Last updated on April 5th, 2026 at 04:45 pm

Quick Breakdown

- The Bank of England wants to introduce stablecoin exemptions that would make regulations less strict. The goal is to support innovation while still keeping the financial system stable and protecting consumers.

- These exemptions could lower compliance costs, boost liquidity, and draw in global investors. This would help the UK become a strong center for digital asset innovation.

- However, exchanges still need to handle important risks like AML/KYC compliance, keeping reserves transparent, and making sure the system stays stable. These steps are needed to operate safely as the rules change

The Bank of England’s proposed stablecoin exemptions represent a major shift in how the UK plans to regulate digital assets used for payments. Instead of applying the same strict rules that govern banks or traditional payment providers, these exemptions would create a lighter, innovation-friendly framework for approved stablecoin issuers and operators.

This move aligns with the UK government’s goal to position the country as a global leader in digital finance. By allowing regulated flexibility, the Bank of England aims to encourage responsible innovation in blockchain-based payments while ensuring financial stability and consumer protection remain intact. These exemptions could reshape how UK crypto exchanges operate and integrate stablecoins into their services.

Current Regulatory Limits for Stablecoins

Right now, both the Financial Conduct Authority (FCA) and the Bank of England (BoE) oversee stablecoin rules in the UK, focusing on consumer protection and financial stability. Most stablecoins are regulated under electronic money and payment system laws, which were not made for crypto assets.

This means issuers have to meet strict rules for capital, safeguarding, and governance, which can be tough for startups or smaller exchanges. The FCA also requires them to register under anti-money laundering (AML) rules, adding more compliance steps.

Restrictions on fiat-backed and algorithmic stablecoins

Fiat-backed stablecoins, such as those pegged to the British pound or U.S. dollar, face strict custody and reserve transparency obligations. Issuers must fully back tokens with high-quality liquid assets and disclose audit details regularly.

Algorithmic stablecoins, on the other hand, face even tougher scrutiny; many are not recognized as legitimate payment instruments under UK law due to their lack of reliable collateral. This makes them effectively unusable for regulated exchanges, limiting trading options and payment use cases.

