In April 2026, Hong Kong’s monetary authority received 36 applications for stablecoin licenses and approved two. Across the Atlantic, out of more than 1,200 crypto firms previously registered across the European Union, roughly 210 secured full MiCA authorization. Tether, the issuer of the world’s largest stablecoin, was not among them. Major exchanges responded by delisting USDT for European users entirely.

Cryptoasset regulation, at least in major economies, has come out of the dark age. So the question now is what regulatory environments are worth investing into, and which firms can afford to navigate them. MiCA authorization costs a typical EU crypto business between €300,000 and €700,000 within a year. A Singapore or Hong Kong institutional license can reach $400,000 before factoring in operational costs. Expensive, but for many firms, worth paying to gain access to markets where serious capital is now concentrating.

What we have now, a global landscape where jurisdictions are competing as actively as the firms operating within them. Europe is using harmonization as a competitive moat. The United States is reshaping agency boundaries to attract institutional participation. The UAE has built a multi-zone licensing architecture designed to give firms options rather than obstacles. Each model reflects a different theory of how to win the next phase of crypto’s development. H1 2026 is where those theories started producing measurable results.

TL;DR

- Out of more than 1,200 crypto firms previously registered across the EU, roughly 210 secured full MiCA authorization, an 18% conversion rate that signals how decisively the regulation is reshaping who can compete in Europe’s market

- Tether’s USDT remains shut out of EU-regulated markets after declining to pursue MiCA authorization, making Circle’s USDC and EURC the only top-ten stablecoins authorized for EU distribution

- A MiCA authorization costs a typical EU crypto business between €300,000 and €700,000 in year one, with €150,000–€250,000 in annual ongoing costs, making compliance an economic filter as much as a legal one

- The U.S. is moving from enforcement-led regulation toward formal market structure, with the CLARITY Act passing the House and a new CFTC-SEC memorandum of understanding reshaping how agencies divide jurisdiction over digital assets

- Hong Kong received 36 stablecoin license applications and approved two, while ADGM reported 57% AUM growth and 13,353 active licenses in Q1 2026, reflecting how Asia is competing through selective, institution-focused licensing rather than broad access

- The UAE has distributed regulatory authority across five bodies, VARA, ADGM/FSRA, DIFC/DFSA, CMA, and CBUAE, giving firms multiple licensed entry points rather than a single approval gate

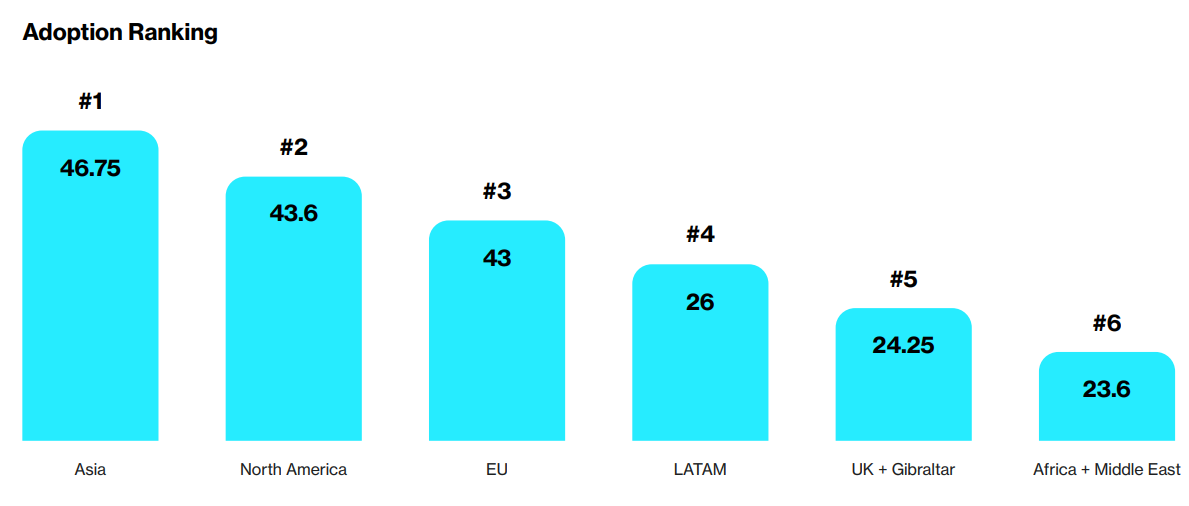

- Latin America ranked as the world’s fourth-largest crypto adoption region in H1 2026, with Brazil emerging as the most structurally regulated market following the implementation of Law 14,478

