Last updated on March 7th, 2026 at 12:47 am

Quick Breakdown

- ZeroLend’s collapse shows that DeFi lenders rely on deep, active liquidity. Expanding to more blockchains does not help if those networks have few users or little trading activity.

- Because profit margins are small, even slight drops in trading volume, higher costs, or security problems can cause a protocol to lose money. This shows how fragile DeFi lending economics can be.

- Dependence on oracles, bridges, and external services, combined with rising security costs, can create hidden risks that threaten sustainability even for protocols with high total value locked.

ZeroLend’s shutdown has drawn attention to the financial pressure facing DeFi lending platforms after it reported ongoing losses tied to low activity and other issues. While the collapse happened to ZeroLend, it shows that lending economics can quickly become fragile when user demand and costs are not balanced

More broadly, this event raises important questions about whether DeFi lending, as a business model, can stay sustainable without steady liquidity, active users, and efficient operations.

Why ZeroLend Collapsed: Key Factors Behind the Shutdown

“After three years of building and operating the protocol, we have made the difficult decision to wind down operations,” ZeroLend’s founder, known only as “Ryker,” said in a post the protocol shared to X.

ZeroLend’s shutdown was the result of several factors:

Declining user activity and liquidity on supported chains

ZeroLend mainly ran on Ethereum layer-2 networks, but some of these chains slowly lost users and trading activity. As liquidity dropped, borrowing and lending slowed down, so the protocol earned fewer fees. Founder Ryker said some blockchains had “become inactive or significantly less liquid,” which made it harder for ZeroLend to work as a lending market.