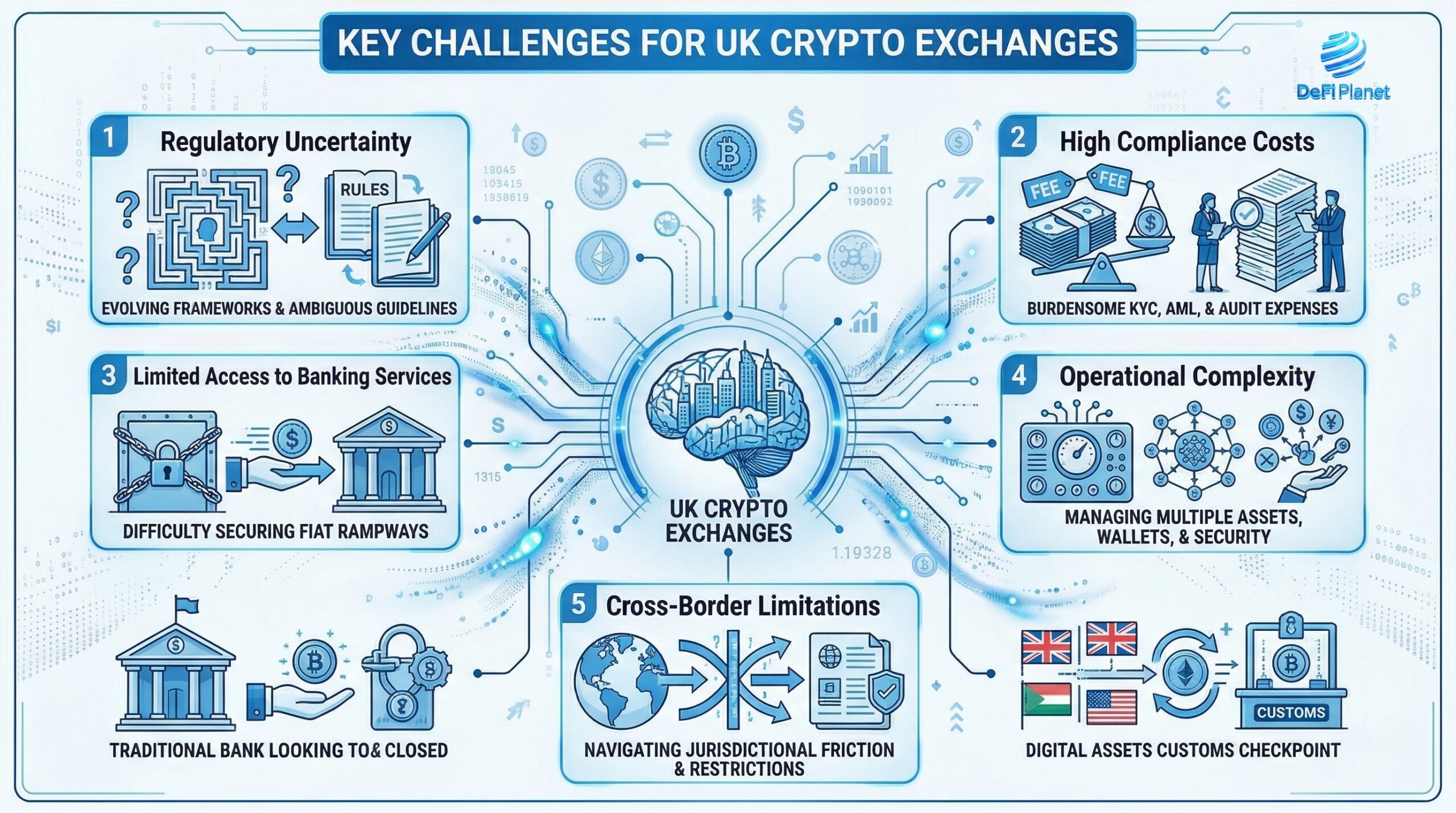

Key challenges for UK crypto exchanges

- Regulatory uncertainty: The absence of a dedicated stablecoin regulation creates confusion over how different types of tokens should be treated. Exchanges must interpret overlapping FCA and BoE rules, increasing legal risks. This uncertainty often leads firms to delay launching new products or seek regulatory approval in other, more predictable jurisdictions.

- High compliance costs: Meeting capital and reporting standards under e-money regulations can be prohibitively expensive, especially for smaller crypto firms. These financial and administrative burdens can limit innovation by forcing startups to divert resources from technology development to legal compliance.

- Limited access to banking services: Many UK banks remain cautious about working with crypto businesses, making it harder for exchanges to manage fiat reserves or facilitate instant stablecoin redemptions. This lack of access to reliable banking partners also affects customer confidence and slows the growth of the broader crypto ecosystem.

- Operational complexity: Without clear guidelines, integrating stablecoins into payment systems or DeFi-like services becomes a legal grey area, slowing innovation. This uncertainty discourages exchanges from experimenting with new financial products that could improve liquidity, settlement speed, and global accessibility.

- Cross-border limitations: Stablecoin projects that operate internationally face conflicting regulatory standards between the UK, EU, and the U.S., complicating compliance strategies. The lack of harmonized rules makes it challenging for UK exchanges to attract international users or offer seamless cross-border transactions.

These limits highlight why many UK crypto exchanges are watching the Bank of England’s exemption plans closely, as they could finally introduce a clearer, more practical pathway for stablecoin adoption and use.

