In May 2026, Mastercard agreed to acquire BVNK, a stablecoin payment infrastructure firm, for up to $1.8 billion. A few weeks earlier, OKX launched a stablecoin payment card for European users through Mastercard’s own network. Both of these were payment infrastructure stories that happened to involve stablecoins, which is precisely the point.

It is mid-2026, and stablecoins have quietly become the settlement layer that most global finance players are now building infrastructure on top of. At the time of writing, USDT’s market cap sits at $186.3 billion. USDC’s is $74.9 billion. Filtered real payment flows through stablecoin rails reached $4.5 trillion monthly in Q1 2026 alone. Nigeria accounted for roughly 60% of all stablecoin inflows into sub-Saharan Africa. In the US, the Federal Reserve and four other federal agencies have proposed joint rules requiring stablecoin issuers to operate as regulated financial institutions with bank-grade compliance programs.

Stablecoins are now competing seriously as monetary infrastructure, which is why regulators, central banks, payment networks, and corporate treasuries are all paying rapt attention to the sector.

TL;DR

- Stablecoin supply reached a combined $261 billion across USDT ($186.3B) and USDC ($74.9B) by mid-2026, with both issuers expanding beyond exchange liquidity into institutional settlement and payment infrastructure

- Real payment flows through stablecoin rails hit $4.5 trillion monthly in Q1 2026 on a filtered basis, excluding bot-driven activity, while total unfiltered on-chain volume exceeded $28 trillion for the quarter

- Mastercard agreed to acquire stablecoin infrastructure firm BVNK for up to $1.8 billion, while OKX launched a stablecoin payment card through Mastercard’s network, signaling mainstream payment infrastructure’s direct move into stablecoin rails

- The yield-bearing stablecoin sector grew to roughly $22.7 billion by early 2026, led by products like sDAI, USDY, and sUSDe, as issuers shifted from competing on stability alone to competing on yield

- Nigeria accounted for roughly 60% of all stablecoin inflows into sub-Saharan Africa, while Latin America’s remittance market reached $174 billion in H1 2026, with stablecoins capturing a growing share of cross-border flows

- The U.S. GENIUS Act and joint federal agency proposals now require stablecoin issuers to operate as regulated financial institutions with 1:1 reserve backing and bank-grade AML controls, marking the shift from crypto oversight to payment system oversight

Growth in Stablecoin Supply and Transaction Activity

Stablecoin supply has continued to grow steadily up to the end of H1 2026, led by major issuers: USDT and USDC. Both control an estimated 83% of the total stablecoin market capitalization, which sits at a record-breaking valuation of approximately $315 billion

Tether’s USDT remains the largest stablecoin by market share, with supply continuing to expand alongside global demand for dollar liquidity in crypto markets. According to market data, USDT supply has a market cap of $186.3 billion and a circulating supply of $186.47 billion in June 2026, maintaining its position as the primary trading and settlement asset across exchanges.

USDC is also expanding its presence across institutional and regulated markets as it is increasingly used in payment rails, treasury operations, and tokenized settlement systems. In June 2026, the USDC market cap reached $74.91 billion with a circulating supply of $74.92 billion.

Increase in on-chain transaction volume and settlement activity

Beyond supply growth, perhaps the most notable trend in 2026 has been in transaction usage. Stablecoins are now moving beyond exchange trading pairs and are now used for:

- On-chain settlement between institutions

- DeFi liquidity routing

- Treasury and cash management flows

- Increased cross-border payments

In Q1, stablecoins set a monthly transfer volume record of $4.5 trillion (with nearly two-thirds of that volume originating from Asia).

Stablecoins Are the Core Liquidity Layer for Crypto Markets

Most crypto trading today is effectively priced through stablecoins.

On most centralized exchanges, major assets like Bitcoin and Ethereum are largely quoted and settled against USDT and USDC pairs rather than fiat. This makes stablecoins the default unit of liquidity, not just a trading alternative.

On-chain, the same structure appears in DeFi liquidity pools. Stablecoin pairs (like USDC/ETH or USDT/ETH) dominate automated market makers because they reduce volatility risk for liquidity providers and allow tighter spreads.

Academic analysis of stablecoin market structure shows that they serve as the primary bridge between fiat and crypto liquidity, enabling continuous pricing and reducing friction across trading environments.

In practice, this means:

- If stablecoin liquidity is deep, markets trade smoothly

- If stablecoin liquidity tightens, spreads widen across almost every asset

Stablecoins have also become the settlement layer between market participants, not just trading assets.

On centralized exchanges, stablecoins allow near-instant movement of capital between accounts, reducing reliance on traditional banking rails that can take hours or days to clear.

On decentralized exchanges, settlement is fully on-chain, meaning trades finalize in minutes or seconds, depending on network conditions.

Market efficiency in crypto is now closely tied to how deep stablecoin liquidity is across venues. When stablecoin reserves are high, markets can absorb large trades without sharp price dislocations. When stablecoin liquidity contracts, even moderate flows can create outsized volatility.

