Quick Breakdown

- Mastercard is expanding into stablecoin infrastructure, not issuance. The company is acquiring BVNK for up to $1.8B to strengthen its ability to move value across fiat and blockchain systems, focusing on payment rails instead of launching its own token.

- BVNK brings cross-border reach across 130+ countries, multi-chain payment infrastructure, and systems that bridge fiat and crypto, enabling smoother integration of stablecoins into real-world payments.

- Mastercard aims to support stablecoin adoption through compliance, interoperability, and programmable payments, while avoiding issuer risks and positioning itself as a key infrastructure layer in digital finance.

Mastercard has entered into a definitive agreement to acquire BVNK for up to $1.8 billion, including $300 million in contingent payments. The deal strengthens Mastercard’s position in the growing digital asset ecosystem by expanding its ability to support money movement across currencies, payment rails, and regions.

Instead of competing in the crowded race to issue tokens, Mastercard is focusing on the systems that make digital money usable in the real world. As stablecoins move from niche crypto tools to core components of global payments and cross-border transfers, the real competition is shifting beneath the surface.

While many players chase token ownership and short-term upside, Mastercard’s strategy is betting on long-term influence at the stablecoin infrastructure layer. That raises a deeper question: in the future of money, is it more powerful to control the currency itself or the rails it runs on?

