Think of two AI systems, one needs access to weather data from an API, the other provides that data. They agree on a price, and payment happens automatically with no humans involved. Now, imagine this happening millions of times per second. How would those tiny payments flow? Are the old payment rails like Visa, SWIFT, or Stripe up to that task? Or does blockchain provide a better approach?

A future with decentralized machine commerce is no longer science fiction, and developers are already building systems where machines can discover services, agree on pricing, and execute payments automatically. The real question is whether existing financial systems can support this transition, or whether we need a new foundation built on blockchain microtransactions.

To understand this, we need to look closely at how machine-driven commerce actually works, and whether using crypto as the native settlement layer for AI-to-AI payments is necessary or simply one option among many.

Why Traditional Payment Rails Struggle at Machine Speed

Traditional financial systems were designed for humans, with payment networks like Visa, SWIFT, and platforms like Stripe, assuming that a person is involved in each transaction. That assumption creates friction when machines begin to transact at scale, as we can imagine the complexity such a process will entail.

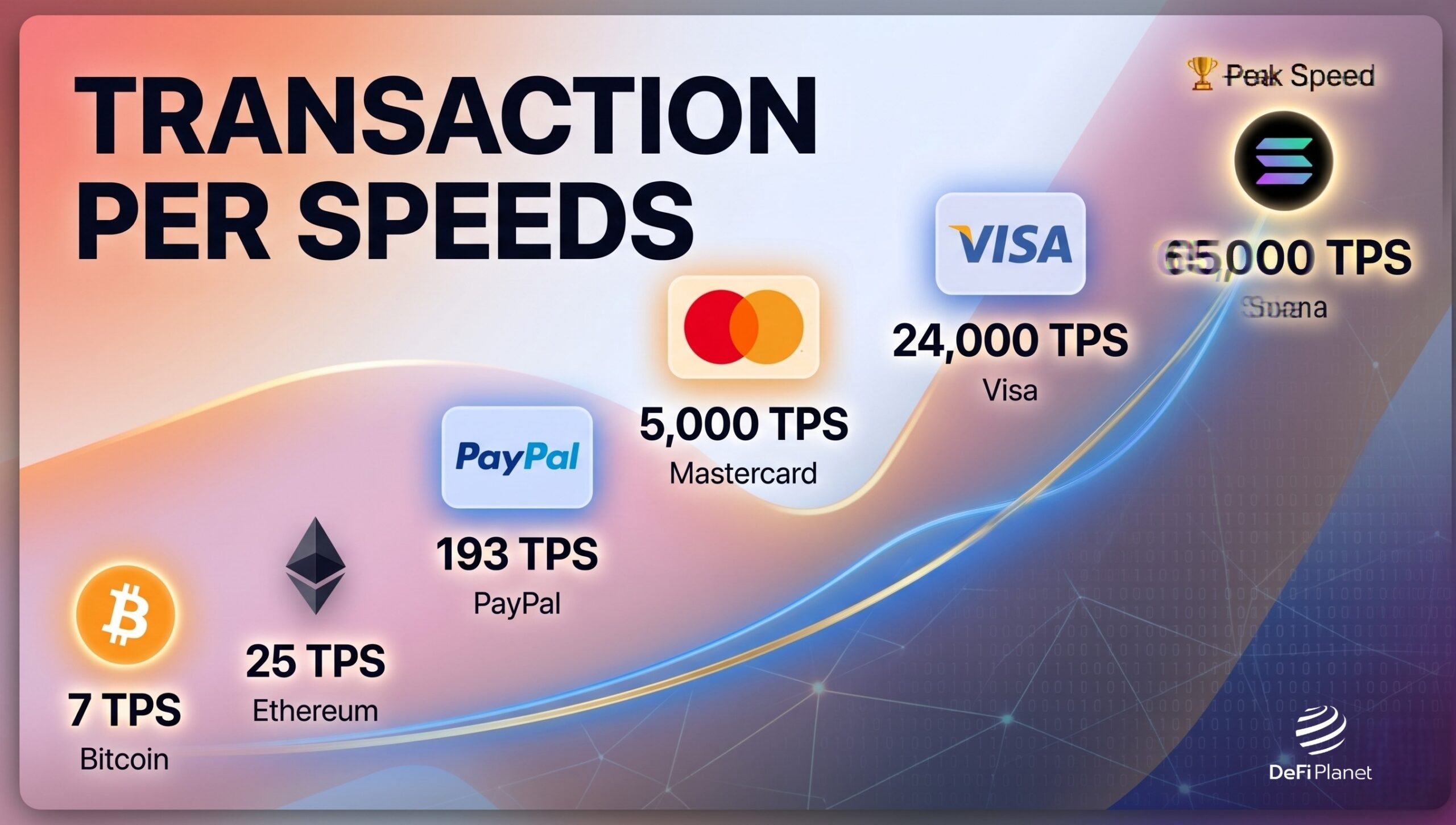

According to Visa Inc., the network processes around 2,400 transactions per second on average, with peak capacity much higher. While this is impressive for human commerce, it becomes limiting in a world where AI agents could generate thousands of transactions per second individually.

Cost is another major constraint, and card payments often include a fixed fee of around $0.30 plus a percentage of the transaction value. This structure makes very small payments impractical. From what we have found, research and industry analysis consistently show that sub-dollar payments are inefficient or impossible on traditional rails.

We also have the issue of timing, which creates friction for such machine-to-machine commerce because we can have systems like SWIFT taking hours or days to settle cross-border payments. Machines operating in real time cannot wait for delayed settlement because they require instant confirmation and continuous availability.

This is where the limitations of traditional infrastructure become clear; it was never designed for autonomous, high-frequency, machine-driven transactions.