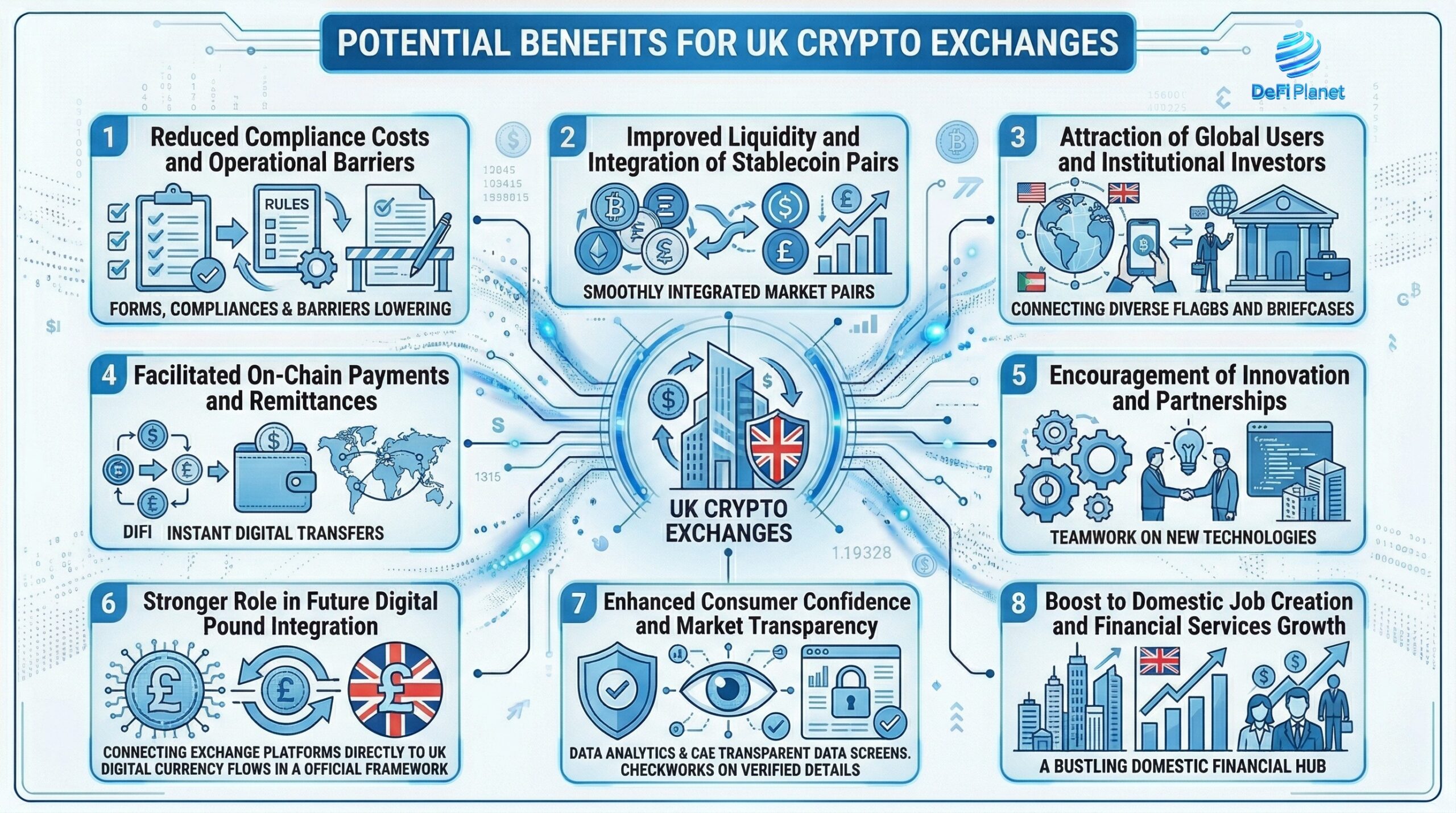

Potential Benefits for UK Crypto Exchanges

If the Bank of England’s proposed stablecoin regulations are implemented, they could reshape how UK crypto exchanges operate, making it easier, cheaper, and more attractive to trade and innovate within a regulated environment.

Reduced compliance costs and operational barriers

By introducing lighter regulatory requirements for approved stablecoins, exchanges could avoid the heavy costs tied to e-money licensing and complex custody rules. This would free up capital for product development, expansion, and improved user experience, helping local exchanges compete more effectively with global platforms like Binance and Coinbase.

Improved liquidity and integration of stablecoin pairs

With a more supportive regulatory structure, UK exchanges could expand their range of stablecoin trading pairs. This would improve liquidity and market depth, making it easier for traders to move between crypto and fiat without price volatility. It could also enhance transaction speed and stability in GBP-based markets.

Attraction of global users and institutional investors

A clearer and more flexible framework would boost international confidence in UK exchanges. Global investors and institutional players prefer regulated markets, so stablecoin exemptions could position the UK as a trusted jurisdiction for digital asset trading and settlement.