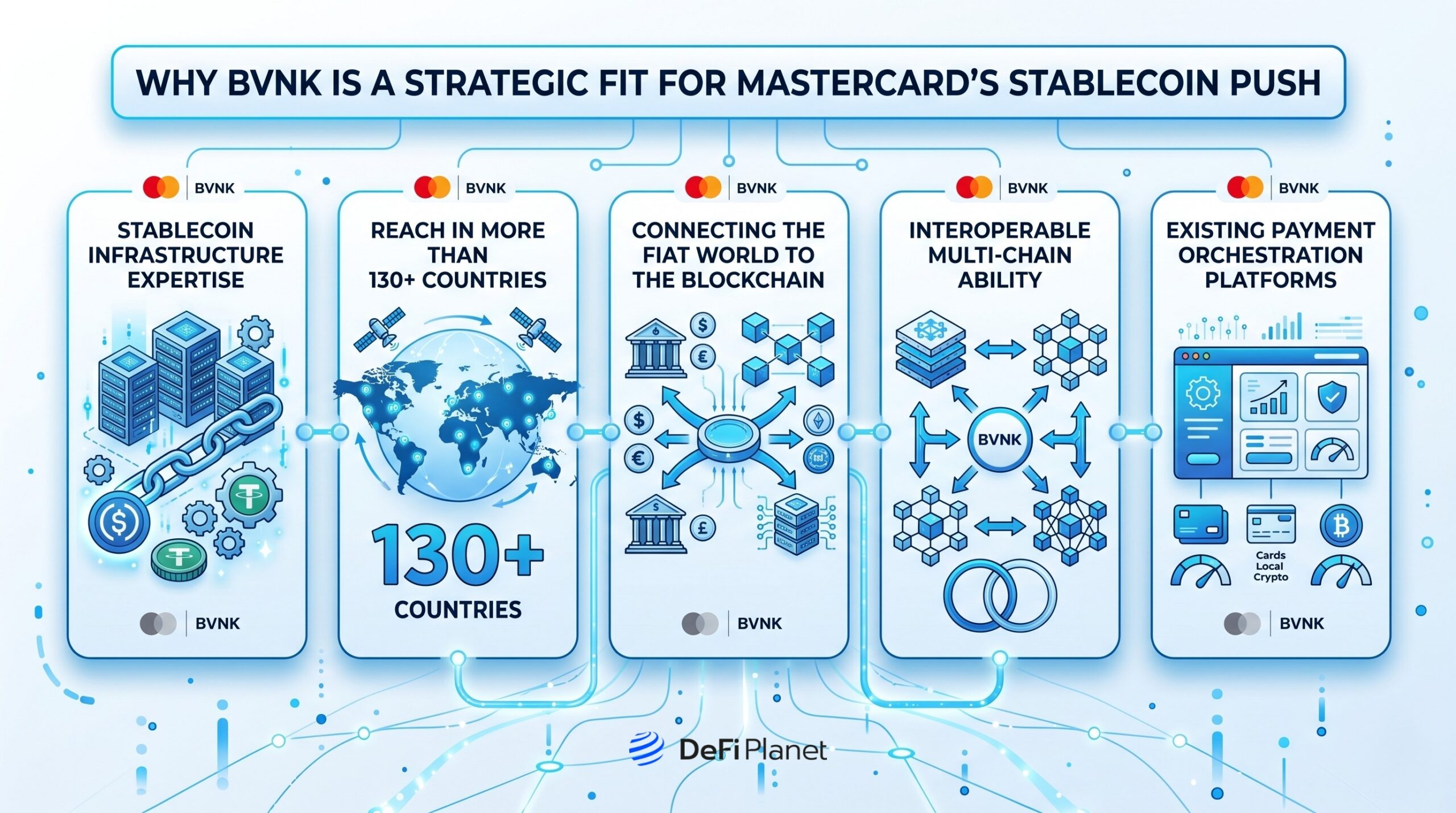

Why BVNK Is a Strategic Fit for Mastercard’s Stablecoin Push

The acquisition of BVNK gives Mastercard a strong technical foundation in stablecoin and blockchain-based payments.

Stablecoin infrastructure expertise

BVNK has built a stablecoin infrastructure that enables businesses to send and receive payments across major blockchain networks. This gives Mastercard direct access to systems that already support real-world digital currency movement.

Reach in more than 130+ countries

BVNK currently serves more than 130 countries where companies are able to make cross-border payments via either fiat or stablecoins. It helps Mastercard to extend its services to other regions without limitations.

Connecting the fiat world to the blockchain

One of the unique qualities of BVNK is that it is able to connect the fiat rails with blockchain, meaning that money can be transferred between both types of rails. This feature will be crucial in achieving real-life adoption because people still use fiat currency.

Interoperable multi-chain ability

The platform is able to work with more than one type of blockchain system, indicating that the system is independent of any particular environment. It is in line with the goal set out by Mastercard that incorporates payment platforms involving digital currencies.

Existing payment orchestration platforms

BVNK currently facilitates payments that are compliant, quick, and reliable. This makes it easier for Mastercard to integrate stablecoins into its broader global payment network without rebuilding infrastructure from scratch.

Objectives of Mastercard

Mastercard’s goal with this acquisition is to expand its payment network into the digital asset era while maintaining trust, compliance, and global interoperability.

According to Jorn Lambert, Chief Product Officer, Mastercard:

“This acquisition reinforces what we have always done, using innovation and technology to power economies and empower people. Adding on-chain rails to our network will support speed and programmability for virtually every type of transaction.”

Extend digital assets’ end-to-end coverage

Currently, Mastercard is trying to build a universal infrastructure that will allow stablecoins and tokenized deposits to be directly integrated into the payments network. Such an initiative aims to develop a system where it would become possible to transfer values from fiat money to blockchain assets without any obstacles.

In turn, it implies that banks, fintech companies, and users would have to work with both payment networks via one and the same connected payments layer.

Develop applications for real-life scenarios for stablecoins

Instead of looking at stablecoins as something to speculate with, Mastercard is now focused on developing practical financial solutions that require the usage of stablecoins to solve some particular problems. These include remittances, peer-to-peer payments, instant settlements, business payouts, etc.

Integrate fiat and cryptocurrency rail systems effortlessly

One of Mastercard’s main objectives is to create an integrated system that connects blockchain and other existing financial systems. Mastercard does not intend to substitute existing financial systems.

