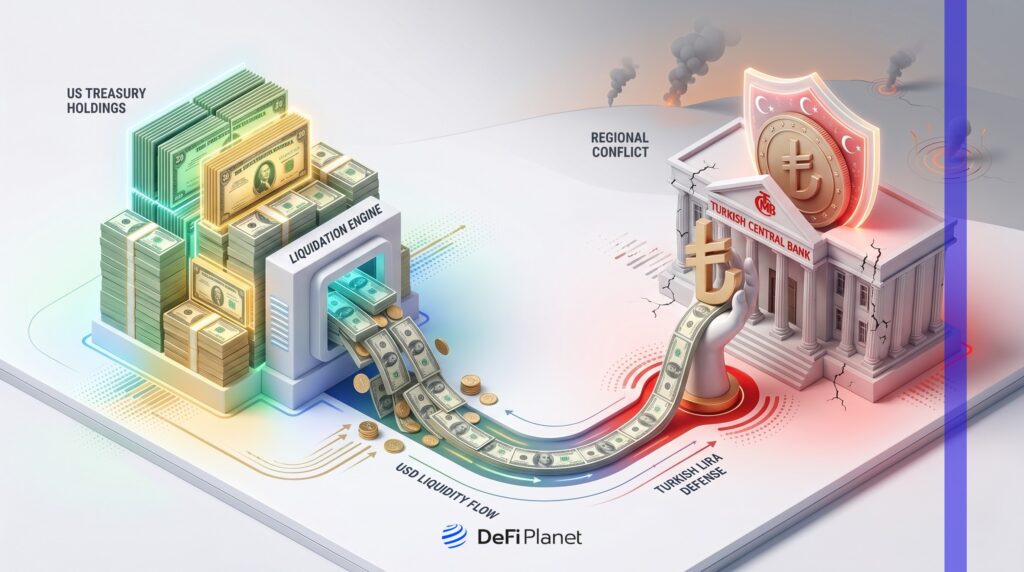

Turkey has almost completely sold off its U.S. Treasury holdings. According to Treasury data, the Central Bank of the Republic of Turkey (CBRT) sold about $14 billion in U.S. debt securities in March, leaving only $1.6 billion outstanding.

Turkey liquidates nearly all US Treasuries as Iran war bites economy: Report

Turkey sold $14bn in US Treasuries as it moved to support the lira

— Middle East Eye (@MiddleEastEye) May 21, 2026

By selling U.S. Treasuries in international markets, the CBRT receives U.S. dollars, which it can then use to buy lira (Turkey’s official currency) and support its value. This sharp move forms part of a wider trend among emerging markets to support their weakening currencies amid mounting global pressures.

In the short term, Turkey’s large Treasury sales could push U.S. bond yields higher and spark volatility in international debt markets. While Turkey’s $14 billion sale is modest compared to the multi-trillion-dollar size of the U.S. Treasury market, such sudden offloading is significant for a single country and can send a signal to other investors. If other emerging market central banks follow suit or reduce their holdings, it could amplify selling pressures, raising borrowing costs globally.

Higher yields may reduce investors’ risk appetite and could trigger outflows from other emerging-market bonds, particularly in countries with similar vulnerabilities. These spillover effects highlight how shifts in one nation’s reserve management can influence broader financial stability. Why did Ankara make such a drastic decision, and what does it reveal about the risks facing local economies during global upheaval?

How Geopolitical Conflict Is Deepening Turkey’s Economic Crisis

Turkey’s BIST 100 is suffering one of its worst crashes since 2008, with ₺2 trillion (~$45B) wiped out over 8 days. The turmoil in Turkish markets is closely linked to the continuing conflict with Iran, which has disrupted energy supplies. Before the conflict, about 14% of Turkey’s natural gas came from Iran. Now, infrastructure problems have stopped these supplies, so Ankara must look for other fuel sources in a global market where prices are high.

In response, Turkey has approached alternative suppliers, including Russia, Azerbaijan, and Algeria, to fill the gap, and has also discussed increasing LNG imports from the United States and Qatar. Each of these options carries its own challenges, as prices are often higher, contracts can be less flexible, and new logistical arrangements may be required, raising both cost and supply chain risks for Turkey in the short term.