Facilitated on-chain payments and remittances

With fewer restrictions, exchanges could enable faster, lower-cost on-chain payments using stablecoins for remittances or retail transactions. This could help the UK strengthen its position as a global fintech hub by merging blockchain efficiency with traditional finance oversight.

Encouragement of innovation and partnerships

Easier rules could lead to new partnerships between banks, payment providers, and crypto firms. Exchanges might collaborate with fintech startups to launch GBP-pegged stablecoins or blockchain-based payment rails, driving ecosystem growth.

Stronger role in future digital pound integration

If the UK eventually launches a central bank digital currency (CBDC), compliant exchanges would already have the infrastructure and experience needed to support it. Stablecoin exemptions could act as a bridge between today’s private tokens and tomorrow’s official digital pound.

Enhanced consumer confidence and market transparency

By allowing regulated stablecoins under Bank of England oversight, exchanges can offer users more transparency and assurance about reserves and risk management, helping rebuild public trust in digital assets.

Boost to domestic job creation and financial services growth

As the UK crypto ecosystem expands under the exemption, exchanges may hire more compliance officers, developers, and analysts, creating new jobs and strengthening London’s status as a global fintech hub.

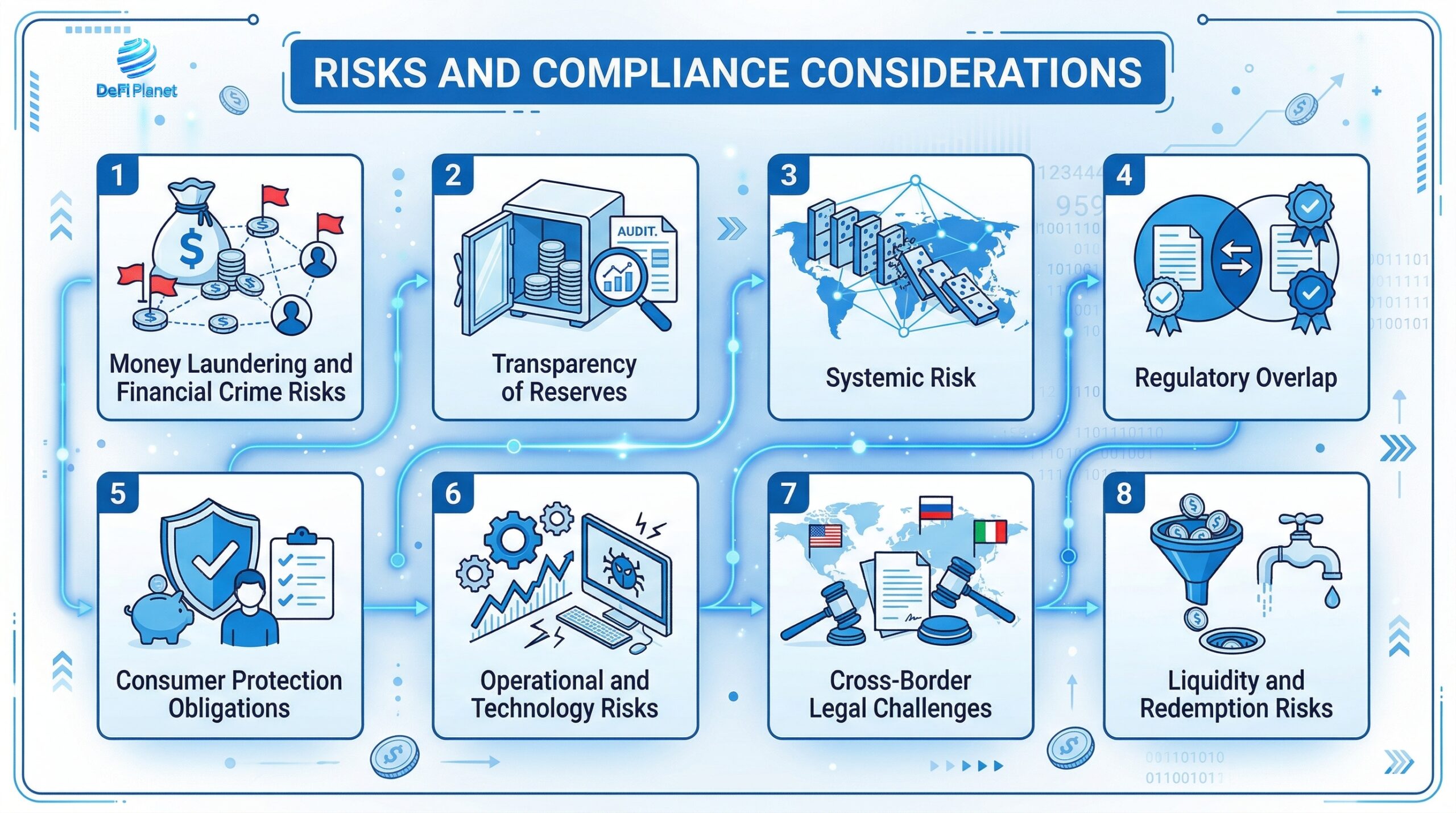

Risks and Compliance Considerations

Even with stablecoin exemptions, UK crypto exchanges face multiple risks and compliance challenges that must be carefully managed to operate safely and legally.

Money laundering and financial crime risks

Exchanges must implement robust AML and KYC procedures to stop stablecoins from being exploited for money laundering, terrorist financing, or fraudulent schemes. This includes identity verification, transaction monitoring, and suspicious activity reporting. Regulators increasingly expect ongoing audits and real-time risk detection systems, meaning crypto firms need dedicated compliance teams to stay ahead of evolving threats.

Transparency of reserves

Stablecoins should be fully backed by fiat, liquid assets, or equivalent guarantees. Exchanges must provide regular independent audits and publish detailed reserve reports to reassure both regulators and investors. Lack of transparency can erode trust and may trigger regulatory scrutiny, making consistent reporting and reserve management crucial for sustainable operations.

Systemic risk