Its goal is to integrate them and ensure that users can switch seamlessly from fiat money to cryptocurrency without having to understand the technology behind it. For that purpose, the integration should be at a higher level to ensure speed and performance.

Improving compliance and trust in digital payments

As digital currencies get integrated into traditional finance more widely, compliance is becoming an important component. This company uses already proven security and regulatory mechanisms applied to stablecoin transactions.

That way, the transaction occurs under a secure financial framework, allowing businesses to utilize blockchain-based payment systems without taking any unnecessary risks in the process.

Position itself for programmable money and future finance

Mastercard believes that stablecoins and tokenized deposits form the basis of programmable money, where payment can be done through automation based on predetermined criteria. Programmable money can have applications in many industries such as treasury management, supply chain payments, capital market settlements, and corporate finance activities.

By anticipating this trend now, Mastercard is putting itself in a position not only as a payment company but also as an essential component of the financial system infrastructure of the future.

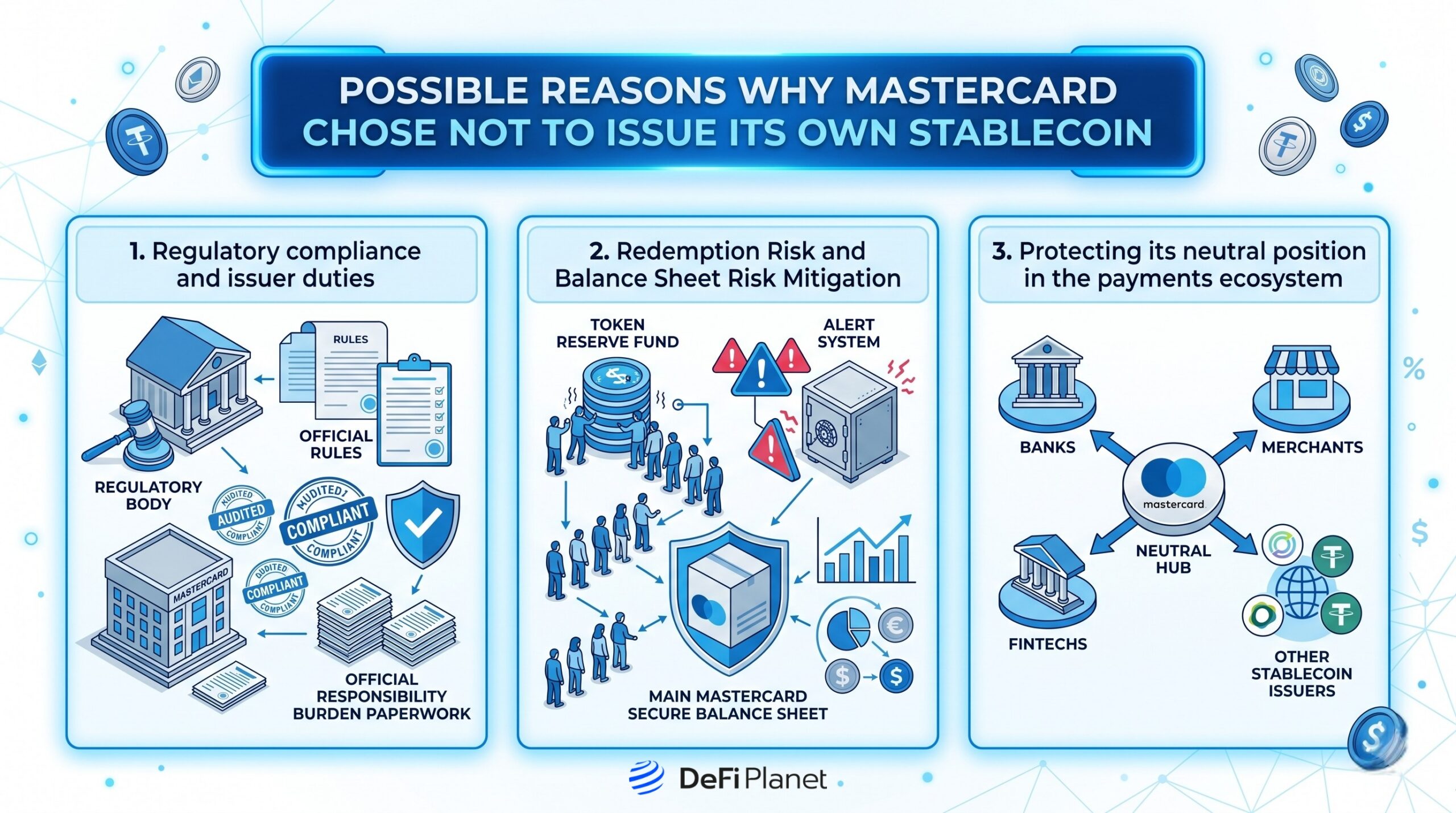

Possible Reasons Why Mastercard Chose Not to Issue Its Own Stablecoin

Here are several reasons why Mastercard could decide not to issue its own stablecoin and rely on the infrastructure:

Regulatory compliance and issuer duties

Mastercard will become the issuer of the stablecoin if it decides to create one. This means that the company will have to fulfil some responsibilities regarding reserve maintenance, auditing, and compliance with regulatory laws, like the GENIUS Act.

Overall, this move would place Mastercard in a more regulated financial institution category.

Redemption risk and balance sheet risk mitigation

The issuers of stablecoins need to hold 100% reserves for each unit in the form of liquid assets like cash and government bonds. This exposes the firm directly to the risk of having to pay out at once should the customers make a large number of redemptions.

Moreover, it also makes the firm sensitive to changes in the interest rate regime. The fact that Mastercard does not issue a stablecoin helps it avoid getting exposed to balance sheet risks.

Protecting its neutral position in the payments ecosystem

