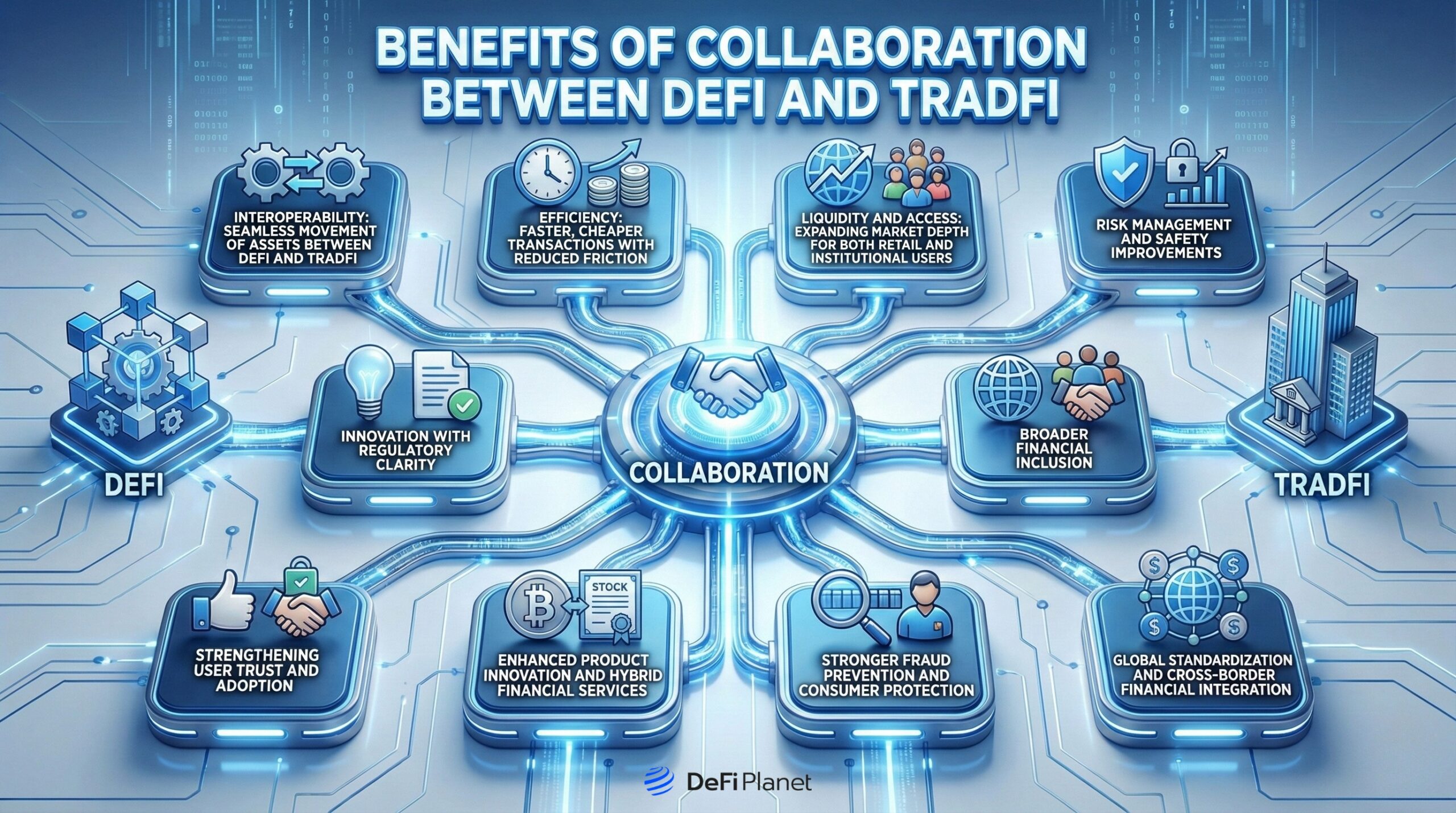

Benefits of Collaboration

Bringing DeFi and TradFi together doesn’t mean forcing one to become the other. It means designing a bridge where each side contributes what it’s best at.

