“Permissionless” has become one of crypto’s defining ideas, though it’s also one of the most misunderstood. It means that anyone can access, use, or build on a network without asking for approval from a central authority. No gatekeepers, no applications sitting in review queues, no institution deciding who gets access and who gets left outside the system.

That principle became the backbone of crypto and later DeFi, fueling the idea of a more open financial system that operates independently of traditional banks and intermediaries. In theory, anyone with an internet connection can participate. You can trade assets, lend funds, move money globally, or build entirely new applications directly on blockchain networks. The barrier to entry is far lower than in traditional finance, where access often depends on geography, paperwork, or institutional relationships that move at the speed of a tired office printer from 2009.

But as crypto inches further into the mainstream, that openness is running into the realities of regulation. Exchanges, stablecoin issuers, and financial platforms are increasingly expected to verify user identities, monitor transactions, comply with anti-money laundering rules, and restrict certain forms of access. Governments want oversight. Institutions want compliance. Regulators want accountability. Crypto was originally designed to avoid relying too heavily on any of those things.

That tension is now becoming one of the industry’s biggest questions. Can a system built around open participation still preserve its core principles once regulation, compliance, and institutional finance become deeply embedded in the ecosystem? Or does permissionless finance start to change the moment permission enters the picture?

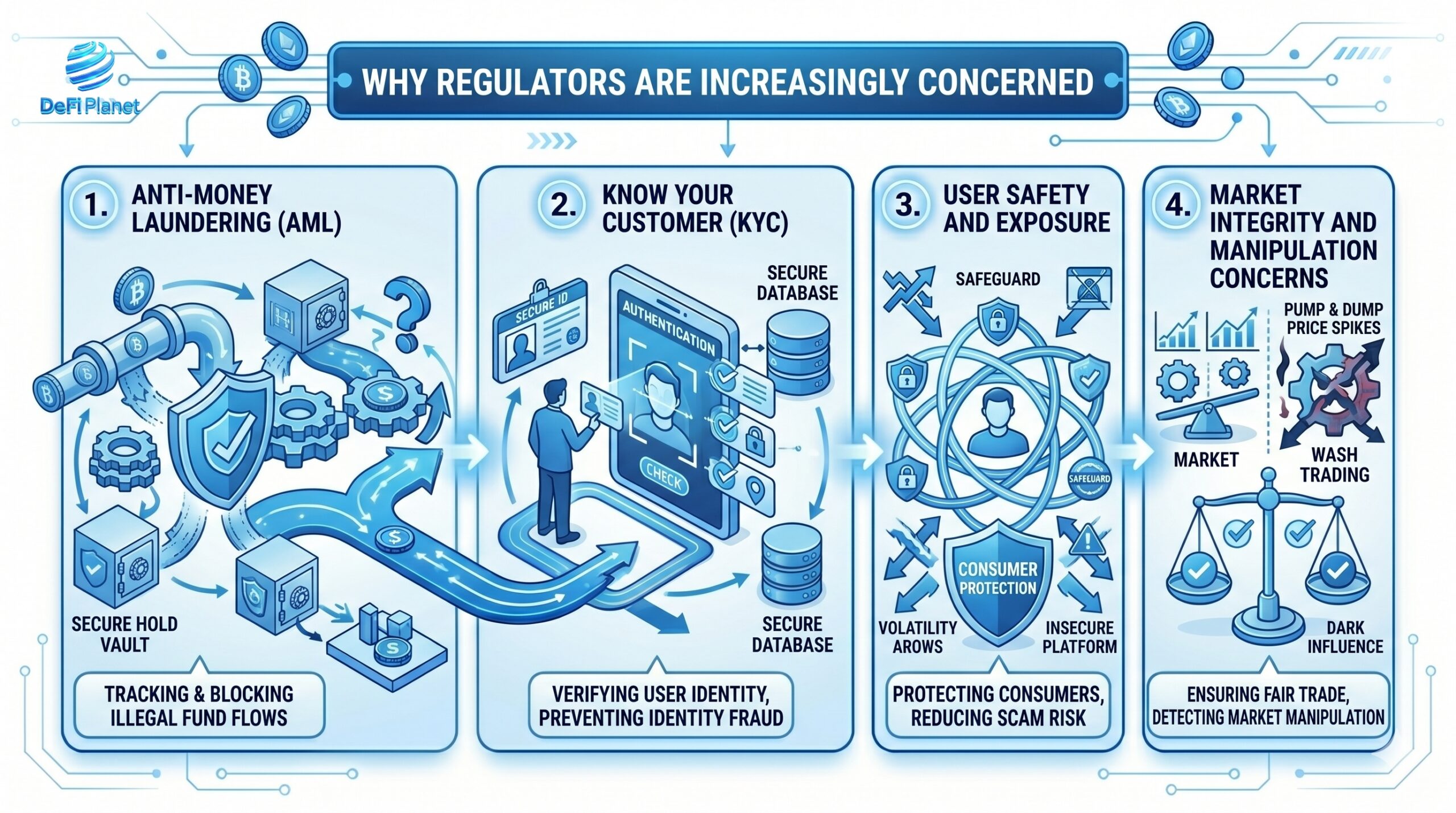

Why Regulators Are Increasingly Concerned

As crypto grows beyond niche use and starts interacting with the broader financial system, regulators are focusing on how its open, permissionless nature fits or conflicts with rules designed to maintain oversight and accountability.

Anti-money Laundering (AML)

The issue of AML tops the list of regulatory priorities. Financial regulations need to ensure that no illegal funds are channelled into or out of the financial system. While traditional finance uses intermediaries to monitor transactions, the permissionless crypto model eliminates most of these intermediaries, making it harder to identify suspicious transactions, particularly cross-border ones.

Know Your Customer (KYC)

KYC regulation requires financial services providers to know the identities of the people behind these transactions. Banks perform KYC verification routinely. However, in permissionless crypto systems, people can transact using wallets without disclosing their identity information. Transactions are known, but identities remain unknown.

User safety and exposure

One other problem pertains to the issue of the protection of consumer interests, where there is very little regulation involved. While traditional banking systems include elements like reversibility and dispute processes to protect consumers, permissionless crypto networks might expose consumers to risks without holding anyone accountable.