Trust and Verification Between Machines

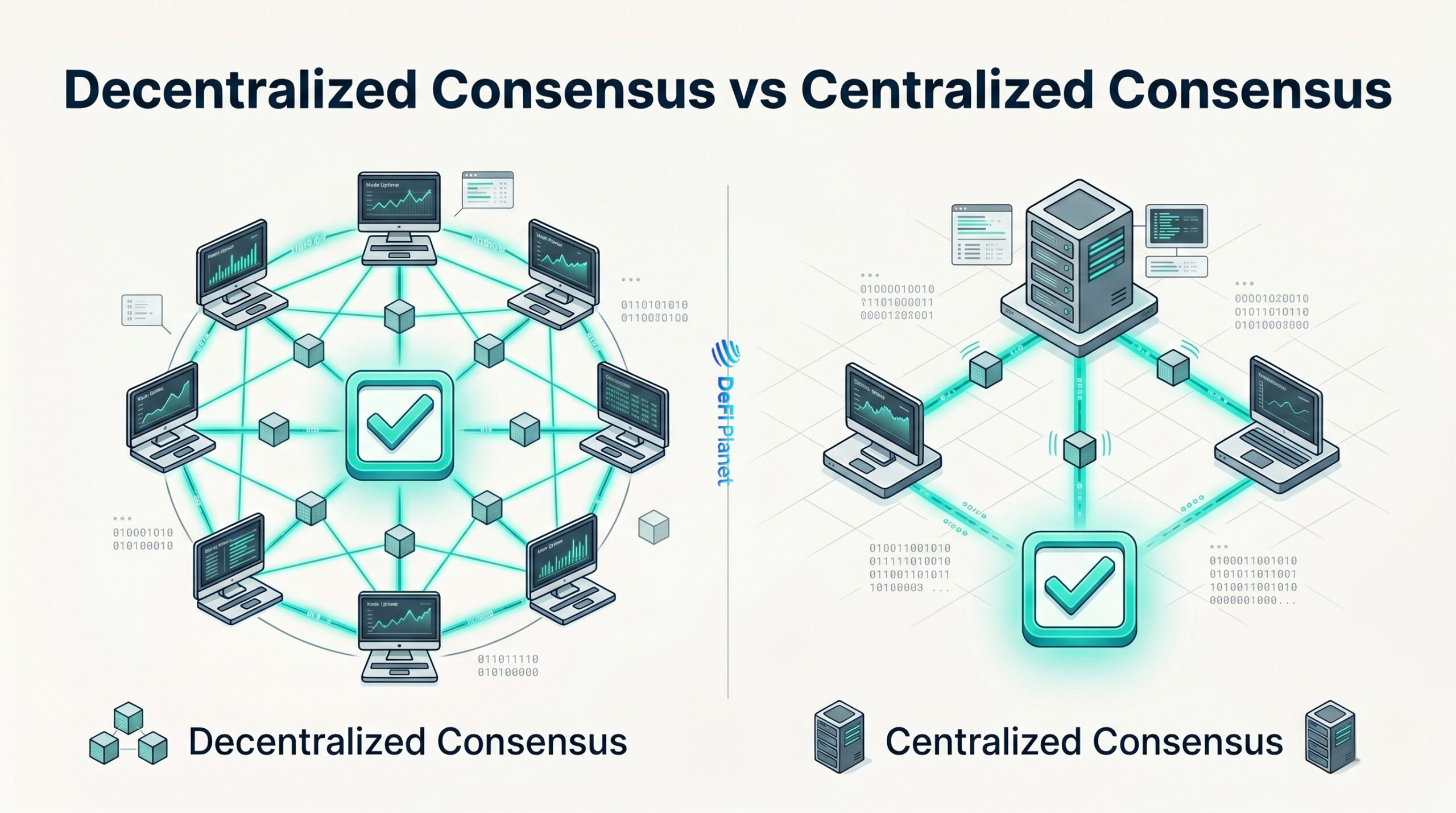

When two companies transact, they often rely on legal contracts or regulatory frameworks; AI agents don’t have that luxury. So how do two machines trust each other? On a blockchain, trust is placed in the code and consensus mechanism, not in any single party. If an AI pays with a blockchain transaction, that transaction is recorded on a public ledger, and both parties can verify it instantly.

If they use a smart contract, they can see the contract code and trust that it will execute exactly what’s written. For example, if an AI pays for data, a smart contract could automatically release the data when payment is made. Neither party has to trust the other’s word; by contrast, paying through a bank or card network often involves trusting the bank not to reverse charges or impose conditions. One analysis puts it bluntly: AI agents cannot operate with the uncertainty of chargebacks or reversals, and crypto transactions more often than not tend to be final (especially on blockchains with fast finality like Solana or Layer 2s).

This reduces risk for small automated payments. Another trust aspect is identity; traditional KYC rules don’t fit AI agents well, and crypto wallets tend to solve this by using cryptographic identities. A wallet address can be a permanent, non-human identity. Researchers call this “wallet-as-identity”, and it is globally verifiable. A blockchain history shows exactly how much an agent has paid or earned in total. You don’t need a corporate registration; you just have a wallet with a history.

This is an advantage for AI payment infrastructure because it sidesteps the whole problem of how an AI gets a bank account and allows it to simply have a wallet on a blockchain network. Of course, this doesn’t eliminate all trust issues, and machines will still need to verify that counterparties are legitimate, but they can build a reputation on-chain over time. Some proposals even add layers, such as oracle networks, to verify off-chain data (e.g., price feeds, identity checks). The key point is that the financial settlement can be made atomic and transparent by code, which is very different from a multi-party banking process.

