The way money moves through the financial system has changed a lot in just a few years. Payments are now faster, more flexible, and less tied to the slow banking systems that used to control global finance. Stablecoins handle billions of dollars in transactions every day, blockchain networks can send value across borders in seconds, and tokenized financial systems are beginning to challenge traditional payment methods. It is safe to say the world is experiencing a financial revolution.

Europe is paying closer attention because this change creates both an opportunity and a growing strategic concern. Dollar-backed stablecoins like USDT and USDC already dominate large parts of the digital asset economy, reinforcing the influence of the US dollar in emerging financial infrastructure. Europe faces increasing pressure to ensure the euro remains relevant in a world where value may eventually move more through tokenized networks than through traditional banking systems.

This is where the Single Euro Payments Area (SEPA) comes into the discussion. A growing idea is that integrating tokenization into SEPA payments could help make euro-based digital payments faster and more competitive in the on-chain financial system. The bigger question is whether integrating tokenization into Europe’s payment system can strengthen the euro’s global role before digital dollar systems move too far ahead.

Why SEPA Matters to Europe’s Financial System

SEPA is one of Europe’s biggest financial integration projects designed to make euro payments across participating countries work as smoothly as local bank transfers. Before SEPA, cross-border payments within Europe were often slower, more expensive, and more complicated because different countries used different banking systems and standards.

SEPA solved this by creating a unified framework for euro payments. Businesses and consumers could send money across borders using the same standardized rules and processes, making transfers faster, cheaper, and easier to manage. This also helped strengthen trade and financial integration across Europe.

For the European Central Bank (ECB), SEPA is not just a payment tool. It is also a way for Europe to maintain monetary sovereignty, meaning it keeps greater control over its own financial infrastructure rather than relying heavily on foreign systems.

This is why tokenization is becoming strategically important to Europe. Integrating tokenized payments into SEPA could help modernize Europe’s payment rails while ensuring the euro remains relevant in the global financial system.

Why the ECB Is Pushing Hard for Tokenized Payments

So what is the ECB’s stance on SEPA payments?