Rapid collapse in TVL

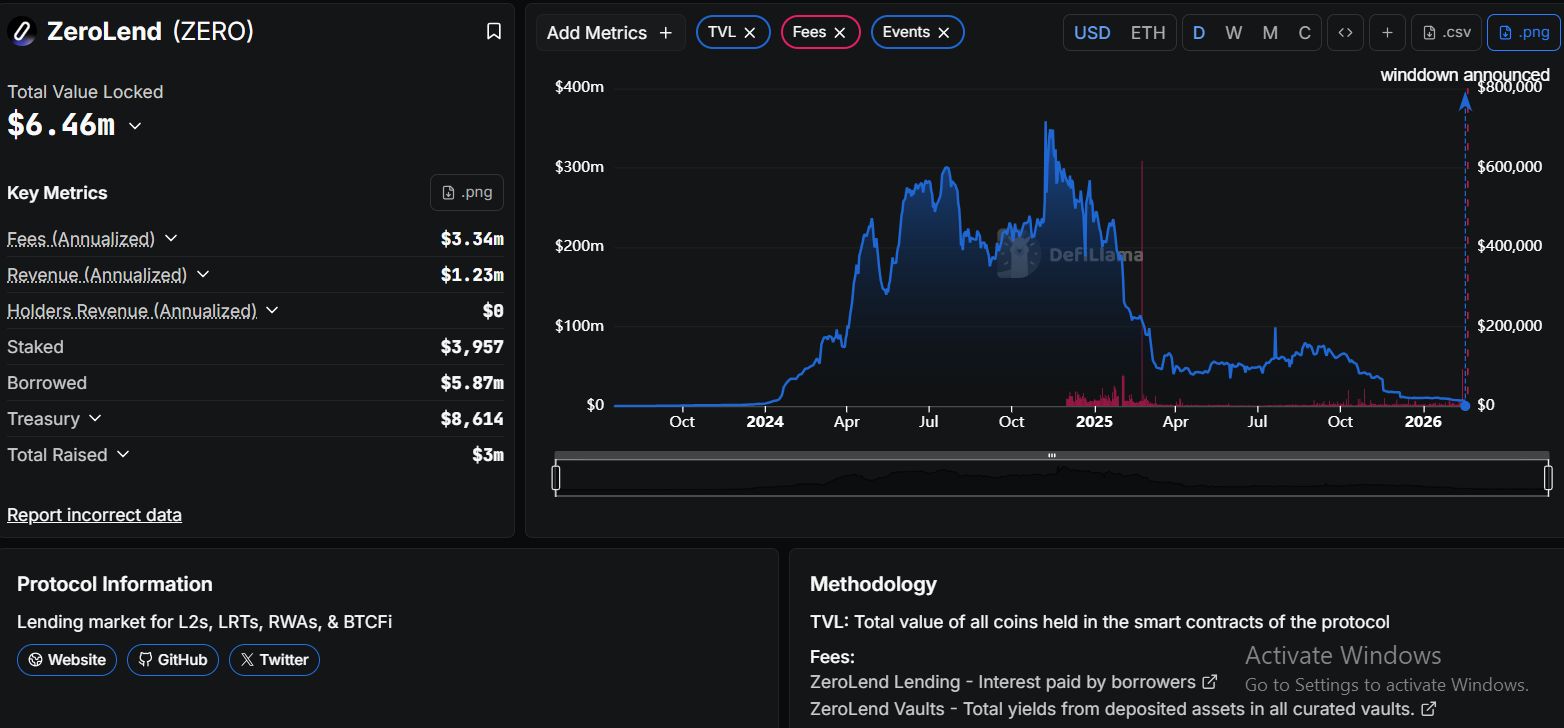

At its peak in November 2024, ZeroLend had almost $359 million in total value locked. Later, this dropped to about $6.46 million, according to DefiLlama.

Oracle support breaking down critical infrastructure

Lending protocols rely on oracles to provide price data and keep markets stable. Ryker said some oracle providers stopped supporting certain networks ZeroLend operated on, making it “increasingly difficult to operate markets reliably or generate sustainable revenue.” Without dependable data feeds, lending markets become risky, fragile, or unusable.

Thin margins combined with rising security risks

DeFi lending already runs on narrow profit margins, especially during low market activity. As ZeroLend grew, it attracted more attention from hackers and scammers, increasing operational and security costs. Ryker noted that this mix of “thin margins and high risk” led to long periods where the protocol was operating at a loss.

Exploits damaged confidence and added financial strain

In February last year, an exploit hit ZeroLend’s Bitcoin product on the Base blockchain, draining lending pools. While the team worked to trace and recover funds, the incident weakened user trust and added financial pressure. Ryker said affected users would receive partial refunds funded through an airdrop allocation, highlighting the long-term cost of security failures.