Mastercard sits in the middle of a global network that includes banks, fintechs, merchants, and payment providers. Launching its own stablecoin could turn it from a neutral infrastructure provider into a competitor within that same ecosystem.

That shift could strain partnerships and reduce its ability to serve multiple digital currencies fairly. By staying infrastructure-focused instead, Mastercard can support a wide range of stablecoins and tokenized assets without picking sides, keeping its role as a trusted intermediary intact.

Risks and Trade-Offs in Mastercard’s Strategy

By expanding its footprint into stablecoin technologies, Mastercard exposes itself to further dependence and potential future risks.

Dependence on third-party stablecoins

The company uses the technology created by other firms to create and issue stablecoins for its network transactions. Hence, Mastercard itself does not have control over the money layer; rather, it depends on third-party issuers of the stablecoins. Thus, should the issuer of the stablecoins experience any problems from a regulatory point of view or suffer any other issues, it will affect the operation of Mastercard’s business.

Uncertainty regarding the global regulatory framework for stablecoins

There remains significant regulatory uncertainty in stablecoin regulation since a uniform global framework does not exist yet. The potential change in the legal environment may include alterations to the requirements regarding reserves and licensing of the coins in addition to limitations on their cross-border transactions. Mastercard needs to cope with this uncertainty rather than having an impact on it.

The risk of disintermediation by fully on-chain systems

Over time, blockchain technology may reach a point where users can conduct transactions directly between themselves without the need for intermediaries. Should that happen, Mastercard’s position as a bridge between fiat and crypto rails would suffer, particularly if highly efficient decentralized systems were used.

Slower innovation compared to crypto-native firms

Because Mastercard operates within established financial and regulatory frameworks, its innovation cycle is naturally more cautious compared to crypto-native companies. While this improves safety and trust, it can also slow down experimentation and rapid product development, especially in fast-moving areas like DeFi, programmable payments, and on-chain finance.

