Discourse on Bitcoin has followed a familiar script over the years because its supporters often refer to it as digital gold. Investors argued over whether it could replace traditional stores of value, while economists debated whether it even deserved to be treated as a serious financial asset. We’re in H1 2026, and those arguments have taken a backseat, the market has moved forward, and investors would rather spend their time deciding how best to use Bitcoin.

Market participants seem to have grown weary of endless philosophical discussions and are now focused on reality. The most important developments surrounding Bitcoin have come from investor actions rather than investor opinions, and while institutional capital continued flowing into regulated investment vehicles, portfolio managers began to view Bitcoin through the lens of allocation decisions. Sovereign entities remained part of the conversation with asset managers comparing Bitcoin against gold, equities, commodities, and currencies rather than evaluating it in isolation.

ETFs Changed the Nature of Bitcoin Demand

No development shaped Bitcoin’s investment landscape more than the continued growth of exchange-traded funds (ETFs). The arrival of spot Bitcoin ETFs in the United States created a bridge between traditional finance and digital assets, a bridge that became even more important throughout the first half of the year.

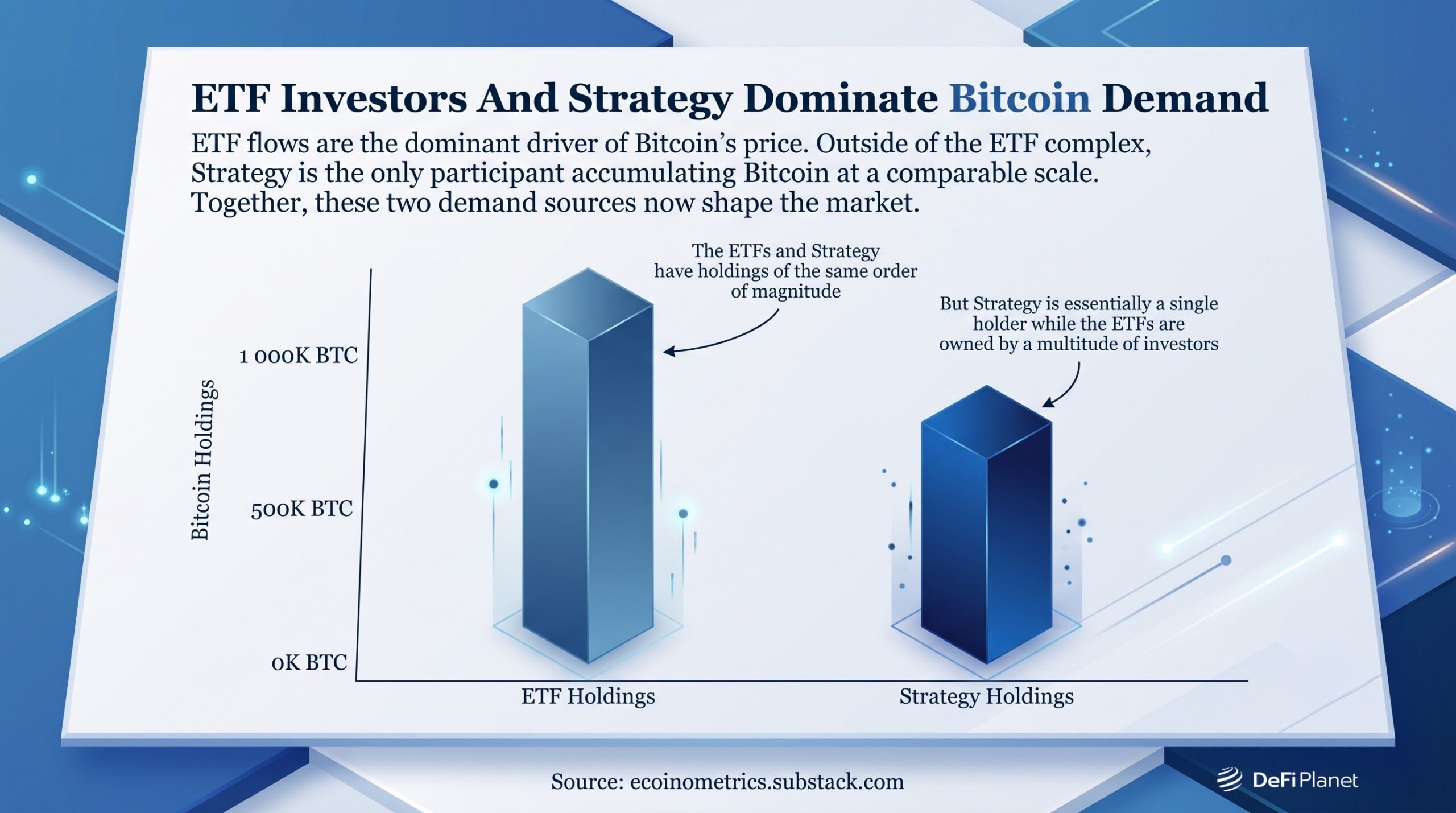

As at mid-2026, US spot Bitcoin ETFs collectively held more than 1.2 million BTC, a significant portion of Bitcoin’s circulating supply. Several industry analyses estimated total assets under management at around $102 billion, highlighting the growing influence of regulated investment vehicles on Bitcoin markets. Their importance lies not only in the size of these holdings but also in the fact that they have created a regulated gateway for pension funds, wealth managers, and other institutional investors to gain exposure to Bitcoin without directly holding the asset. Before ETFs existed, institutions interested in Bitcoin often faced operational challenges related to custody, compliance requirements, internal risk controls, and reporting standards, but ETFs simplified the process.

Instead of managing private keys or establishing specialized crypto infrastructure, investors could gain exposure through familiar financial products traded within existing brokerage and retirement account systems, and that convenience attracted new categories of investors who previously remained on the sidelines.