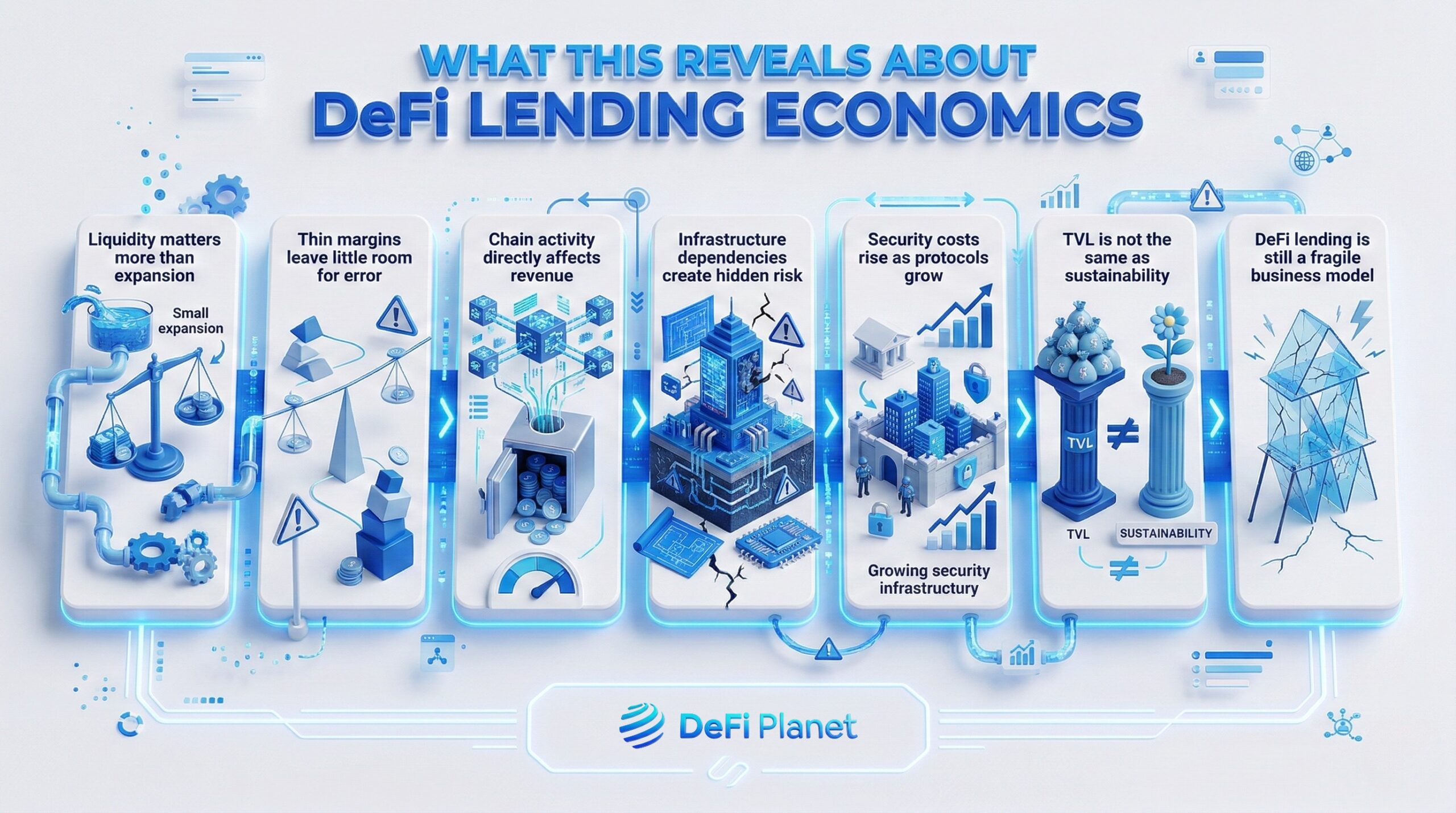

What This Reveals About DeFi Lending Economics

ZeroLend’s collapse highlights the hard economic realities behind DeFi lending and shows why many protocols struggle to survive beyond early growth.

Liquidity matters more than expansion

DeFi lenders only work when there is deep, active liquidity. Operating on multiple chains means little if those networks lack users, trading activity, and capital, because low liquidity leads to weak revenue and higher risk. Without enough borrowers and lenders, markets become inefficient and unattractive to new users.

Thin margins leave little room for error

Lending protocols earn small spreads, so even minor issues like falling volumes, higher costs, or stalled markets can quickly push operations into losses. This makes DeFi lending far more fragile than many users realize, especially during market downturns.

Chain activity directly affects revenue

When supported blockchains become inactive, lending demand drops, and interest income dries up. DeFi lending is tightly linked to network usage, not just smart contract design, meaning protocols suffer when ecosystems lose momentum.

Infrastructure dependencies create hidden risk

DeFi protocols rely on oracles, bridges, and external services to function properly. If those providers stop supporting a chain, markets can break down, increasing operational risk and forcing protocols to shut down products or entire networks.

Security costs rise as protocols grow

As platforms attract more users and capital, they also attract hackers and scammers. Rising security expenses and the risk of exploits can overwhelm already thin margins, turning growth into a liability rather than an advantage.

TVL is not the same as sustainability

High total value locked can disappear quickly if incentives fade or confidence drops. Sustainable DeFi lending depends on real usage and long-term demand, not temporary yield-driven inflows.

DeFi lending is still a fragile business model

ZeroLend shows that without consistent liquidity, reliable infrastructure, and manageable risk, even established lending protocols can fail. This raises broader questions about which DeFi lenders can survive outside of bull markets.

Lessons for Other DeFi Lenders

Other DeFi lenders can draw clear lessons from ZeroLend’s collapse about what actually matters for long-term survival.

Demand-led chain expansion is critical

Expanding to new blockchains only makes sense when there is proven user demand and active capital. Launching on quiet or declining chains increases costs without generating revenue and can weaken the entire protocol.

Liquidity depth matters more than chain count

Supporting many chains looks impressive, but deep liquidity on fewer networks is far more valuable. Strong liquidity improves market efficiency, attracts borrowers, and reduces the risk of stalled or broken lending pools.

Lending models must survive low-activity periods

DeFi lenders need to test whether their economics work during slow markets, not just in bull cycles. Stress-testing for low volumes, reduced fees, and rising security costs helps reveal whether a protocol can stay solvent when conditions turn unfavorable.

Cost control is as important as growth

Rapid expansion increases operational, security, and maintenance costs. Without tight cost management, lending protocols can burn through resources faster than they generate revenue, especially when activity slows.

Risk management must evolve with scale

As protocols grow, exposure to exploits, oracle failures, and bad debt increases. Lenders need stronger monitoring, conservative parameters, and contingency plans to prevent isolated issues from becoming existential threats.

DeFi Lending Enters a Reality Check Phase

ZeroLend’s collapse shows that investors are now focusing more on the basics instead of hype. Deep liquidity, real borrowing demand, cost control, and risk management matter more than fast growth or incentives.

For DeFi lending platforms, long-term survival depends on being efficient, not just on reach. Protocols that control costs, manage risk, and operate on active, liquid chains are more likely to retain users and liquidity as market conditions tighten.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this piece? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}