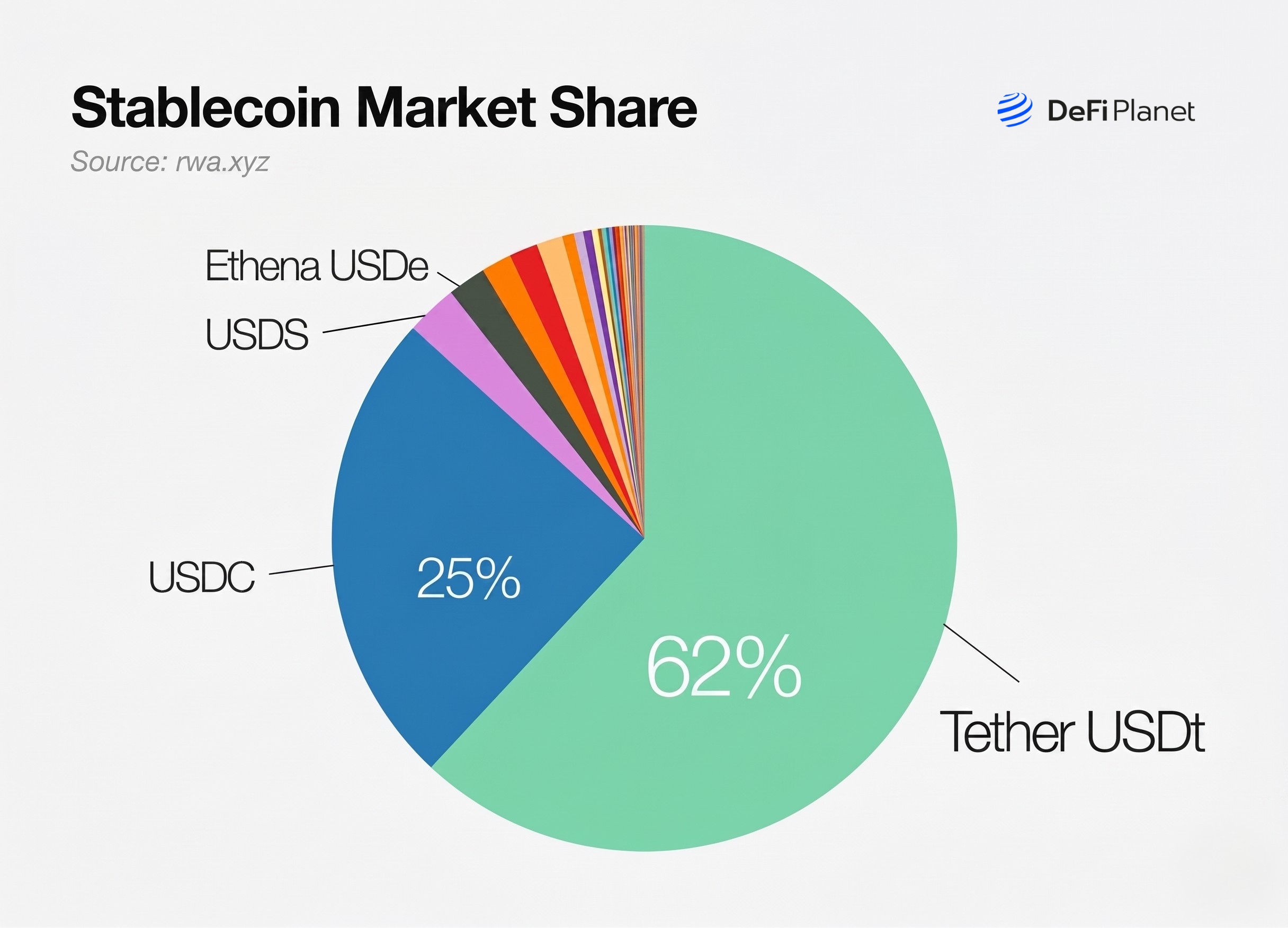

The ECB is paying close attention to how fast digital money systems are evolving. One key concern is the rapid rise of stablecoins, especially US dollar-backed ones like USDT and USDC, which together control over 85% of the stablecoin market.

