Tokenization is often presented as a breakthrough that could unlock liquidity across a wide range of traditionally illiquid assets. The concept of tokenization is straightforward: convert assets like real estate, private credit, or collectibles into digital tokens, making them easier to access and trade on-chain.

This innovation has driven strong industry-wide interest over the years, with more asset classes being brought on-chain as part of a broader push toward digital finance.

However, key industry stakeholders like Oya Celiktemur, EMEA Sales Director at Ondo Finance, have spotlighted some gaps. During Paris Blockchain Week 2026, Celiktemur noted that there is still a widespread misunderstanding that tokenization alone can make illiquid assets easy to trade.

So, are expectations around asset tokenization’s impact on market liquidity being overstated?

Where Tokenization Actually Works Well

Tokenization creates the most meaningful impact in markets that already have active participation and consistent demand, but are held back by slow infrastructure, high transaction costs, or limited access pathways. In these environments, liquidity is not the main issue; execution and settlement efficiency are.

Rather than creating new buyers or sellers, asset tokenization improves how existing markets operate. It upgrades the underlying infrastructure that connects participants, making trading processes more direct and less dependent on multiple layers of intermediaries.

Where it adds the most value

This is most visible in traditional financial markets such as government bonds, publicly traded equities, ETFs, and large institutional asset pools. These are markets where capital is already active and continuously moving, but where settlement systems, reconciliation processes, and cross-border constraints still rely on legacy frameworks.

In these cases, tokenization helps shorten settlement timelines, reduce operational friction, and improve access to fractional ownership where it is practical. It can also simplify how assets are recorded and transferred across systems, lowering administrative overhead for institutions managing large volumes.

The key outcome is improved market efficiency. Assets move through the system faster, costs are reduced, and participation becomes easier, but the underlying liquidity is not newly created. It is simply made more usable and more efficiently distributed.

Where Tokenization Falls Short

According to Oya Celiktemur, EMEA Sales Director for Ondo Finance:

“I think there’s still this idea that tokenizing something illiquid will somehow magically make it a liquid asset, which is just not true”. She added that assets like real estate and private credit “were never that liquid” to begin with.”

Francesco Ranieri Fabracci, head of tokenization expansion at Tether, echoed a similar view.

“It’s not that if you put an asset onchain, it will be liquid,” he said, arguing that only a narrower set of instruments, including bonds, money market funds and stablecoins, are likely to achieve consistent liquidity in tokenized markets.”

In these cases, putting an asset on-chain may make it easier to represent or transfer, but it does not solve the deeper issue: there simply aren’t enough active participants willing to trade it at scale.

Assets with inherently weak or inconsistent demand:

This includes ultra-niche private investment opportunities that are attractive only to a very limited circle of potential investors, as well as very specific physical assets in the real world, such as rare collectibles, custom-made products, or privately negotiated investments. These assets already find it difficult to attract buyers, even in traditional markets.

After they have been tokenized, these assets usually do not undergo much trading in the secondary market. While it may be technically possible to trade these assets, they rarely see any trading volumes, since there is no solid or ongoing demand for them.

Sometimes, asset tokenization creates a false impression of liquidity, which implies that a certain asset becomes more easily traded due to its digital presence alone, rather than due to its actual trading.

While tokenization might help better represent and transfer assets, it cannot create the demand necessary for the creation of a functional and liquid market.