Interoperability: Seamless movement of assets between DeFi and TradFi

When systems speak the same language, users don’t have to “start over” every time they change platforms. Interoperability reduces manual transfers, custodial risk, and confusing workarounds, turning finance into something that feels consistent rather than fragmented.

Efficiency: Faster, cheaper transactions with reduced friction

Combining blockchain automation with TradFi’s established infrastructure can dramatically speed up settlement times and cut processing fees. Smart contracts can replace slow, paper-based workflows, while regulated institutions ensure compliance and stability. This blend leads to fewer bottlenecks and more reliable financial operations.

Liquidity and access: Expanding market depth for both retail and institutional users

DeFi has innovation and always-on markets. Institutions have deep capital. When those connect, markets can become more liquid and less jumpy. Retail users get better access to products. Institutions get new ways to deploy capital, without having to pretend DeFi doesn’t exist.

Risk management and safety improvements

TradFi brings decades of experience in compliance, auditing, and risk controls, which can help DeFi platforms strengthen their security frameworks. Meanwhile, DeFi’s transparency and on-chain data can make risk assessments faster and more accurate. Together, these strengths can produce better security hygiene and more resilient financial products.

Innovation that doesn’t die at the “regulation” stage

A lot of good ideas never make it mainstream because they can’t fit inside compliance requirements. TradFi can help translate DeFi innovation into something regulators and everyday users can actually accept. That’s how tokenized assets, stablecoin settlement, and automated lending move from “cool demo” to “real infrastructure”.

Broader financial inclusion

DeFi is often praised for “inclusion,” and it’s true—anyone with internet can participate. But access alone isn’t enough. People also need easy onboarding, trusted interfaces, support, and protection against scams. Traditional platforms are better at distribution. DeFi is better at open access. Together, you can reach more people in a way that’s usable, not just idealistic.

Strengthening user trust and adoption

When well-regulated institutions work with transparent blockchain systems, users gain confidence in both worlds. This trust encourages cautious investors to explore DeFi and motivates institutions to adopt blockchain-based tools. Greater trust ultimately accelerates blockchain adoption and drives long-term growth for both sectors.

Enhanced product innovation and hybrid financial services

Collaboration enables the creation of hybrid products, such as tokenized ETFs, blockchain-powered savings accounts, and automated lending tools, that neither DeFi nor TradFi could build alone. These innovations offer better yields, more transparency, and improved accessibility compared to traditional options. As both sectors share technology and expertise, the range and quality of financial products grow significantly.

Stronger fraud prevention and consumer protection

TradFi’s compliance systems, identity verification, and fraud-monitoring tools can help DeFi platforms detect suspicious activity earlier. Meanwhile, DeFi’s on-chain transparency makes it easier to trace funds and identify malicious behaviour. Together, they provide users with stronger protection, better dispute resolution, and safer financial environments.

Global standardization and cross-border financial integration

DeFi operates on borderless networks, while TradFi relies on localized regulations and banking rules. Collaboration can help align standards for digital assets, payments, and identity verification across regions. This harmonization enables smoother cross-border transactions, faster global settlements, and a more unified international financial environment.

Examples of Successful Partnerships

Several major banks have already stepped into the blockchain and DeFi space. JPMorgan uses its Onyx blockchain network for tokenized settlements and has tested DeFi-based trading on public blockchains like Polygon and Avalanche.

Societe Generale recently issued tokenized bonds through MakerDAO. “The successful completion of this transaction highlights our industry-leading position in securities tokenization. It demonstrates Societe Generale’s capabilities to securely bring new instruments on-chain, in a sophisticated legal and regulatory environment,” said Jean-Marc Stenger, CEO of Societe Generale – FORGE.

HSBC uses blockchain for tokenized gold trading and settlement. These collaborations allow banks to reduce operational costs, settle transactions faster, and experiment with decentralized liquidity systems while staying compliant with regulations.

Fintech platforms using blockchain for payments and lending

Major fintech players have also embraced blockchain to enhance their payment and lending services. PayPal launched its own stablecoin, PYUSD, enabling faster on-chain payments and integrations with DeFi platforms. Revolut offers crypto trading and is exploring tokenized financial products through blockchain rails.