Market integrity and manipulation concerns

The possibility of market manipulation also exists in public cryptocurrency exchanges. The conventional finance system has strict rules against any manipulative activity such as insider trading. In addition, the authorities carefully observe any transactions for any suspicious activity.

However, on an unregulated platform, anybody can design trading bots, collude with other users, and exploit the illiquid assets on the platform. It is challenging to maintain market integrity and price fairness as more players enter the market.

Responsibility and accountability gap

One other issue is the question of responsibility for the failure of a certain project. For example, in a conventional banking environment, there are distinct roles, such as those of the bank, broker, or financial institution, that can be held accountable.

In contrast, with a permissionless crypto venture, there is no centralized authority that can be blamed for failure or when the system is exploited by hackers. As permissionless technology becomes increasingly integrated into the mainstream economy, regulators have become even more vigilant in striking a balance between protecting users and fostering innovation.

Therefore, it becomes imperative to find ways of reducing the risk of misuse while preserving the open nature of the system.

Case Study 1: DeFi and the Limits of “No Gatekeepers”

The expansion of DeFi has been really fast, with lending, trading, and yield generation enabled by smart contracts accessible to any wallet holder. However, the lack of regulation in DeFi makes it susceptible to exploitation.

There have been many attacks on DeFi systems in recent times, and in the first four months of 2026, over $750 million worth of funds have been lost to attacks and exploits on DeFi platforms. Just two major incidents account for more than $577 million of that total: Kelp DAO’s LayerZero bridge was drained of $292 million in rsETH on April 19, while Drift Protocol lost $285 million on April 1 following a long-running social engineering attack linked to a North Korean hacking group.

The issue of responsibility in DeFi is vague. Typically, smart contracts are immutable once implemented, and any errors or exploits can render them impossible to fix. In such a situation, users will have no way to recover their losses, while the developers can claim that the system works regardless of their control.

This poses a challenge for regulation since there is no central authority, no entity incorporated anywhere, and no jurisdiction applicable to the system. Consequently, regulators find it hard to identify the party at fault in the event of an error.

Case Study 2: Stablecoins and Financial System Integration

Stablecoins such as Tether (USDT) and USD Coin (USDC) are widely used for transactions and payments. The appeal of these cryptocurrencies lies in their combination of blockchain speed and the stability of fiat currencies, making them serve almost the same purpose as physical money while also serving as speculative cryptocurrencies.