RELATED: Top 10 Top Use Cases of Asset Tokenization

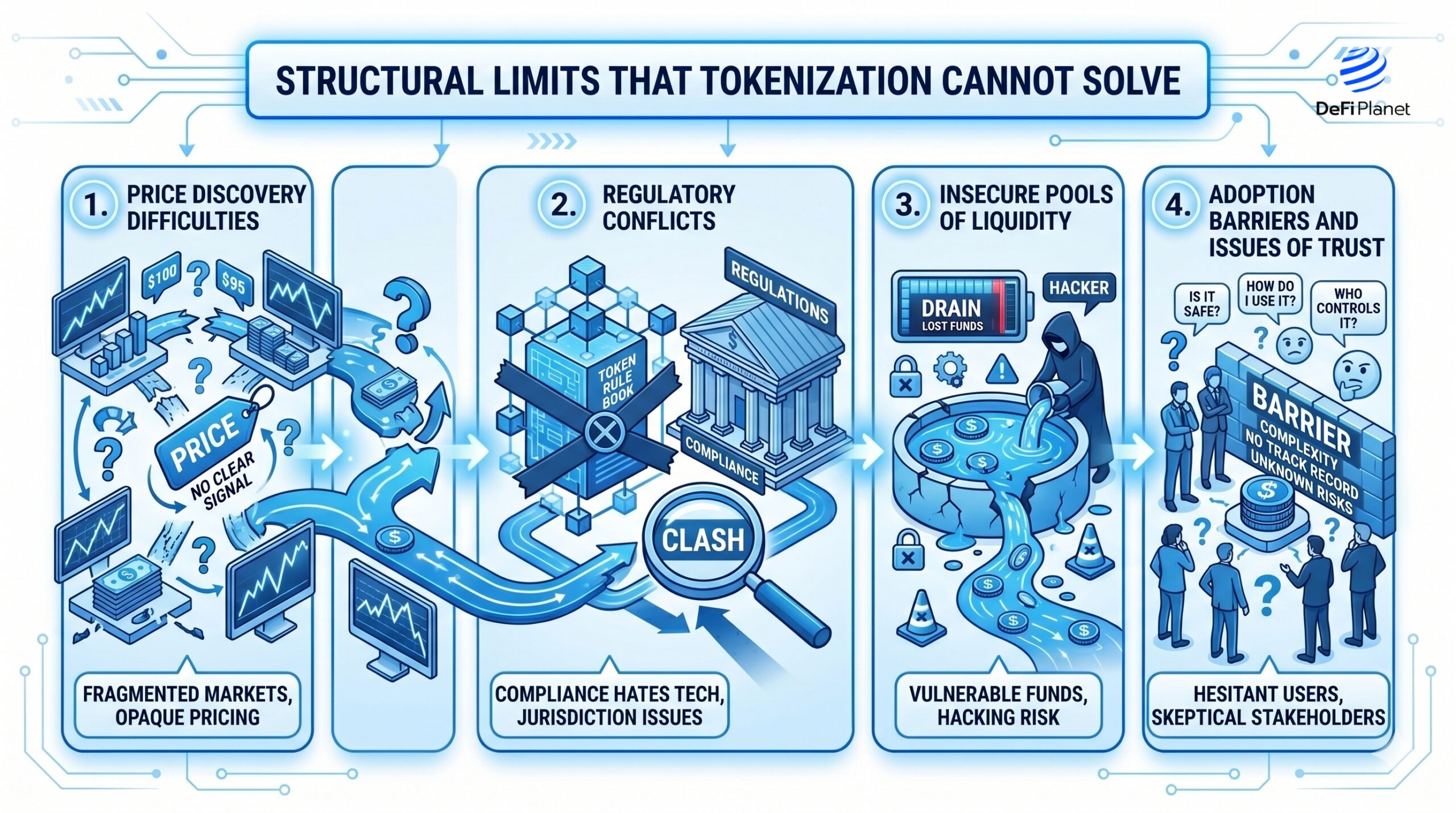

Structural Limits That Tokenization Cannot Solve

Even with improved technology and on-chain access, tokenization still runs into deep structural problems that are rooted in market economics.

Price discovery difficulties

The lack of active and continuous trading makes valuation extremely subjective. Without sufficient trading, there is little price discovery, which means that the valuation will likely be guesswork. Tokenization would theoretically improve trading efficiency, but it may also increase mispricing risks, particularly when the markets are thinly traded, where even a small trade could impact the price.

Regulatory conflicts

While tokenization provides liquidity to an asset, it does not alter the fact that the underlying asset remains subject to regulation within real-life jurisdictions. Every legal authority imposes its own laws on who should be able to purchase, own, or sell various assets.