Why Blockchain Microtransactions Fit Machine Commerce

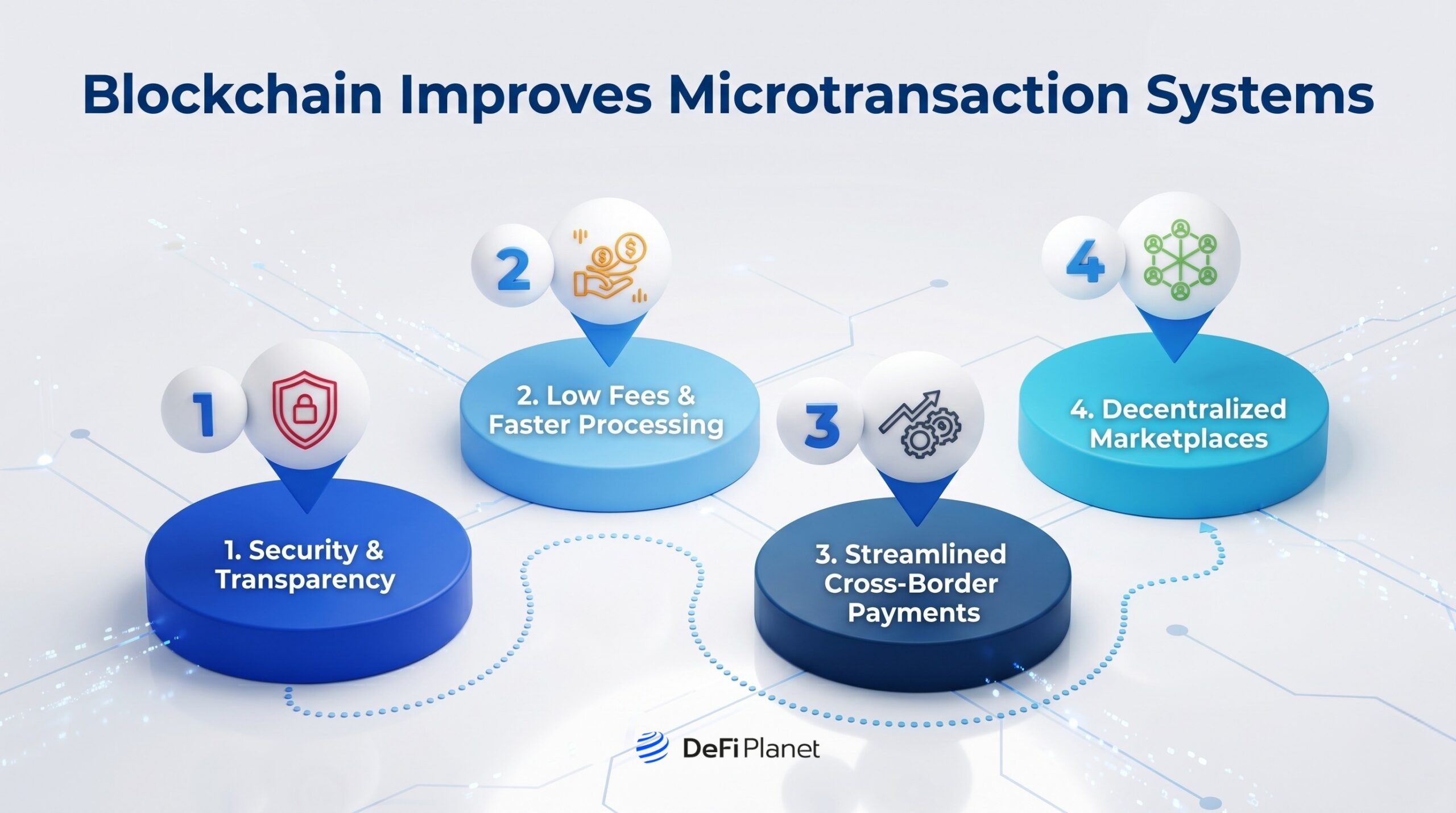

Blockchain systems typically take a fundamentally different approach; they allow value to move directly between participants without relying on centralized intermediaries. This makes them highly relevant to AI payment infrastructure.

One of the key advantages here is accessibility; when you have AI agents that cannot easily open bank accounts, but can operate crypto wallets, it makes it ideal for decentralized blockchain networks as payment layers for autonomous agent commerce. Another advantage is programmability. Smart contracts allow payments to be automated and conditional. For example, an AI agent could release payment only after receiving verified data, creating trust without relying on intermediaries.

Blockchain systems also operate continuously, and unlike banks, they do not close on weekends or holidays. This makes them suitable for machine environments that run at all times, and most importantly, they enable blockchain microtransactions. Networks like Solana are known for low fees and high throughput, with theoretical capacities exceeding tens of thousands of transactions per second, making it possible to support payments of such size and enabling machine-to-machine transactions with crypto micropayments at scale.

Micropayments Change the Economics of the Internet

Micropayments sit at the center of this discussion because in a machine economy, transactions are likely to be very small but extremely frequent. An AI might pay fractions of a cent for data, compute, or bandwidth.

Traditional systems struggle here because fees exceed transaction value. Blockchain systems, however, can process transactions at extremely low cost, with some networks achieving fees below $0.001 per transaction, making them viable for high-frequency machine activity.

This is why many researchers argue that using crypto as the native settlement layer for AI-to-AI payments becomes more attractive as transaction size decreases. The smaller and more frequent the payment, the stronger the case for blockchain-based systems.

Real-World Pilots and the Role of Stripe and Companies

Even though the vision is futuristic, parts of this system already exist in tests or limited use. Stripe, for example, has been working on agentic commerce. They built an Agentic Commerce Protocol (ACP), which lets AI agents check out from stores via APIs. They also introduced Shared Payment Tokens, which allow an agent to spend on behalf of a user without exposing the user’s credit card details. This system currently uses credit cards and digital wallets behind the scenes, not crypto, but it shows how big payment companies are adapting traditional rails to serve AI.