- Compliance is now functioning as a market-entry barrier globally, with institutional licensing costs ranging from €3,000 for basic EU registration to $400,000 for a Singapore or Hong Kong institutional license, before operational costs begin

Europe’s MiCA Era Has Moved From Regulatory Framework to Market Competition

The Markets in Crypto-Assets Regulation (MiCA) has shifted from a legislative framework into an active supervisory system shaping how crypto firms operate across Europe. Rather than remaining a policy framework on paper, it is now being applied through national regulators responsible for authorizing Crypt Asset Service Providers (CASPs) under a unified set of EU rules.

Implementation has focused on transitioning firms from fragmented national licensing regimes to a standardized compliance system. This means companies that previously operated under different national rules must now align with harmonized requirements covering governance, custody, capital adequacy, disclosures, and consumer protection.

While adoption is still in transition, early market data suggest a consolidation phase is underway. Out of more than 1,200 Virtual Asset Service Providers (VASPs) previously registered across the European Union, only 244 Crypto Asset Service Providers (CASPs) have secured full MiCA authorization across 23 EU member states as of June 2026, a conversion rate of under 20%. This shows how entry into the European market is becoming more structured and selective compared to the pre-MiCA environment.

What licensing, compliance, and passporting mean for companies

Under MiCA, licensing is issued at the national level by EU member state regulators, but it operates within a harmonized framework that enables “passporting” across the European Economic Area once authorization is granted.

This passporting mechanism is central to MiCA’s structure. A licensed CASP in one member state can expand services across all EU countries without applying separately in each jurisdiction. This reduces regulatory fragmentation while increasing the importance of securing initial approval.

Compliance requirements under MiCA are significantly more standardized than previous national regimes. Firms must demonstrate adherence to capital requirements, custody safeguards, operational resilience standards, and detailed reporting obligations. As a result, regulatory readiness has become a core operational requirement rather than a peripheral legal function.

Early signs of winners and challenges across European markets

Early implementation trends indicate that MiCA is already influencing competitive dynamics in the European crypto sector. Larger exchanges and established financial institutions are generally better positioned to meet compliance costs and operational requirements, while smaller providers face higher barriers to authorization.

At the same time, regulatory enforcement and licensing requirements are beginning to determine market access. Firms operating in Europe are increasingly required to either secure MiCA-aligned authorization or restructure their services to remain compliant within specific jurisdictions.

This is gradually centralizing activity around firms with stronger regulatory infrastructure, compliance capacity, and institutional relationships, while increasing pressure on smaller or less regulated entities to adapt or exit certain markets.

No outcome illustrates this more clearly than the stablecoin market. Tether’s USDT, the largest stablecoin by market cap globally, remains effectively shut out of EU-regulated markets after Tether declined to pursue MiCA authorization. In response, major licensed exchanges moved systematically: Coinbase began delisting USDT for EEA users in December 2024, Kraken followed in early 2025, Crypto.com delisted it alongside nine other tokens, and Binance applied geofencing across all EEA USDT pairs.

Circle, by contrast, secured full MiCA compliance for both USDC and EURC, making them the only top-ten stablecoins authorized for EU distribution. Tether CEO Paolo Ardoino defended the decision, arguing that MiCA’s requirement to hold 60% of reserves in European banks could trigger simultaneous banking and stablecoin instability. Whatever the merit of that argument, the practical outcome is that MiCA has already reshaped which stablecoins can circulate in the world’s largest single regulated crypto market, and in favor of the issuers that chose compliance over resistance.