Such limitations can negatively impact the emergence of secondary markets as well as the process of active trading. On some occasions, a lack of clarity regarding regulation can act as a barrier similar to liquidity.

Insecure pools of liquidity

The availability of liquidity typically concentrates around certain markets, ensuring that pricing and exchange become relatively easy processes. By tokenizing an asset, such pools of liquidity could be fragmented across several chains, exchanges, or issuers of tokens.

If liquidity is spread across various locations rather than being concentrated in a single pool, each separate pool will be less liquid, with higher price slippage. The result is a more scattered ecosystem where liquidity exists in theory but is less effective in practice.

Adoption barriers and issues of trust

Liquidity of an asset is not only determined by supply and demand but also depends on issues of trust in the trading system. In the case of tokens, all three aspects need to be trusted: the token issuer, the market itself, and the legislation that backs up the token.

If these elements are unfamiliar or lack proven credibility, investors may be wary. This is especially true for institutional investors who are more likely to be satisfied only when there is regulatory certainty.

The Illusion of “Always-On Markets”

One of the more overlooked claims regarding asset tokenization is that it fosters round-the-clock markets due to the constant operation of blockchain technology. At first glance, this is indeed an essential improvement over conventional markets where trading can only occur during designated hours.

However, there is a significant difference between market accessibility and actual market activity. While blockchain systems operate on a 24/7 basis, this does not mean that participants will engage in trading, add liquidity, or effectively price assets. In other words, the system may be up and running without having the market itself being adequately liquid.

The true liquidity factor still relies on the following:

- Market makers that constantly give prices

- Constant involvement of the investors

- Capital flow that facilitates trading processes

Otherwise, even if tokens can always be bought on the market, they don’t have enough depth in the order book.

What this means is that there is a slight misconception here. Because trading is always possible, people assume that liquidity must also be constant. However, what might actually exist is availability without depth, and markets that are available but not necessarily working well.

The confusion here lies in the mixing up of technical uptime and liquidity. While tokenization ensures that transactions happen at any time, this does not necessarily mean that there will be sufficient demand or supply in the market.

In that sense, “always-on markets” are not automatically liquid markets; they are simply markets that never close, even when participation is low.

RELATED: Is Tokenization All That It’s Cracked Up To Be?

What This Means for the Future of Tokenized Markets

Instead of focusing on its failures, the lesson from asset tokenization may very well be one of changing our expectations on how market development proceeds. Perhaps the biggest change here is that the results of any market activity remain more influenced by the underlying economic conditions rather than any design features in technology.

This implies that the next wave of financial tokenization may not see a generalized increase in liquidity for all types of assets. Rather, such activities would revolve around certain niches where there is already existing participation and where infrastructure gains can be iteratively compounded.

In this respect, tokenization may turn out to be more of a filtering process, whereby some assets prove to naturally facilitate trading environments while others do not, no matter their technological construction.

It implies that the future progress may not rely heavily on the development of tokenization alone, but rather on recognizing where it truly resonates with market reality.

Are Expectations Around Tokenization’s Impact on Market Liquidity Being Overstated?

Yes, but not because tokenization lacks value. The issue is that it is often expected to solve liquidity problems in a uniform way across very different types of assets. In reality, illiquidity isn’t a single, uniform problem. This may result from low demand for the asset, lack of historical trade experience, or more fundamental challenges associated with how some types of assets are owned, valued, and traded. As these factors vary, the effects of tokenization will be unevenly distributed based on the specific market being targeted.

Here, assumptions differ greatly. For example, if there is much participation and trading in the market, the process of tokenizing the asset becomes much more effective because of good mechanisms and decreased costs. Nevertheless, if participation is low by definition, then making an asset a token does not automatically make trading increase.

Ultimately, the most important misconception about asset tokenization is to regard it as a universal fix for liquidity. In reality, liquidity is created by participating continuously, interacting with prices, and investing resources. The absence of these elements means that tokenized markets can operate perfectly well technologically, but they will lack meaningful economic depth.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.”