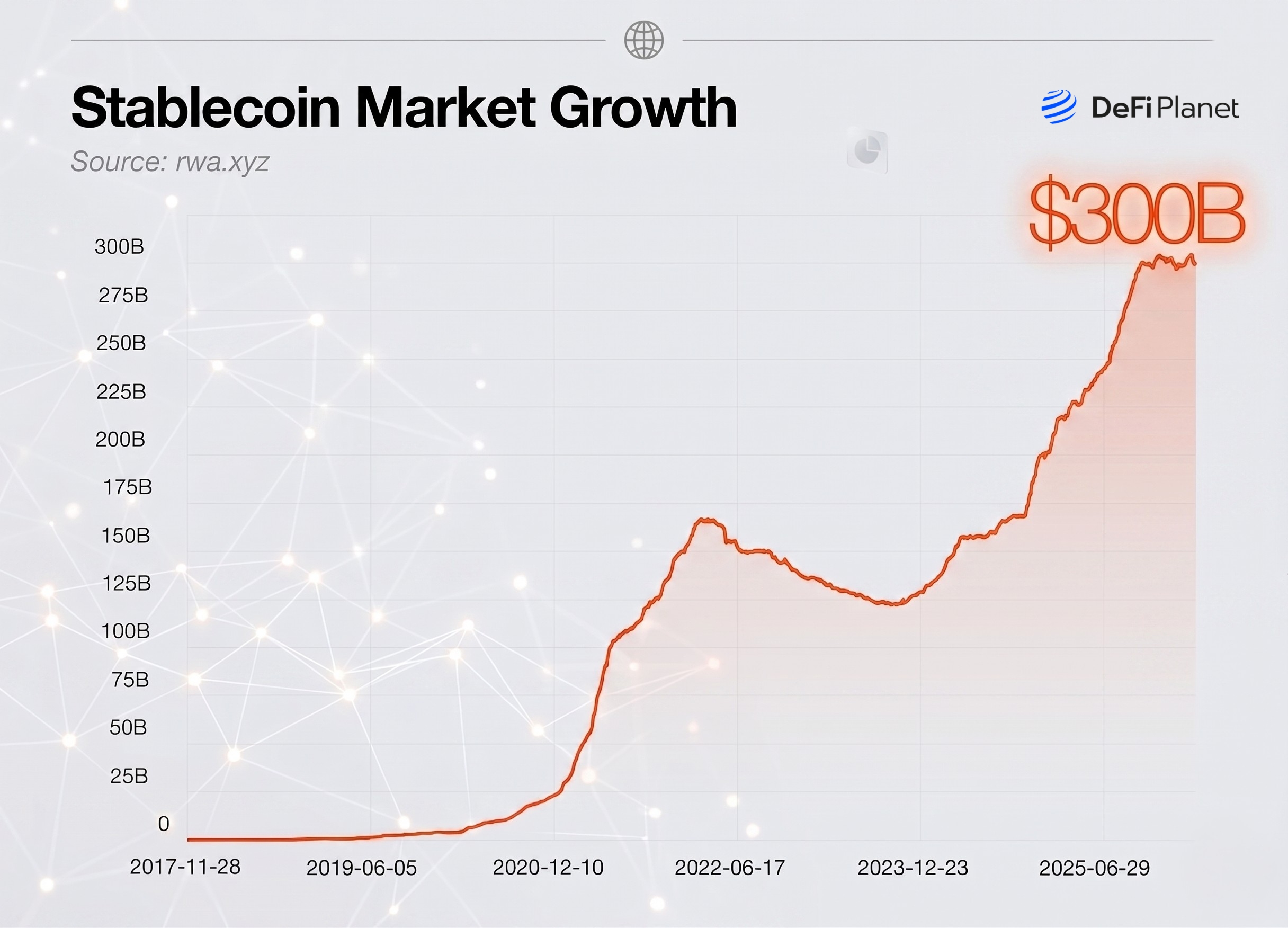

The total stablecoin market is now worth around $300 billion, making it a major part of global crypto liquidity.

While these assets are not official central bank money, they are increasingly used for cross-border transfers and crypto trading, effectively acting as a “bridge currency” in global payments. This raises concerns that settlement activity could gradually shift away from traditional euro-based systems.

The ECB’s worry is not just about competition, but control. If more global payments settle in private stablecoins instead of euros, it could gradually reduce the euro’s role in international finance. In other words, even if people still use euros in Europe, global digital flows could start to run on dollar-linked systems instead.

Tokenized payments are seen as a way to respond to this change. By representing money and deposits on blockchain-based systems within regulated European infrastructure, settlement can remain within supervised financial rails rather than moving to private, offshore networks. This keeps more payment activity within the European system, even as technology changes.

Beyond strategy, tokenization also solves practical problems. It can speed up payments, reduce delays in cross-border transfers, and enable transactions to run 24/7 rather than only during banking hours. It also makes payments programmable, meaning money can move automatically when conditions are met, and it improves interoperability between banks and financial institutions that currently use different systems.

Chiara Scotti’s Argument for Tokenized SEPA Payments

Bank of Italy Deputy Governor Chiara Scotti has become one of the key voices pushing Europe to take tokenized payments more seriously. In a recent speech at a workshop on ‘Digital Assets and Monetary Policy Transmission’ held in Rome, she argued that Europe should not wait too long before modernizing payment systems like SEPA for the tokenized economy.

Scotti believes Europe should actively explore tokenized SEPA payments as a way to modernize financial infrastructure while still keeping the euro at the center of European payments. Instead of allowing private stablecoins to become the default digital money layer, Europe could create tokenized payment rails connected to regulated banks and central bank settlement systems.

One of Scotti’s biggest concerns is preserving the euro’s competitiveness in a world where digital payments are becoming more global and blockchain-based. If businesses and users increasingly settle transactions in dollar-backed stablecoins rather than euro-based systems, the euro could slowly lose influence in digital commerce and international finance.

The deputy governor also warned about fragmentation. Right now, many tokenized payment systems are developing separately across banks, stablecoin issuers, and blockchain networks. Without coordination, Europe could end up with disconnected systems that do not work smoothly together. Scotti argues that Europe needs interoperable infrastructure so tokenized payments can move across institutions without breaking the “singleness” of money.

Another major point in Scotti’s argument is the importance of keeping central bank money relevant in tokenized finance, as trust in money ultimately depends on trusted institutions and settlement systems. If more financial activity moves onto blockchains, Europe wants that system to remain anchored to regulated banking infrastructure and central bank settlement rather than fully shifting toward private digital currencies.