Stripe’s work proves that non-crypto systems can handle machine payments too, and they even collaborated on open standards with Google and other partners, though they still rely on Mastercard, Visa, etc., with new software layers. In one Stripe blog, they explain that they enable AI agents to transact using tokens and APIs and have managed to keep fraud near zero. This suggests that legacy systems can be extended to support some agent use cases.

However, Stripe itself sees stablecoins and crypto as part of the future mix as well (e.g. the shared payment tokens are meant to allow any payment method, including crypto, for agents). Meanwhile, projects like Cloudflare and Coinbase are pushing fully blockchain-native solutions, and the x402 standard allows machines to request micropayments via HTTP, assuming stablecoins as the payment currency. Google’s AP2 standard, while still allowing cards, explicitly includes stablecoin as a supported payment type, and this hybrid approach means that agents and merchants can accept multiple payment rails.

The technology ecosystem is not rigidly one or the other; it’s building ways to use both, and one interesting pilot: ElaadNL in the Netherlands showed a mini Tesla car paying with a cryptocurrency called IOTA after using an EV charger.

Another is the Machine Payments Protocol (MPP) co-developed by Stripe and a company called Tempo, which uses stablecoins to let AI agents pay just like OAuth for money. These early experiments demonstrate feasibility, even if they are not mainstream yet.

Comparing Crypto to Legacy Systems

- Speed/Finality: On-chain stablecoin payments can finalize in a few seconds (or even under a second on fast blockchains). Visa or SWIFT can take days to finalize in the sense of irreversible settlement.

- Cost: Blockchain micropayments can cost near-zero per transaction, while traditional rails charge at least tens of cents, and cross-border bank payments can cost $10–$50 each.

- Programmability: Crypto supports smart contracts and programmable wallets; traditional systems do not natively offer this (they rely on back-office processes). So crypto makes new use cases possible, like direct API payments.

- Open Access: Crypto systems allow anyone to join with a wallet. Traditional rails require accounts, IDs, etc., and an AI agent can boot up and get a wallet easily, but can’t easily open a bank account.

- 24/7 Global: Crypto works 24/7, while credit rails are limited to working hours and holidays. This ‘always on’ nature is important for machines, which do not sleep. The downside of crypto rails includes issues like the need for oracles, blockchain bloat, and security risks. No on-chain system is perfect. ChainScore Labs points out that current blockchains have troubles with storing massive numbers of tiny payments, with cross-chain bridging costs, and with privacy.

- Security: There is also the risk of front-running (MEV) when payments are predictable, and this is an active research problem. By contrast, legacy rails have decades of battle-tested security, compliance, and user trust; they also have extensive existing infrastructure and networks of merchants. In many scenarios, especially for larger payments or within a single ecosystem, they might remain the simplest solution.

What AI Agent Spending May Look Like

Andreesen Horowitz (A16Z) makes an important point: as AI agents scale up, most of their spending may become bulk B2B deals on negotiated terms (net 30, volume contracts, etc.), where traditional rails (invoices, wires) will handle the high-volume portion.

The key is that the future likely involves both, and we may see hybrid systems where an agent uses centralized systems for some transactions and blockchain for others. For instance, an AI within Amazon’s infrastructure might charge a user’s card, but if the user’s agent interacts with a new external data vendor, it might use stablecoins.

Or an enterprise could pay its AI agent’s allowances via traditional payroll, while the agent trades microtasks on-chain. The Agentic Commerce Suite by Stripe, for example, was designed to be protocol-agnostic so sellers don’t have to “bet their roadmap on any single spec”.

Cross-Border Payments Without Friction

Cross-border transactions are another area where blockchain shows clear advantages. Traditional systems rely on intermediaries, currency conversions, and regulatory checks that introduce delays and costs.

Blockchain networks are inherently global, and a transaction between two AI agents in different countries can settle in seconds using stablecoins, without requiring correspondent banks.

The Bank for International Settlements has explored how distributed ledger technology could improve cross-border payments by reducing friction and increasing transparency. For machines operating across borders, this kind of frictionless system is essential.