BlackRock’s IBIT emerged as the dominant force within the ETF market, holding hundreds of thousands of Bitcoin and attracting a substantial share of new inflows. Fidelity also became a major beneficiary as institutional investors concentrated capital among the largest providers.

This concentration reinforced a winner-take-most dynamic, in which the largest ETFs benefited from deeper liquidity, tighter bid-ask spreads, stronger analyst coverage, and greater institutional confidence, making them even more attractive to subsequent investors, while smaller funds struggled to compete. Bitcoin increasingly became accessible through the same channels investors already used for stocks, bonds, and commodities, and that changed who could buy Bitcoin and how they approached it.

RELATED: Crypto ETFs May Not Be the Boon for the Ecosystem As Some Believe

Institutional Accumulation Became a Structural Force

The phrase institutional Bitcoin accumulation appeared frequently throughout market discussions for good reason. Institutional participation no longer looked like a temporary experiment, as evidenced by April 2026 alone. Spot Bitcoin ETFs attracted billions of dollars in net inflows (around $1.97 billion), making it one of the strongest months since their launch. Several analysts are describing these flows as evidence that institutional demand was becoming a persistent component of market structure rather than a cyclical event, but the story was not entirely one-directional.

Periods of substantial inflows were occasionally interrupted by meaningful outflows as investors responded to changing macroeconomic conditions and portfolio rebalancing needs. These episodes demonstrated that institutional participation introduces both buying power and selling pressure, a reality that challenged a common assumption.

Many investors once believed institutional involvement would automatically reduce volatility and create permanently rising prices, but the evidence from H1 2026 suggested something more nuanced. Institutions brought scale, liquidity, and legitimacy; they also brought disciplined risk management practices, quarterly reviews, and macroeconomic sensitivities.

Bitcoin was increasingly becoming part of traditional portfolio management processes, and that represented progress, even when it produced uncomfortable short-term market movements.