Appia’s Role in Europe’s Long-Term Tokenization Strategy

The ECB’s Appia project is part of Europe’s broader plan to prepare its financial system for a tokenized economy. The project is tied to the ECB’s wider strategy of building an integrated digital financial ecosystem by around 2028, where tokenized assets, digital payments, and blockchain-based settlement systems can operate within regulated European infrastructure.

The main goal is to create a framework that allows different forms of digital money to work together safely. This includes tokenized bank deposits, stablecoins, and central bank money existing within the same financial environment instead of competing in completely separate systems.

One major focus is interoperability. Europe wants banks, payment providers, and financial platforms to be able to exchange tokenized assets and payments smoothly across networks. Without a common infrastructure, tokenized finance could become fragmented, where each institution runs isolated systems that cannot easily connect with others.

Appia also reflects Europe’s attempt to prevent private stablecoins from becoming the dominant settlement layer for digital finance. By creating infrastructure that keeps settlement linked to regulated financial institutions and central bank systems, Europe hopes to maintain monetary control while still supporting innovation.

The project’s importance spans beyond just payments because tokenization could eventually affect much wider parts of finance. Tokenized systems may later be used for bonds, securities, trade finance, collateral management, and cross-border settlement.

Is Appia Already Solving the Problem?

Appia directly addresses many concerns raised by Chiara Scotti because its entire goal is to keep Europe’s financial system connected to central bank money while preparing for tokenized finance. The project focuses heavily on interoperability, common standards, and reducing fragmentation between banks, tokenized deposits, and digital settlement systems.

However, major gaps still remain. Appia’s full blueprint is not expected until 2028, while private stablecoin issuers and US-linked digital payment systems are expanding globally much faster. Europe also still faces challenges around interoperability between different DLT networks, fragmented legal frameworks across member states, and slower institutional decision-making.

The risk is that by the time Europe fully builds its tokenized infrastructure, dollar-backed stablecoins may already be deeply embedded in global digital payments and settlement flows, making it harder for euro-based systems to catch up.