Stripe, though not a crypto exchange, now supports USDC payments on networks like Solana, making global transactions much faster and cheaper. These companies use blockchain to reduce friction, improve global access, and offer financial services with almost instant settlement.

Highlighting measurable outcomes

These partnerships have already produced measurable wins. Banks like JPMorgan report faster settlement times and more efficient liquidity management through tokenization trials. Fintech platforms such as PayPal and Stripe have seen increased transaction volume as users adopt stablecoin-based payments.

User engagement also rises when people get access to faster transfers, lower fees, and transparent blockchain-powered tools. These outcomes prove that collaboration creates value and signal a future where DeFi and TradFi operate side-by-side rather than separately.

Challenges and Risks

Collaboration between DeFi and TradFi offers huge upside, but it also introduces complex challenges that both sectors must navigate with caution.

Regulatory compliance and oversight concerns

TradFi operates under strict laws that govern everything from customer identification to transaction reporting. DeFi, on the other hand, was built to be permissionless, global, and resistant to centralized control, making regulatory alignment extremely difficult.

When banks partner with DeFi platforms, they must figure out who is responsible for compliance, how to enforce user verification, and how to prevent illegal activity. Without clear rules, institutions fear legal repercussions, fines, and operational uncertainty, which slows down deeper integration.

Security and smart contract vulnerabilities

In DeFi, a single coding error can result in millions of dollars lost to exploits, flash-loan attacks, or faulty logic. TradFi is not used to this level of open-access risk, especially since banks operate in insured, controlled environments.

Even when protocols are audited, new vulnerabilities may emerge, and no audit can guarantee 100% safety. To collaborate safely, institutions need multiple layers of defence, insurance pools, advanced monitoring systems, multi-sig protections, and emergency circuit breakers to reduce exposure.

Cultural and technological barriers between TradFi and DeFi

Banks and financial institutions value stability, predictability, and strict internal processes. DeFi developers value rapid experimentation, open collaboration, and decentralized decision-making.

These contrasting cultures create friction: banks move slowly due to compliance; DeFi moves fast because innovation demands it. Similarly, DeFi’s open-source tools can be unfamiliar or uncomfortable for risk-averse institutions. Bridging this gap requires both sides to understand each other’s priorities, governance models, and risk tolerance.

Legacy system limitations in banks and financial institutions

Many institutions still rely on outdated software infrastructure that was never designed to interface with blockchains, smart contracts, or digital asset wallets. Integrating with DeFi can require re-engineering core systems, upgrading security frameworks, and retraining staff, all costly and time-consuming steps. These legacy hurdles make it difficult for banks to adopt blockchain-based services at scale, slowing collaboration even when interest is high.

Risk of fragmentation across different blockchains and standards

The DeFi ecosystem is spread across multiple chains, including Ethereum, Solana, BNB Chain, Avalanche, and others, each using different token standards and interoperability tools. For institutions, this creates confusion about which networks to support, how to move assets safely between them, and whether bridges can be trusted.

This fragmentation raises integration costs, increases technical complexity, and exposes institutions to additional points of failure. Until cross-chain standards improve, collaboration remains more difficult than it should be.

Reputational risk from partnering with unverified or unstable DeFi platforms

Banks must protect customer trust and brand credibility, so partnering with a DeFi project that later experiences a hack, rug pull, or governance failure can damage their public image.

Regulators and customers may question why the institution collaborated with an untested or risky platform. This drives banks to prioritize only the safest, most transparent, and well-funded DeFi protocols, significantly narrowing the pool of potential partners.

Conclusion: Driving Real-World Blockchain Adoption

DeFi has proven that finance can be programmable, transparent and always on. Traditional finance has proven that trust, compliance and risk discipline are prerequisites for scale.

Collaboration is how those truths meet. Done well, it accelerates innovation while reinforcing safety. Done poorly, it imports the weaknesses of both worlds into one fragile system.

But the direction is hard to ignore: the financial system is being refactored in real time. And the winners won’t be the loudest ideologues. They’ll be the builders — developers, institutions and regulators — who treat finance like infrastructure and design it accordingly.

That’s what drives real-world blockchain adoption: not hype, not maximalism.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you would like to read more articles like this, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}