The United States Is Moving From Enforcement Toward Market Structure

The U.S. crypto space is moving from an enforcement-driven approach toward a structured framework focused on defining market rules, agency jurisdiction, and asset classification.

In early 2026, U.S. lawmakers significantly advanced the Digital Asset Market Clarity Act (CLARITY Act), a comprehensive market structure bill aimed at formally defining when crypto assets fall under SEC or CFTC jurisdiction, including clearer classification of tokens as securities or commodities and expanding the CFTC’s authority over spot crypto markets.

The SEC issued updated interpretive guidance in March 2026, clarifying how federal securities laws apply to crypto activities such as staking, airdrops, and protocol participation, signalling a shift toward rule clarification rather than enforcement-led definition.

Regulators have also formalized a new CFTC–SEC Memorandum of Understanding, shifting from episodic cooperation to structured coordination. This increased alignment includes joint efforts to reduce jurisdictional overlap between securities and derivatives markets, improving regulatory clarity for firms operating across both regimes.

The CFTC has reduced broad enforcement activity in favour of targeted fraud prevention and clearer compliance guidance, signalling a structural shift in how crypto-related cases are handled.

How market structure debates are influencing business decisions

Legislative efforts building on the FIT21 framework continue to shape business strategy by defining how digital asset regulations are categorized and which agency governs them, influencing how exchanges, custodians, and issuers structure their operations in the U.S. market.

The FIT21 model, still serving as the foundation for current proposals, introduces a dual system in which the SEC oversees securities tokens and the CFTC regulates digital commodities, providing firms with a clearer framework for product design and compliance planning.

Market proposals increasingly favour assigning the CFTC broader authority over spot crypto markets, which directly affects how exchanges structure listings, custody arrangements, and trading venues in the U.S.

The growing role of politics in shaping crypto policy

Political appointments and Senate confirmations for key regulatory roles, particularly leadership at the CFTC and the SEC, have become central to U.S. crypto policy direction.

The December 2025 confirmation of Michael Selig as CFTC Chair illustrated how directly personnel decisions now shape crypto policy direction. Selig, who previously served as chief counsel of the SEC’s Crypto Task Force, entered the role with an explicitly pro-crypto posture, describing his regulatory philosophy as the ‘minimum effective dose of regulation.’ His confirmation effectively signalled the CFTC’s intent to position itself as the primary overseer of spot digital commodity markets, a stance that has shaped how exchanges, custodians, and trading platforms approached compliance planning throughout H1 2026.

Cryptocurrency legislation is becoming increasingly politicized within Congress, where significant pieces of legislation, such as the CLARITY Act, have been passed in the House but not in the Senate due to the inability to resolve significant disagreements about regulatory jurisdiction and authority, DeFi regulations, and the risks to traditional banking posed by stablecoin yields.

The dynamics within the Senate are further influenced by election cycles that limit enthusiasm for comprehensive financial legislation. Indeed, even when committees such as the Senate Banking Committee pass legislation to the Senate floor, votes can easily turn out to be partisan.

Related: What Phase Is the Global Push to Regulate Crypto Entering?

The UAE and Middle East Are Building a Competitive Crypto Hub Model

Unlike the US and Europe, the Middle East region, led by the UAE, takes a different stance on crypto regulation.

As of June 2026, there were a total of 100 virtual asset licenses issued in the UAE among five regulatory bodies in the country; these include VARA, ADGM/FSRA, DIFC/DFSA, the Capital Market Authority (CMA), and the Central Bank (CBUAE).

Unlike other nations with a single regulatory body for the entire nation’s crypto sector, the UAE has adopted a multiple-zone approach, allowing companies to select the regulatory regime based on their business model through VARA.

Role of licensing, business incentives, and regulatory certainty

In 2026, the UAE significantly expanded its regulatory architecture for cryptocurrencies. The federal government replaced the former VASP framework with a Capital Market Authority regime and introduced eight categories of crypto activities and a capital requirement from AED 500,000 to AED 4 million. Also, VARA, DFSA, ADGM, and CBUAE changed their regulations simultaneously.