Cross-Border Crypto Payments and Real-World Usage Expansion

One of the strongest growth areas for stablecoins is cross-border remittances. In emerging markets like Africa and Latin America, users are increasingly using dollar-pegged stablecoins to send and receive money across borders because they settle faster than traditional banking rails and have lower remittance fees.

A recent IMF report found that Nigeria received about $59 billion in crypto-asset inflows between mid-2023 and mid-2024, and that the country has accounted for roughly 60% of all stablecoin inflows into sub-Saharan Africa since 2019.

Latin America is also becoming a major stablecoin remittance market. The region’s remittance flows reached about $174 billion, and stablecoins are increasingly used as an alternative to traditional money transfer services for faster settlement and lower costs.

How Stablecoins are Increasingly Used Outside Trading Environments

Perhaps the biggest structural change in 2026 is that stablecoins are no longer confined to exchanges. Institutional payment providers and fintech platforms are integrating stablecoin rails into their infrastructure to support real-time global payments.

OKX recently launched a stablecoin payment card for European users through Mastercard’s network. Mastercard also expanded its stablecoin infrastructure by agreeing to acquire BVNK in a deal worth up to $1.8 billion.

They are now used in:

- Payroll and contractor payments

- e-commerce settlements

- Remittances and family transfers

- Treasury and liquidity management for firms

- Cross-border B2B payments

Yield-Bearing Stablecoins and Product Innovation

Stablecoins are no longer competing for stability and distribution advantages. We’re now entering a new phase where issuers are competing over how to make their stablecoins earn without compromising their usability in the crypto market.

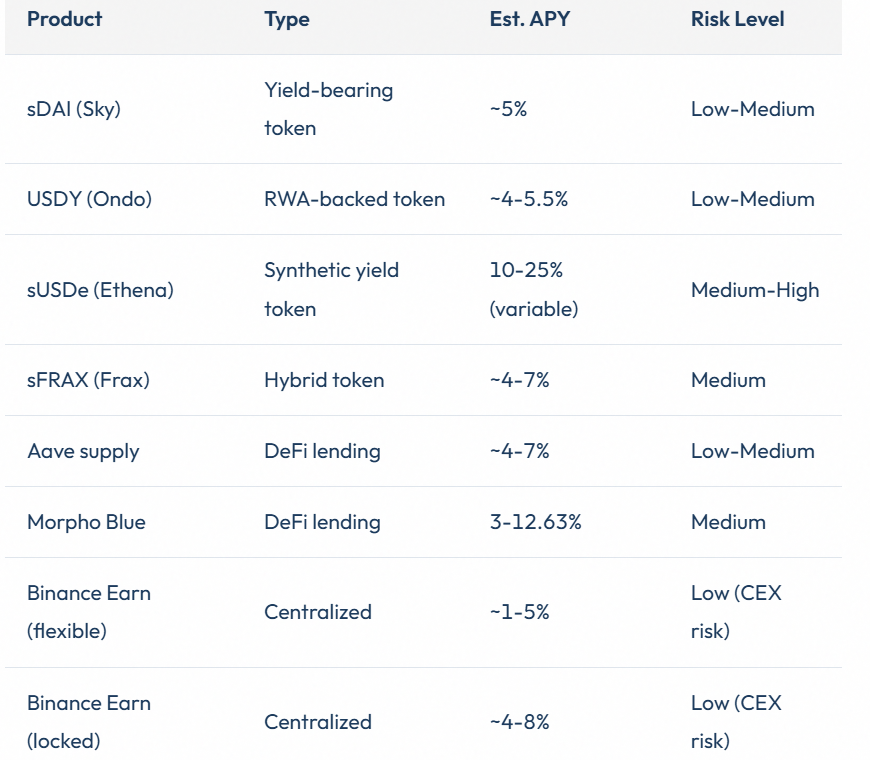

The most important stablecoin topic in 2026 is undoubtedly the emergence of yield-bearing stablecoins, which are stable assets created in order to provide dividends to holders. In contrast to classic stablecoins (like USDT and USDC), which generally operate as digital cash, yield-bearing models offer the opportunity to earn a profit simply by holding the token.

There are various instruments available, including government bond yields, DeFi lending opportunities, and even trading-based yield schemes. Such products as sDAI (Sky/Maker), yielding around 5% due to its Treasury-based saving scheme, USDY (Ondo Finance) with 4.5% yield due to U.S. Treasury exposure, sFRAX (Frax) with yields close to 5%, and sUSDe (Ethena) providing various variable yields from 8% to almost 30% via basis-trading schemes.

By early 2026, the yield-bearing stablecoin sector had grown to roughly $22.7 billion, expanding much faster than the broader stablecoin market. Much of this growth has come from issuers competing to offer returns through different income models rather than simply maintaining price stability.

Risks and opportunities created by yield-based designs

Yield-bearing stablecoins create new opportunities, but they also introduce new trade-offs.

The opportunity is obvious: idle capital becomes productive. Users can earn yields on their stablecoins without locking up these assets solely for settlement purposes.

However, yield adds another dimension to risks.

Stablecoin return generation can create tension between maintaining stability and taking enough risk to remain competitive. Different yield sources also carry different stress behaviour during volatile conditions.