However, due to their increased use beyond just trading purposes, the stablecoins have become part of the financial sector and are subject to regulation. This allowed for the growth of the market capitalization of the industry, totalling around $315 billion as of April 2026.

Another major concern is the issue of reserve backing and transparency, given historical precedents that raise doubts about issuers’ ability to ensure full 1:1 backing in difficult times.

For example, when TerraUSD (UST) collapsed in 2022, people were aware of the impact such a collapse had on the economy. In 2023, other problems, such as depegging, were observed in the case of USDC depeg (Silicon Valley Bank crisis).

Accountability is another problem faced by stablecoins. Stablecoin issuers are privately owned businesses that issue assets that function like digital dollars. However, they do not fall under the jurisdiction of financial regulatory bodies, and this makes it unclear whether they are held accountable for anything.

Case Study 3: Centralized Exchanges as Hybrid Models

Cryptocurrency exchanges serve as intermediaries that connect open blockchain technology, which enables cryptocurrencies to function, with the existing regulatory framework, making exchanges among the most strictly controlled aspects of the entire crypto infrastructure.

Binance, Coinbase, and Kraken act as platforms for buying and selling cryptocurrencies, but at the same time offer their customers the ability to store the purchased cryptocurrencies, thereby providing access to the global markets and their liquidity by means of services provided by a centralized body managing their money.

As part of their regulatory compliance obligation, exchanges conduct identification processes with the checking of personal documentation and addresses, compromising anonymity in favour of transparency. At the same time, they also conduct monitoring systems analyzing transactions to detect any fraudulent activity, sanctions risk, and abnormal behaviour.

Thanks to their structure, cryptocurrency exchanges turned out to be effective enforcement tools for regulators. Instead of checking each blockchain-based transaction, it is easier for authorities to control exchanges.