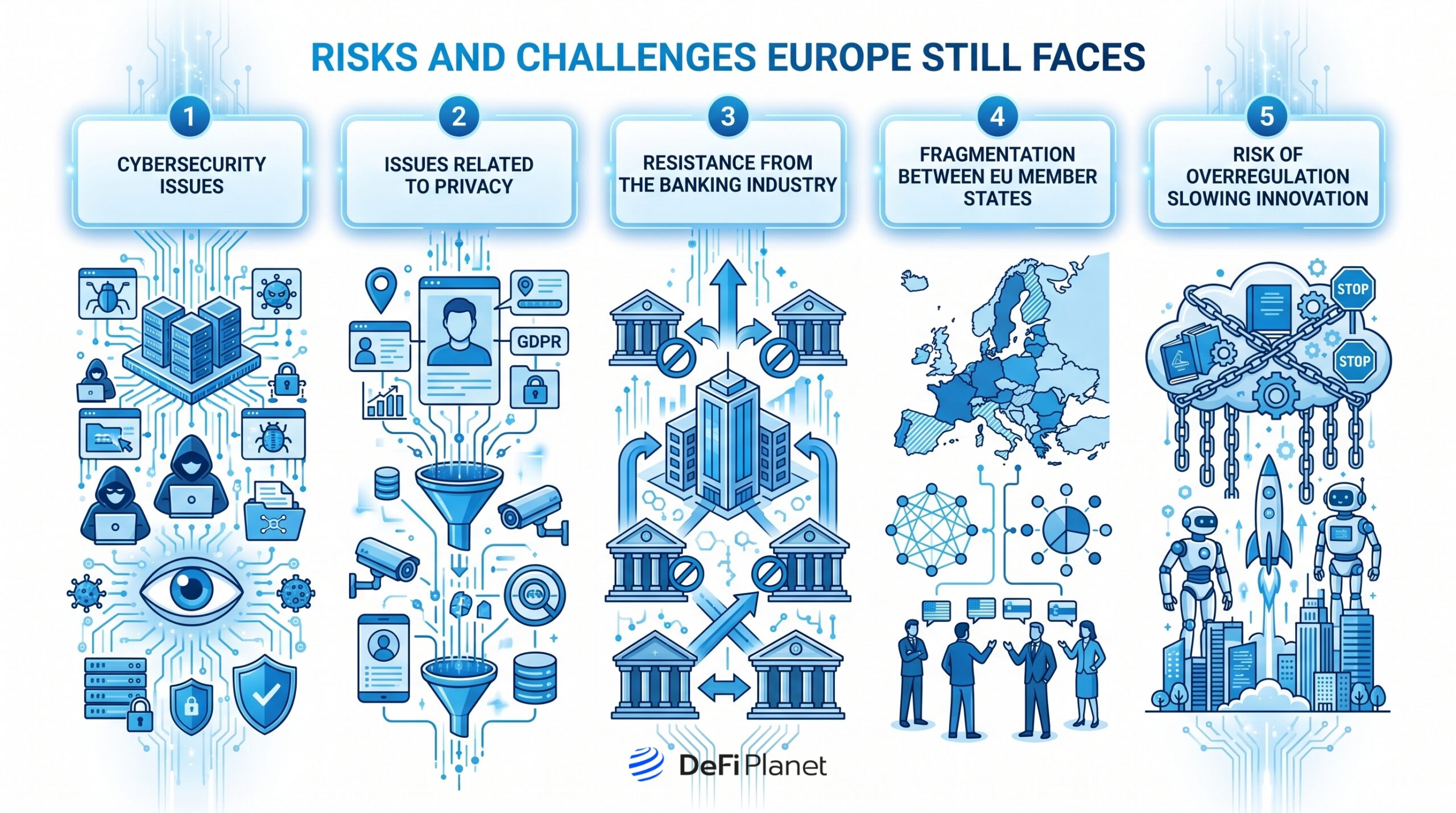

Risks and Challenges Europe Still Faces

Even though tokenization of SEPA payments would be useful in improving the European financial sector, the following challenges continue to hinder this region:

Cybersecurity issues

With an increasing trend towards digitalizing and using blockchain for payments, there will be increased exposure to cyber attacks. Such attacks on payment infrastructure, if they occur, can undermine public confidence in Europe’s digital payment project.

Issues related to privacy

With regards to transaction tracking, tokenization of payments would be a big advantage, but at the same time, it creates privacy issues for end-users. In particular, European regulators are striving to achieve a proper balance between financial monitoring and the protection of personal financial information. While it is important to develop solutions that protect against fraud and financial crimes, users at the same time must not feel as if they are being monitored all the time.

Resistance from the banking industry

Traditional banks might resist using tokenization technology, even silently, due to its ability to undermine their control over payments and their settlement. In cases where customers have an opportunity to make transactions faster than before using tokenization or any other fintech services, then banks will lose some of their power over the payment process.

Fragmentation between EU member states

While SEPA has managed to standardize euro-based transactions, there is still fragmentation when it comes to legal and regulatory differences between different countries within Europe. This could slow down Europe’s ability to compete with more centralized systems developing in the US or Asia.

Risk of overregulation slowing innovation

Europe has long been recognized as the most tightly regulated continent when it comes to financial transactions, but nowadays, the threat of overregulation is growing stronger because of the possible hindrance that it might bring to innovations. If the issuance of tokenized financial products becomes too complicated in the region, it would make logical sense for businesses to find greener pastures.

Glimpsing Into the Future of Digital Finance in Europe

Tokenized SEPA payments is a valid milestone in developing a digital finance system in Europe, which does not automatically imply abandoning traditional payment systems in favour of innovation.

With proper use of tokenization technology, Europe might just be able to combine both worlds, i.e., develop a more efficient payment network while preserving connections to the current system of money transfers.

The main problem lies in finding the optimal balance between innovation, supervision, financial stability, and competitive position in the international financial market. While Europe would like to encourage innovation in financial technologies, it still needs to maintain tight regulation and consumer protection.

Too slow progress in this case will leave the space open to the dominance of American stablecoin issuers and foreign fintech businesses, whereas overly rapid developments may entail various risks for both banks and financial markets.

In any case, the result of this delicate balance may affect Europe’s global monetary power in the future, particularly considering the increasing popularity of cross-border payments, tokenization of assets, and blockchain settlements across the world.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.”