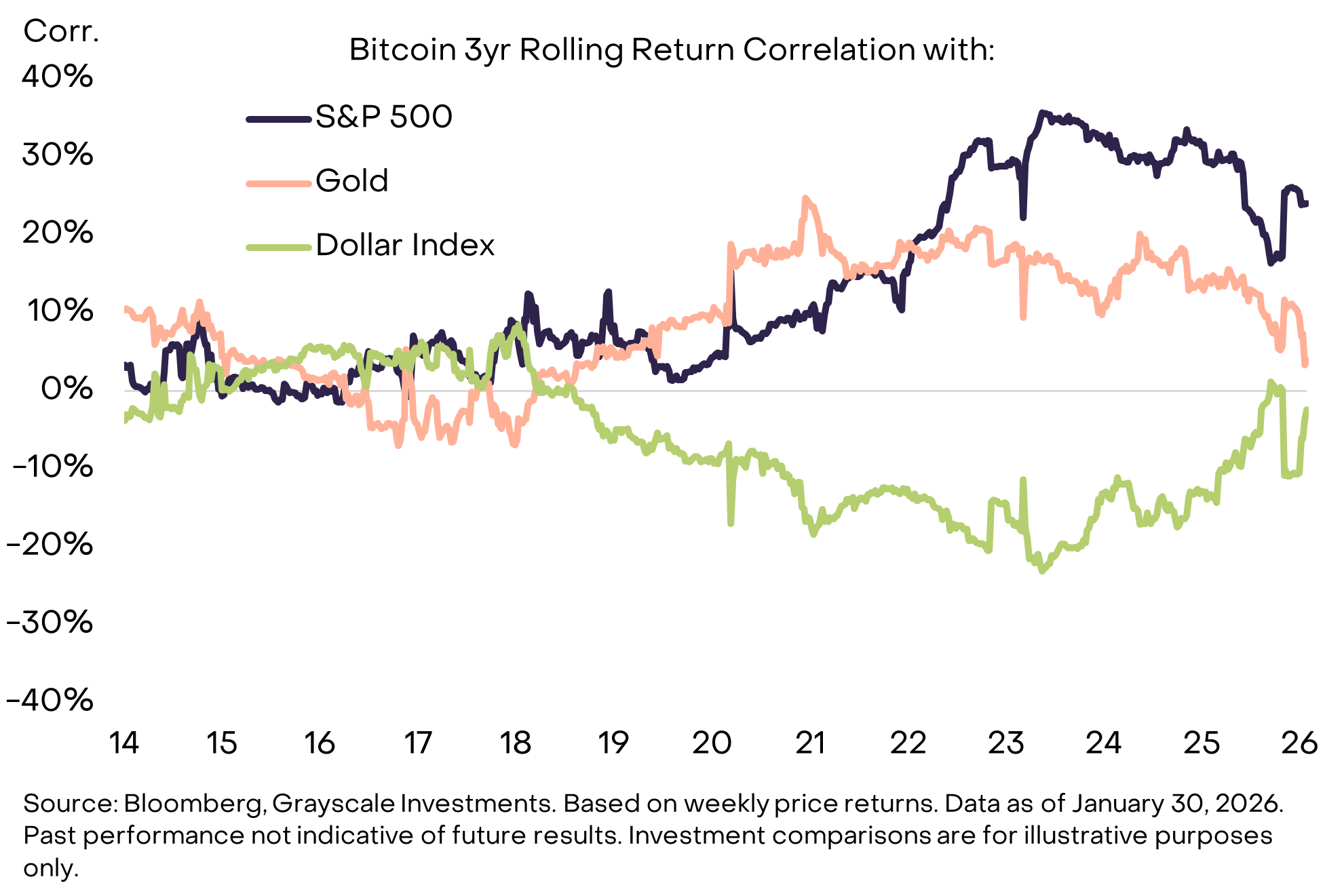

Bitcoin’s Relationship With Stocks Became More Complicated

Bitcoin’s correlation with stocks is one that’s closely watched mainly because, for many years, Bitcoin’s supporters had promoted it as an asset capable of behaving independently of traditional financial markets. Reality has, however, proved more complicated because at various points during its history, Bitcoin displayed strong correlations with technology stocks and broader risk assets.

At other times, those relationships weakened considerably, and by mid-2026, market researchers observed Bitcoin’s correlation with the S&P 500 declining significantly, while its relationships with macroeconomic variables and alternative reserve assets became more prominent. One analysis found Bitcoin’s 90-day correlation with the S&P 500 had fallen near multi-year lows.

This mattered because diversification remains one of the primary reasons investors allocate capital across different asset classes. If Bitcoin moved exactly like stocks, its value as a portfolio diversifier would be limited; the changing correlation patterns suggested Bitcoin remained difficult to classify using traditional categories.