These economic disturbances have made Turkey’s economy very vulnerable. Even though the central bank took strong action, using up its foreign-exchange reserves and about 50 tons of gold, the lira is still near record lows. Inflation has jumped to 32.4%, and 10-year government bond yields are now over 35%. At the same time, the lira has lost about 5% of its value against the U.S. dollar since the conflict began, making imports priced in dollars more expensive for Turkey.

By comparison, during the 2018 Turkish currency crisis, annual inflation peaked at around 25%, and 10-year bond yields remained near 21%, while the 2001 crisis saw inflation around 70% at its height but bond yields at roughly 80%. This time, the mix of persistently high inflation, surging bond yields, and aggressive asset sales paints a picture of stress more severe than that of most post-2000 emerging-market crises, except for the worst episodes.

Meanwhile, Turkey’s parliament approved a major tax package to attract investment, companies, and wealthy individuals from abroad. Key incentives include a 20-year income tax exemption on foreign earnings for qualifying returning citizens, significant reductions in corporate tax rates for new foreign investments in priority sectors such as advanced manufacturing, green technology, and financial services, and lower tax on capital gains for international companies relocating their regional headquarters to Turkey.

Certain business profits may also be taxed at preferential rates or be fully exempt, depending on the scale and nature of the investment. In simple words, Turkey is trying to become a friendlier place for investors and workers by offering lengthy tax breaks and sector-specific incentives.

Türkiye passes investor-friendly reforms offering a 20-year tax break for foreign earnings, expanded IFC incentives and new perks for multinational firms and manufacturershttps://t.co/hF6ySHdAt3

— Türkiye Today (@turkiyetodaycom) May 21, 2026

President Recep Tayyip Erdogan initially introduced the incentive package in April, characterizing Türkiye as a prospective “center of attraction” for international capital, commerce, and talent.

Treasury and Finance Minister Mehmet Simsek subsequently described the incentives as “radical” measures intended to attract long-term investment and encourage companies to relocate regional operations to Türkiye.

Turkey Moves To Tax Crypto Gains At 10% In Draft Bill.

If enacted, Turkey’s proposed 10% tax on crypto income and gains would be among the highest rates in the region. For comparison, the United Arab Emirates and Qatar currently do not tax crypto gains, while most European countries apply rates between 0% and 30% depending on the asset and holding period. The move positions Turkey as more interventionist than nearby countries, which could influence both investor decisions and the competitiveness of local crypto exchanges.

Turkey’s ruling Justice and Development Party has submitted a draft bill to parliament that would impose a 10% tax on income and gains from cryptocurrency transactions. The proposal would bring digital assets under the country’s expenditure tax system and could give platforms a new role in collecting levies from users.

The draft also suggests that platforms subject to capital gains tax may have to withhold 10% from user gains on a quarterly basis. It further gives the president the power to adjust the rate between 0% and 20%, leaving room for the final burden to shift if lawmakers advance the bill. The move occurs as Turkey remains one of the region’s busiest crypto markets.