Examples of risk include:

- Yield compression during changing market conditions

- Collateral quality deterioration

- Smart contract and protocol exposure

- Depeg risk during periods of stress

In simple terms, the higher the promised yield, the more important it becomes to understand where that yield actually comes from.

Regulatory Attention Across Key Jurisdictions

Stablecoin regulation has shifted from fragmented oversight to a more structured global framework. But instead of a single global rulebook, what has emerged is a three-speed system: the US focusing on federal licensing and reserves, the EU tightening MiCA enforcement, and Asia maintaining a more fragmented but innovation-driven approach.

Across all regions, the common focus is the same: reserves, transparency, redemption rights, and systemic risk control.

United States: From uncertainty to federal stablecoin rules

The United States is in a new phase of regulation with the passage of stablecoin regulations at the federal level, such as the GENIUS Act, which imposes the obligation of 1:1 collateralization, monthly attestations, and licenses for issuers over major circulating amounts.

In this system,

- Stablecoins are regarded as payment mechanisms, rather than investment commodities

- Issuers have to have high-quality reserves (cash and short-term Treasury bonds)

- Big issuers fall under federal regulation. Small ones can work under state regulation

The overall aim is to minimize risks and keep stablecoins an integral part of the US dollar payment system. The US approach is not restricting stablecoins outright, but formalizing them into a regulated financial product class.

European Union: MiCA remains the global benchmark

In the EU, MiCA is fully operational and marks the most developed stablecoin regime in the world at present. Stablecoins are considered e-money tokens with strict criteria regarding redemption rights, reserve backing, and issuance licenses.

Main points include:

- 1:1 reserve backing in liquid instruments

- Compulsory redemption at par value

- Issuers licensed as regulated financial institutions

- Enhanced regulation of stablecoins that are systemically important

However, there is the problem associated with systemic risk owing to spillover effects, particularly in cases of cross-border stablecoins, which may be issued in another jurisdiction, yet redeemable in the European Union. Regulators have expressed fears that this mechanism can cause problems with EU reserves during stress periods.

Moreover, certain rules, like limitations on transactions in non-EU-denominated stablecoins, demonstrate that the EU is actively working on scale control in order to mitigate financial stability risks. The model of the EU is focused on financial stability despite the limitation of growth possibilities.

Asia: Fragmented regulation with selective openness

Asia’s regulation is much more diverse and fragmented.

- Singapore and Japan are still supporting the licensed models for stablecoins, focused on payment use cases

- Hong Kong is developing an approach that includes licensing and is aimed at positioning the jurisdiction as a regional hub of digital assets

- Other territories tend to be either cautious or partially restrictive due to their capital controls and monetary policy considerations

Unlike in the US and Europe, Asia is less unified. Asia operates as a network of separate national frameworks that balance innovation and capital-flow management.

Is regulation enabling or restricting stablecoin growth?

The answer is both, depending on the region and the issuer types.

First, regulation facilitates the development of stablecoins as it:

- Provides legal certainty for using stablecoins

- Involves banks, fintech firms, and asset managers in the stablecoins ecosystem

- Imposes standards in terms of reserves and redemptions

At the same time, it restricts the expansion of stablecoins, as:

- It increases the costs of compliance for issuers

- It limits the way stablecoins are scaling across jurisdictions

- It implies divergent rules across jurisdictions, thus fragmenting the global usage

RELATED: The Crypto Market Runs on Stablecoins—Whether Regulators Like It or Not

Stablecoins in Emerging Use Cases Beyond Trading

Stablecoins are no longer expanding just because people want a place to park capital between trades. Growth is increasingly coming from new crypto-native applications that need a stable unit of account to function continuously and predictably.

Expansion into DeFi, gaming, and automated settlement systems

DeFi continues to be among the largest stablecoin demand drivers, although the use of stablecoins in the DeFi space has changed. Gaming and consumer applications are also starting to adopt stable settlement models.

Companies such as Sony’s Soneium ecosystem, Stripe, PayPal, and gaming-focused blockchain platforms like Immutable are expanding stablecoin and blockchain payment infrastructure to support in-app purchases, digital commerce, creator payments, and more predictable settlement across consumer applications.

Moreover, automated settlement systems are gaining significance. Stablecoins enable applications to make transfers, payments, and treasury management actions 24/7, regardless of the banking schedule.

Industry estimates reveal that stablecoins are transforming into a payment rail rather than an auxiliary infrastructure for crypto operations. The transaction volume on stablecoin rails exceeded $28 trillion in unfiltered stablecoin transaction volume (76% of which were bot-driven activity) in Q1 2026, which means that the annualized transaction volume might amount to $40-46 trillion.

This means that settlement operations are also becoming one of the main products offered by the stablecoin ecosystem.

Why Usage is Diversifying Beyond Traditional Transfers

Stablecoins are expanding beyond transfers because they solve multiple problems at once.

They combine:

- Price stability

- Continuous settlement

- Programmability

- Global accessibility

That combination makes them useful anywhere value needs to move quickly and predictably.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.

{kind=link}