Key tension: control vs reliance on external issuers

Central to Mastercard’s strategy lies a delicate balance. They become powerful through having control over the infrastructure used for payments, yet they have no control over the stablecoin itself. This brings about a structural dilemma where Mastercard controls the rails but is dependent on third parties for issuing the currency.

Long-Term Implications for Crypto Adoption

As traditional financial players like Mastercard deepen their involvement in stablecoin infrastructure, the crypto industry is gradually shifting from experimental use cases toward real-world financial integration on a global scale.

Institutional validation of stablecoins as payment rails

When a major payments network supports stablecoin infrastructure, it signals to banks, fintechs, and regulators that these assets are no longer purely speculative. Instead, stablecoins begin to be viewed as credible settlement tools for moving money across borders, especially for faster and cheaper transactions.

Shift from speculation to utility-driven crypto use cases

This evolution also marks a broader change in how crypto is used. Rather than focusing mainly on trading and price speculation, more activity is moving toward practical applications like remittances, business payments, payroll, and cross-border transfers, where stablecoins offer clear efficiency advantages.

Acceleration of global payment digitization

By integrating blockchain-based systems into existing financial networks, companies like Mastercard are helping speed up the digitization of global payments. This means money movement becomes more programmable, faster, and more connected across different currencies, banks, and blockchain networks.

Potential standardization of stablecoin-based settlement systems

Over time, increased adoption could lead to shared standards for how stablecoin payments are processed, settled, and verified. This would make it easier for different financial institutions and blockchain networks to interoperate, reducing fragmentation in the digital payments ecosystem.

Infrastructure players shaping the future of money

The biggest long-term implication is that companies controlling payment infrastructure may end up shaping how billions of people interact with digital money. Even without issuing tokens themselves, these players could influence which stablecoins are used, how transactions flow, and what the global payment system looks like in the digital era.

Is This a Quiet Dominance Strategy?

Mastercard’s strategy is taking a long-term approach by focusing on the infrastructure layer rather than competing in the crowded stablecoin issuance space. Instead of taking on the risks of being a token issuer, it positions itself as the system that enables value to move, benefiting from the growth of digital assets without directly holding the liabilities behind them.

In the bigger picture, this reflects a familiar pattern in financial history: those who control the infrastructure often end up with more durable influence than those who control the assets themselves. As crypto payments evolve, the real power may not lie with the issuers of tokens, but with the platforms that connect, route, and settle them at scale.

FAQs

How does Mastercard acquisition of BVNK affect global crypto payments?

The acquisition strengthens Mastercard’s ability to integrate stablecoins into everyday payment flows. This means faster cross-border transfers, improved interoperability between banks and blockchain networks, and more seamless movement of money between fiat currencies and digital assets.

What does BVNK actually do in the stablecoin ecosystem?

BVNK provides the technical backbone that allows businesses to send, receive, and manage stablecoin payments across multiple blockchain networks. It connects traditional fiat systems with on-chain infrastructure, enabling real-world use cases like cross-border payments, settlements, and business payouts across more than 130 countries.

What risks does Mastercard face with this infrastructure-first strategy?

Even without issuing tokens, Mastercard still depends on external stablecoin providers and evolving regulatory frameworks. It also faces long-term risks from fully on-chain systems that could bypass intermediaries and from crypto-native companies that innovate faster in decentralized finance and programmable payments.

Will Mastercard compete with stablecoin issuers like USDT or USDC?

No, Mastercard is not directly competing with stablecoin issuers. Instead, it acts as a bridge between them and traditional financial systems. This allows it to support multiple stablecoins at once while remaining neutral in the ecosystem and avoiding conflicts with banks and fintech partners.

Why is Mastercard focusing on stablecoin infrastructure instead of launching its own crypto token?

Mastercard avoids issuing a stablecoin because it would require it to act as a regulated money issuer, taking on reserve management, redemption risk, and heavy compliance obligations. Instead, it focuses on infrastructure, which allows it to support multiple stablecoins without competing directly with issuers or becoming dependent on a single token model.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}