The licensing model now separates responsibilities by activity:

- CBUAE oversees payment tokens and stablecoins

- VARA regulates virtual asset services in Dubai

- DFSA governs crypto activity inside DIFC

- ADGM supervises digital asset financial services

This structure provides regulatory certainty while giving firms multiple routes to market entry.

Early signs of regional market expansion

ADGM’s Q1 2026 results reflect the pace of that expansion in concrete terms. According to the centre’s official May 2026 report, total active licenses reached 13,353, with 961 new licenses issued in the first three months of 2026 alone, representing a net increase of 2,783 licenses since Q1 2025. The number of operational entities grew 34.52% year-on-year to 3,741, while regulated financial services entities rose 30% to 365. Assets under management jumped 57%, supported by the entry of major global firms, including Capital Group, Man Group, Bain Capital, and Barings, collectively representing over $4.4 trillion in global AUM. The Financial Services Regulatory Authority also issued 29 new Financial Services Permissions during the quarter, a 45% increase compared to the same period in 2025.

In 2026, despite geopolitical uncertainty in the broader region, crypto firms operating within UAE financial centres continued without significant disruption, a sign that the jurisdiction’s regulatory architecture and digital-first infrastructure have provided meaningful operational stability.

Hong Kong and Singapore Are Competing Through Controlled Openness

Hong Kong moved into execution mode in H1 2026, operationalizing its stablecoin licensing regime under the Stablecoins Ordinance.

Two stablecoin issuers were granted their licenses by the HKMA to HSBC and Anchorpoint Financial in April 2026. This represented the beginning of the first stage in the operation of its regulated stablecoin market. Only two out of 36 applications received licenses in the first round, showing a careful selection process.

The regulatory perimeter of Hong Kong was expanded beyond the exchanges with new licensing plans for dealers and custodians of digital assets, as well as tokenized bonds and digital asset liquidity.

Singapore entered 2026 with an already mature model and without any additional legislation. The Singaporean model ran on the same licensing regime in accordance with the Payment Services Act, along with the regulation of digital payment token services, stablecoins, custody, and institutional market practices.

Approaches to balancing innovation with oversight

Hong Kong’s approach has become increasingly interventionist. Innovation is permitted, but inside tightly defined regulatory channels.

The HKMA emphasized a “same activity, same risk, same regulation” principle and limited approvals despite broad market interest. There are reserve criteria, controls around redemption, and regulations for governance and oversight when issuing stablecoins.

In Singapore, there’s another approach. Rather than controlling innovation by way of strict approvals, MAS places an emphasis on supervision, capital standards, asset segregation, and disclosure while innovating within a regulated environment.

This leads to two forms of controlled openness:

- Hong Kong: permissioned growth through selected approval

- Singapore: expanded participation through ongoing supervision

Competition for institutional capital and regional leadership

Competition between the two markets is increasingly focused on institutional funding rather than consumer adoption.

Hong Kong has started to incorporate banks into digital asset infrastructure, with HSBC looking to integrate stablecoins through payments and investments after getting regulatory approval. In this approach, digital assets will be seen as an integral part of the overall modernization of the financial market, not as a separate crypto ecosystem.

Hong Kong’s broader roadmap also includes the development of tokenization and liquidity solutions that aim to foster institutional involvement and capital generation.

Singapore continues to stay focused on its role as an institutional finance hub in Asia by incorporating digital assets into its already existing infrastructure for banking, payments, and capital markets.

Latin America’s Next Phase of Crypto Policy

The policies concerning cryptocurrencies in Latin America have moved on to a new stage. Previously, the development of the industry was mainly determined by consumer demand, volatility of local currencies, remittances, and lack of access to traditional finance. By 2026, Latin American governments will be trying to regulate this activity through licensing, regulation, and integration into the system.

Brazil has become the most structured market in terms of regulations in Latin America. Due to the introduction of Law 14,478 and amendments in regulations of the Central Bank, VASPs have to receive authorization, be regulated officially and meet certain requirements regarding AML, governance, and operations.