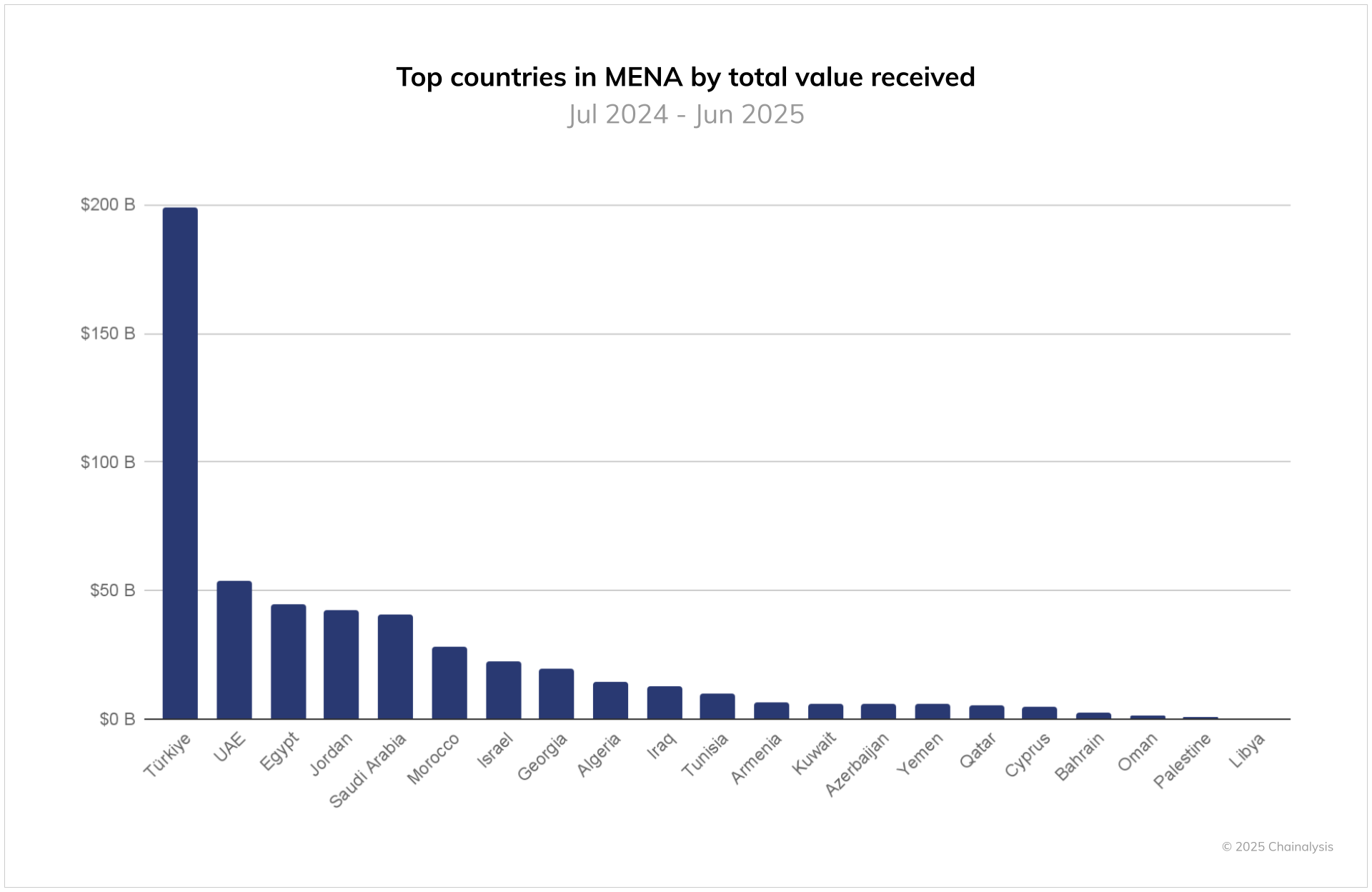

Chainalysis ranked the country first in the Middle East and North Africa for crypto transaction volumes, reporting about $200 billion in on-chain activity between July 2024 and June 2025.

“Such plans for taxes risk doing more harm than good at this stage,” said Bora Erdamar, director of the BlockchainIST Center. “These tax plans could push users away from local platforms and slow the growth of the market. These measures may be appropriate once the sector is mature, but for now, I think it is too early”, Erdamar said.

Also, the Turkish Ministry of Treasury and Finance has introduced broad crypto regulations to address money laundering and illegal activities. The main measures involve a minimum 20-character description for transactions, mandatory withdrawal delays of 48 to 72 hours, and transfer limits for stablecoins—$3,000 daily and $50,000 monthly. Platforms that fully comply with the Travel Rule may double these limits. Breach of rules may lead to license revocation and financial penalties.

Strategies for Reserve Management

Going forward, Turkey will likely need to find new ways to manage its economy beyond asset sales. Ankara may introduce tighter capital controls or seek new trade deals and payment systems with nearby countries to keep energy imports flowing. As traditional reserves run low, some analysts have proposed that central banks add digital assets, such as Bitcoin or stablecoins, to their reserves as a hedge against global shocks. There are a handful of real-world cases to consider.

In 2022, the Central African Republic made Bitcoin legal tender and announced its intention to hold digital assets in its national reserves, though the implementation details remain unclear. El Salvador’s central bank has been most prominent, purchasing Bitcoin for its national reserves and integrating it into the country’s financial system, but this approach has drawn caution from international institutions and has been marked by ongoing volatility.

Other central banks, such as the People’s Bank of China, have launched digital currencies (such as the digital yuan), but these are tied to national currencies and are not part of reserve diversification strategies that use volatile cryptocurrencies. However, the practicality of adding digital assets to reserves remains very uncertain.

Digital assets remain highly volatile, and their regulatory treatment varies widely across countries. There are also concerns about liquidity, transparency, and potential cybersecurity risks for large institutional holders, such as central banks.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on X, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”