A collapse or sudden de-peg of a widely used stablecoin can ripple through financial markets, affecting payment systems, trading platforms, and institutional users. Exchanges should maintain liquidity buffers, clear risk mitigation frameworks, and emergency protocols to minimise the impact of sudden market shocks, including communication strategies for users during crises.

Regulatory overlap

With guidance coming from both the FCA and Bank of England, exchanges face potential contradictions in capital, reporting, and operational rules. Legal ambiguity can increase compliance costs and operational delays. Firms need legal and compliance teams to interpret overlapping rules carefully and maintain flexibility without breaching regulatory expectations.

Consumer protection obligations

Even under exemptions, exchanges are expected to educate users about stablecoin risks, such as de-pegging, network failures, or counterparty issues. Clear disclosures, limits on product offerings, and safeguards like redemption guarantees can protect retail investors and build long-term trust. Failing to meet these obligations can lead to reputational damage and enforcement action.

Operational and technology risks

Integrating stablecoins into platforms, wallets, and payment rails introduces risks, including cyberattacks, software bugs, and system downtime. Exchanges must invest in secure infrastructure, regular penetration testing, redundancy measures, and incident response plans. Operational resilience is essential to maintain investor confidence and avoid costly disruptions.

Cross-border legal challenges

UK exchanges that service international users must navigate conflicting regulatory frameworks across the EU, the US, and other regions. Misalignment in rules can lead to fines, trading restrictions, or legal disputes. Proactive strategies include implementing geofencing, tailored compliance protocols for each jurisdiction, and ongoing regulatory monitoring.

Liquidity and redemption risks

Stablecoin holders expect to convert tokens into fiat or other assets quickly. Exchanges must maintain sufficient reserves, robust redemption processes, and contingency plans to prevent liquidity shortages. Poor liquidity management can erode trust, trigger withdrawal panics, and harm market credibility.

Implications for Market Growth and Innovation

The Bank of England’s stablecoin regulation could position the UK as a leading hub for crypto innovation, attracting both retail and institutional players. By reducing regulatory barriers while maintaining oversight, these measures may encourage exchanges to expand offerings, improve liquidity, and foster new financial products. Exchanges that prepare early for compliance and robust risk management are likely to benefit most from these changes.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this piece? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”