Sometimes it behaved like a risk asset; other times, it behaved more like a macro asset; and in some instances, it followed its own path entirely. That unpredictability has frustrated some analysts while attracting others.

The Safe Haven Debate Refused to Disappear

Although discussions have evolved beyond simple comparisons of digital gold, the Bitcoin safe-haven narrative has remained relevant.

Investors continued asking an important question: what happens when markets become stressed? Gold has historically occupied a special place during periods of uncertainty because central banks hold it and governments accumulate it. Investors often seek it during crises, but Bitcoin’s record remains shorter and more complicated.

Researchers have suggested that Bitcoin and gold increasingly share certain macroeconomic drivers, particularly concerns surrounding currency debasement and fiscal expansion. Some studies found rising correlations between the two assets compared with previous years, while important differences still remained.

In H1 2026, Gold generally experienced smaller drawdowns during periods of market stress, while Bitcoin continued exhibiting higher volatility. Researchers concluded that investors increasingly viewed the assets as complementary rather than interchangeable, a finding that helps explain evolving portfolio strategies.

Many investors stopped asking whether Bitcoin would replace gold and began exploring how both assets could coexist within the same portfolio.

READ ALSO: The Safe-Haven Debate Between Bitcoin and Gold Isn’t Settled Yet

Portfolio Construction Now the Real Conversation

One of the most important developments during H1 2026 concerned Bitcoin portfolio allocation strategies, as financial professionals increasingly approached Bitcoin through the lens of risk-adjusted returns rather than ideological conviction.

Instead of asking whether Bitcoin belongs in a portfolio, investors increasingly asked how much Bitcoin belongs in a portfolio, and this change may seem subtle, yet it reflects a dramatic evolution in market thinking.

Portfolio optimization studies conducted by analysts and institutional researchers continued suggesting that modest Bitcoin allocations could improve diversification characteristics under certain assumptions. Researchers frequently examined allocations ranging from low single digits to more aggressive positions depending on investor objectives and risk tolerance, but not everyone agreed on the appropriate percentage.

Some asset managers remained conservative while others advocated larger allocations due to concerns about inflation, sovereign debt levels, and currency debasement.

Strategists at Berenberg attracted attention after proposing substantial exposure to gold, precious metals, and Bitcoin within certain portfolio frameworks. The recommendation was a 45% allocation to a “gold plus” bucket of gold, silver and Bitcoin, alongside 20% in broad commodities and just 35% in equities, with bonds cut to zero entirely.

What mattered most was the changing mindset as Bitcoin was increasingly being analyzed alongside established asset classes instead of existing outside conventional portfolio discussions.

Sovereign Exposure Still Drawing Attention

Sovereign Bitcoin adoption remained one of the defining storylines of H1 2026, and the numbers tell a more concrete story than the headlines suggest. By the end of 2025, 23 governments held Bitcoin in some capacity, collectively controlling approximately 432,000 BTC, which is roughly 2.1% of the total supply. The United States led with 328,372 BTC, primarily accumulated through criminal asset confiscations, followed by the United Kingdom at 61,245 BTC.

Policy direction has been significant, riding on the buildup from 2025, when Trump signed an executive order establishing a Strategic Bitcoin Reserve as a permanent reserve asset and directing agencies to transfer their holdings rather than sell them, a deliberate break from earlier practice.

The broader significance extends beyond the amount of Bitcoin governments currently hold. Whether or not governments ultimately establish strategic Bitcoin reserves, the fact that policymakers are now debating the asset’s potential role in national financial strategy represents a notable change in Bitcoin’s institutional standing. Unlike previous market cycles, where Bitcoin adoption was driven primarily by retail investors and private companies, we’re seeing sovereign-level discussions become part of the broader conversation around the asset’s future.

A similar trend is also happening in the private sector. ARK Invest CEO Cathie Wood described BlackRock CEO Larry Fink’s evolution from Bitcoin skeptic to advocate as “entry permission” for pension funds, sovereign wealth funds, and other large institutional investors that often wait for established market leaders before allocating capital to a new asset class. Her argument was that BlackRock’s embrace of Bitcoin, particularly through its spot Bitcoin ETF business, reduced the perceived career and reputational risk for institutions that had previously remained on the sidelines.