Across the region, approaches remain uneven. Brazil is emphasizing licensing and integration into the financial system, while markets such as Argentina, Panama, and El Salvador continue operating under different combinations of registration requirements, legal recognition, and financial supervision. Latin America increasingly looks like a collection of national frameworks rather than a unified regulatory market.

Role of inflation, payments, and financial inclusion in policy decisions

Economic conditions remain one of the region’s biggest policy drivers. In H1 2026, Latin America solidified its position as one of the world’s fastest-growing digital asset markets, ranking as the #4 global adoption region.

Argentina and Brazil have become two of the strongest examples of utility-driven crypto usage. Adoption has expanded not primarily through speculation, but through demand for dollar access, payments, and more predictable settlement mechanisms during periods of currency pressure and financial friction.

Drivers vary across the region: inflation protection remains stronger in Argentina and Venezuela, remittance demand is more important in Mexico and Central America, while Brazil’s growth is increasingly linked to payments and institutional financial integration.

This means crypto policy in Latin America is often being shaped less by innovation goals and more by broader economic questions around payments efficiency, dollar access, and financial inclusion.

Compliance Infrastructure Became a Competitive Advantage

As regulated crypto marketplaces began to grow in 2026, companies made sure that they were compliant in full. For a CASP in terms of MiCA, it is estimated that first-year operational and licensing costs would range from €300,000 to €700,000, and ongoing operating and compliance costs will continue even after licensing.

For smaller regulated firms, compliance itself has become a meaningful operating expense. Industry estimates show small EU CASPs spending approximately €150,000–€250,000 annually across legal support, compliance staffing, reporting, audits, monitoring technology, insurance, and regulatory obligations

Custody infrastructure has become another competitive layer. On average, the base fee charged annually for custody services provided by institutional custodians was 0.09% in 2024 and increased to 0.12% in 2025. Other fees related to insurance and control have also been accounted for. Custody is no longer considered as storage but rather a regulated utility service.

How compliance providers became part of crypto infrastructure

Compliance providers are increasingly functioning as infrastructure providers rather than external service vendors.

Identity verification, transaction monitoring, sanctions screening, blockchain analytics, reporting pipelines, and Travel Rule frameworks have become intrinsic parts of the exchange platform, custody services, and payment systems themselves, rather than add-ons.

Compliance analysis for the industry indicates that regulatory preparedness has moved from getting permission to go live to continuous monitoring, reporting, controls, and technical integration.

A new layer of infrastructure has been created in which compliance service providers are increasingly seen next to custodians, cloud providers, and settlement providers in the operational stack.

The growing cost of participating in regulated markets

The cost of entering regulated crypto markets has risen sharply. Depending on jurisdiction and business model, licensing structures now range from relatively low-cost registration frameworks to institutional-grade approvals that can reach hundreds of thousands of dollars once legal preparation, capital requirements, reporting systems, and operational controls are included. For example, Crypto license costs range from €3,000 for a basic European registration to $400,000 for an institutional license in Singapore or Hong Kong.

In the U.S., high-regulation environments remain among the most expensive. Estimates for operating under New York’s BitLicense framework place total upfront preparation and implementation costs into six-figure ranges or higher, with continuing annual regulatory and operational expenses.

The result is that compliance is increasingly acting as an economic filter. Regulation is no longer simply determining who is allowed to operate, it is increasingly determining who can afford to compete.

The Regulatory Race Is No Longer About Permission, It’s About Positioning

The biggest regulatory question in crypto has changed. The debate is no longer whether governments will regulate digital assets, but which regulatory models will attract companies, retain capital, and build durable financial ecosystems. Different regions are increasingly competing using different means: Europe through harmonization of regulations; United States through designing its market structure; UAE through regulatory specialization; Asia through controlled openness. Regulation is becoming an economic tool, not just a supervisory one.

The next phase of competition will likely depend less on who moves fastest and more on who builds the most usable system. Markets that combine clear rules with efficient licensing, scalable compliance infrastructure, and access to liquidity are increasingly becoming the preferred destinations for long-term crypto activity. In that environment, regulatory clarity alone is no longer the advantage, execution is.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.

{kind=link}