Trust Without Human Oversight

In human commerce, trust is enforced through contracts and legal systems. In machine commerce, trust must be built into the system itself.

Blockchain enables this through transparency and immutability, and transactions are recorded on a shared ledger that both parties can verify. Smart contracts enforce these rules automatically.

This reduces reliance on trust between parties and instead, trust is placed in the system – a key principle behind decentralized machine commerce.

Crypto transactions also offer strong finality. Once confirmed, they are difficult to reverse, making it important for AI agents that cannot manage disputes or chargebacks as humans do.

ALSO READ: What are AI Agents in Crypto and Why They Matter Now

Programmable Compliance in a Machine Economy

A common concern is regulation; Financial systems must comply with laws related to identity, taxation, and anti-money laundering. Blockchain systems can incorporate compliance directly into their design, allowing smart contracts to enforce rules automatically.

Projects exploring digital identity and compliance layers show that AI payment infrastructure can evolve without ignoring regulation, suggesting that blockchain systems are not inherently incompatible with legal frameworks but instead offer new ways to implement them.

Another emerging concept is “programmable compliance,” where rules such as transaction limits, geographic restrictions, or reporting requirements are embedded directly into smart contracts. For example, a payment between two AI agents could automatically check whether both parties meet regulatory standards before completing, and if conditions are not met, the transaction simply does not occur.

This model shifts compliance from a reactive process to a proactive one. In traditional systems, regulators often review transactions after they happen, but in a blockchain-based system, compliance can be enforced in real time, reducing the need for intermediaries and lowering the risk of violations.

There are already early examples of this approach; Certain stablecoin issuers include controls that allow them to freeze or restrict funds linked to sanctioned addresses. Enterprise blockchain platforms are also experimenting with permissioned environments where only verified participants can transact, and these systems show that compliance and decentralization are not mutually exclusive.

However, this approach also introduces trade-offs. Embedding rules into code reduces flexibility, and financial systems sometimes require human judgment, especially in complex or emergency situations. A fully automated compliance system may struggle to adapt to unexpected scenarios or nuanced legal interpretations.

There are also questions about governance; if compliance rules are written into code, who decides those rules? And how are they updated when regulations change? These challenges highlight the need for hybrid models that combine programmable enforcement with human oversight.

Despite these concerns, the broader trend is clear. Blockchain technology allows compliance to move closer to the transaction itself. Instead of relying solely on external institutions, rules can be enforced at the protocol level.

Real-World Experiments and Hybrid Systems

Real-world experiments show that both crypto and traditional systems are being adapted for machine commerce. Stripe has developed agent-based payment systems that allow AI to transact via APIs, which rely on traditional rails but introduce automation layers.

At the same time, blockchain-based systems like the x402 protocol allow APIs to request payments directly in stablecoins. Google’s work on agent payment standards also supports multiple payment methods, including crypto, suggesting that the future will not be dominated by a single system but instead will likely involve a combination of traditional and blockchain-based infrastructure.

So, is Crypto Necessary or Optional?

The answer is not simple, and crypto is not strictly required for AI-to-AI commerce. Traditional systems can be extended to support automation, as seen with companies like Stripe. However, crypto offers clear advantages in specific areas. It excels in micropayments, global transactions, and programmable settlement. These are all critical features for machine-driven economies.

This is why many experts believe the future will be hybrid. Some transactions will use traditional rails, while others will rely on decentralized blockchain networks for autonomous agent commerce.

In this model, machines will choose the most efficient system based on context, and large payments may go through traditional systems, while small, high-frequency payments may use blockchain microtransactions.

Conclusion

The rise of AI agents is forcing a rethink of how money moves. Machines operate faster than humans and require systems that match their speed and scale, making AI payment infrastructure more essential. It must support automation, low-cost transactions, and global access.

Crypto is not the only solution, but it is one of the most powerful tools available, enabling it to serve as the native settlement layer for AI-to-AI payments in a way that traditional systems struggle to match. At the same time, legacy systems are evolving. The future will likely combine both approaches, creating a flexible and efficient financial layer for machines.

What matters most is not which system wins, but whether the system works, and as machines begin to transact at scale, the infrastructure behind those transactions will define the next phase of the internet. And in that future, enabling machine-to-machine transactions with crypto micropayments may not just be an innovation; it may become a necessity.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

“Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”