Sovereign interest represents a separate, but equally meaningful, form of validation. Governments move far more cautiously than private investors, so even preliminary policy discussions tend to carry symbolic weight. While these discussions do not imply imminent government purchases or broad international consensus, they indicate that Bitcoin is increasingly being considered within policy circles rather than dismissed outright as a speculative asset.

It is important, however, to distinguish between governments that intentionally acquire Bitcoin and those whose holdings stem from law enforcement activity. Much of the Bitcoin currently associated with sovereign states (including the United States’ holdings from criminal forfeitures and China’s holdings linked to the PlusToken seizure) was not acquired as part of a deliberate reserve-building strategy. Consequently, existing government holdings should not be interpreted as evidence of an intentional sovereign allocation to Bitcoin.

Likewise, many of the proposals discussed during H1 2026 remained just that—proposals. Legislative or policy discussions in countries such as Brazil, Japan, and Pakistan had not resulted in adopted national Bitcoin reserve policies by the end of the reporting period.

Similarly, in Switzerland, a citizen-led popular initiative has sought to amend the constitution to require the Swiss National Bank to hold Bitcoin alongside gold as part of its monetary reserves. The proposal originated from private advocates rather than the Swiss government and required sufficient public signatures before reaching a national referendum. The Swiss National Bank outrightly rejected the proposal.

Under Switzerland’s system of direct democracy, campaigners were given 18 months to collect the 100,000 signatures required to trigger a national referendum. In May 2026, the organizers announced they were abandoning the initiative after collecting only about half of the required 100,000 signatures, meaning it never reached a referendum.

Even with these important distinctions, the broader trend remains significant. A decade ago, proposals for a US Strategic Bitcoin Reserve, parliamentary discussions about national Bitcoin reserves, or citizen-led constitutional initiatives calling for central bank Bitcoin holdings would have seemed politically improbable. By the end of the H1, such ideas had entered mainstream policy debate across multiple jurisdictions. Whether these initiatives ultimately become law is uncertain, but their emergence reflects Bitcoin’s continued evolution from a niche digital asset into a subject of serious consideration within government and institutional finance.

Investor Behaviour Maturing…

Perhaps the most interesting development involved how investors view Bitcoin in 2026, as investor behaviour has changed noticeably compared with earlier market cycles. Previous cycles were often dominated by retail speculation, social media excitement, and rapid momentum-driven trading, and those elements still exist and always will, but the first half of the year showed increasing evidence of longer-term thinking.

Even during periods when ETF inflows slowed or temporarily reversed, long-term holders continued accumulating Bitcoin, suggesting many investors viewed market weakness as an opportunity rather than a reason to exit entirely.

RELATED: Spot Bitcoin ETFs Bleed $4.4 Billion Over Thirteen Days in Longest Outflow Run on Record

This behaviour resembled patterns commonly associated with mature asset classes, in which investors were becoming more selective and paying closer attention to macroeconomic conditions.

They often monitored interest rate expectations, evaluated portfolio correlations, considered liquidity conditions, and analyzed allocation decisions rather than simply chasing price momentum. That progression reflected a market growing up.

Bitcoin and the Macro Environment

No review of H1 2026 would be complete without examining Bitcoin macroeconomic correlation analysis, as Bitcoin increasingly responded to the same forces influencing broader financial markets. Interest rate expectations mattered as much as inflation expectations, currency strength, and fiscal policy.

Research throughout 2026 repeatedly highlighted the importance of macroeconomic variables in explaining Bitcoin’s performance. Some pointed to factors including Federal Reserve policy expectations, dollar weakness, fiscal concerns, and institutional capital flows as major drivers of market behaviour, representing yet another sign of maturation.

As Bitcoin became integrated into institutional portfolios, it naturally became more sensitive to the forces shaping institutional decision-making. Some critics interpreted this as evidence that Bitcoin had lost its independence, but others disagreed. They argued that Bitcoin’s growing relevance meant it could no longer exist outside the global financial system, but the truth likely sits somewhere between those positions.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.

{kind=link}