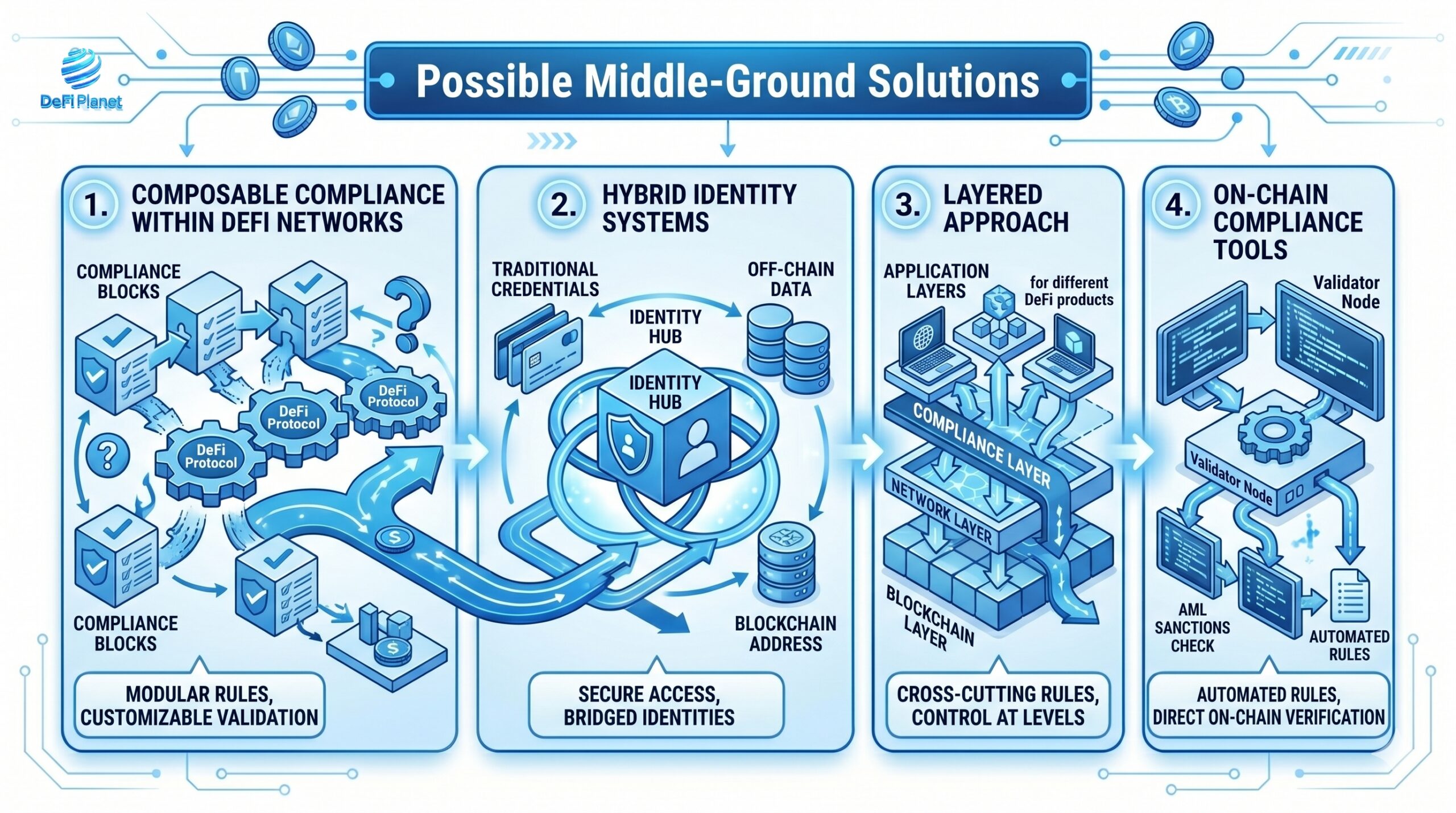

Possible Middle-Ground Solutions

The debate can shift from full openness versus full regulation to whether both can exist within a layered system that supports innovation while meeting compliance needs.

Composable compliance within DeFi networks

Composable compliance is a framework where regulatory controls are integrated into a decentralized finance ecosystem without changing the principle of openness of access. Instead of relying on a centralized regulator for this process, compliance can be implemented in an interchangeable module format that may be picked up by different regions or projects.

For example, a lending platform may permit users to access the platform from anywhere in the world but implement regulatory controls for interactions with regulated financial institutions. This model maintains the permissionless crypto nature at its very heart while at the same time allowing regulatory compatibility as an option.

Hybrid identity systems

Another potential solution is to enable users to keep their identity pseudonymous on-chain while maintaining the ability to prove identity in specific cases. This would allow users to transact on any protocol they wanted without giving away all kinds of personal information, yet prove their identity in situations requiring it.

This model avoids the need for full identification or complete anonymity, providing another option in between.

Layered approach

A potential solution to the problem is the adoption of the layered model, where the crypto ecosystem is segmented into multiple layers. In this situation, the base layer would continue to be entirely open and permissionless for all kinds of operations and initiatives.

On the other hand, additional application layers would be developed, which would be subject to much stricter regulation and control. This implies that sensitive operations, such as on-ramping fiat, institutional lending, or tokenizing physical assets, could only be conducted in those application layers.

On-chain compliance tools

Another option would be the introduction of compliance mechanisms that will be used through smart contracts. With this option, you can automate some processes, such as restricting transactions to certain jurisdictions. It could also involve imposing limits on transaction volumes or verifying users’ identities before executing certain actions.

The End of Permissionless Crypto — or Just Its Next Phase?

The debate around permissionless crypto systems boils down to whether they can continue to exist alongside traditional finance laws or if they must undergo a transformation to align with them.

A completely permissionless environment, where anyone can participate without identity checks, approvals, or compliance requirements, sits in direct tension with how modern financial regulation works. Governments and regulators are built around oversight, accountability, and controlled access. Crypto, at least in its original form, was built around the opposite idea—open participation without relying on centralized authority.

Still, it seems highly unlikely that the industry will fully abandon the permissionless principles it was founded on. That philosophy of openness remains deeply embedded in crypto culture, especially across decentralized networks and developer communities that still view unrestricted access as one of blockchain’s biggest innovations.

What is more likely is not the disappearance of permissionless systems, but their evolution. The underlying blockchain infrastructure may remain open and accessible, while the layers built on top of it begin to vary depending on jurisdiction, regulation, and use case. In practice, that could mean one version of crypto designed for institutions and regulated finance, and another that remains closer to the original decentralized vision.

The technology itself may stay permissionless at its foundation, but the way people access and interact with it is increasingly becoming shaped by geography, compliance requirements, and political realities. Crypto is not necessarily moving away from permissionlessness altogether. It may simply be entering a phase where permissionless infrastructure and regulated access are forced to coexist, even if the relationship between the two remains uneasy.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}