Last updated on April 8th, 2026 at 11:25 am

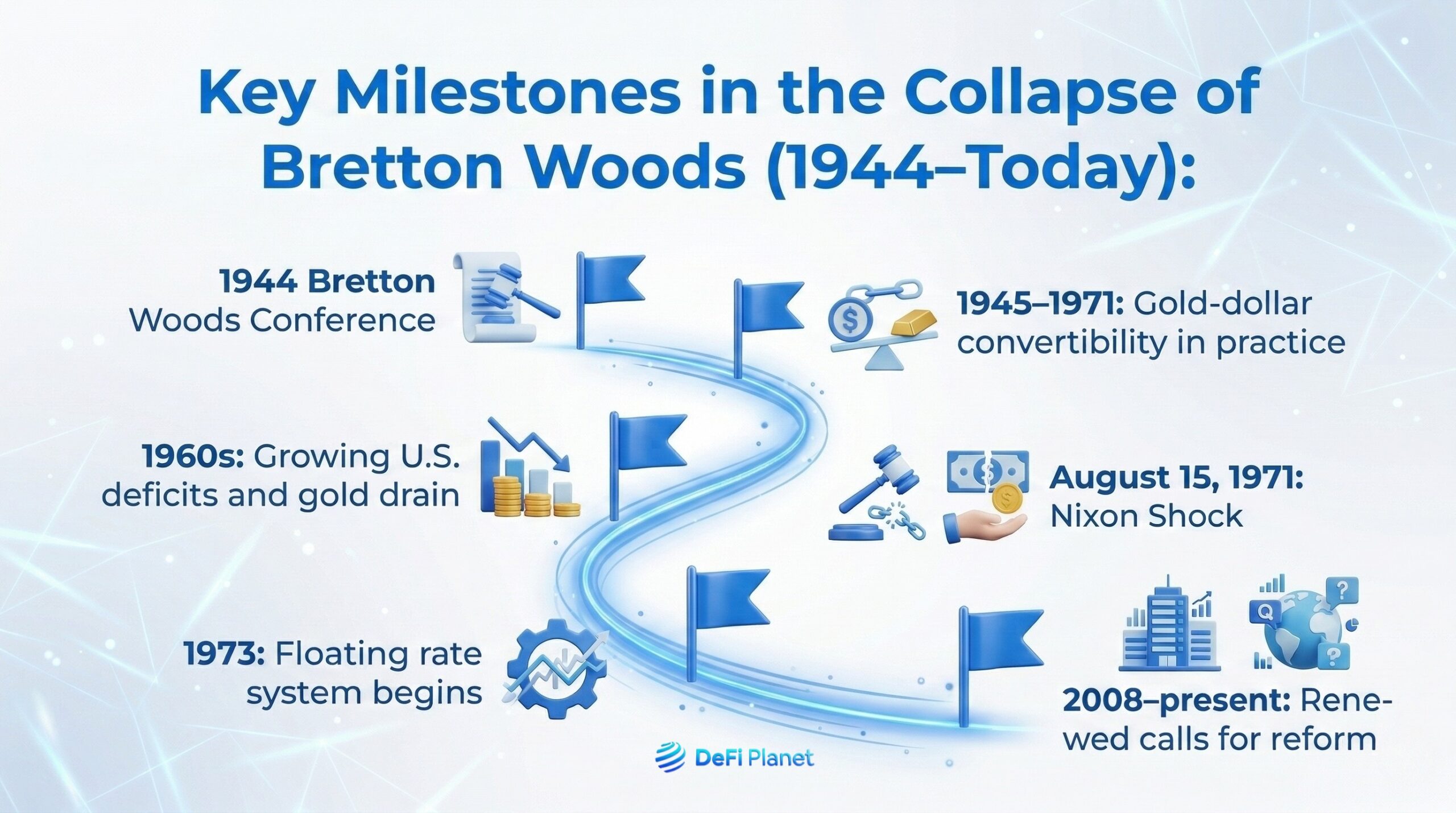

In July 1944, while World War II was still raging, delegates from 44 nations gathered in New Hampshire, United States, to design a new international monetary system. The world was broken, and Europe was physically destroyed. Trade had collapsed, trust between nations was fragile, and leaders knew that if they did not build a stable financial order, the chaos of the 1930s could repeat itself.

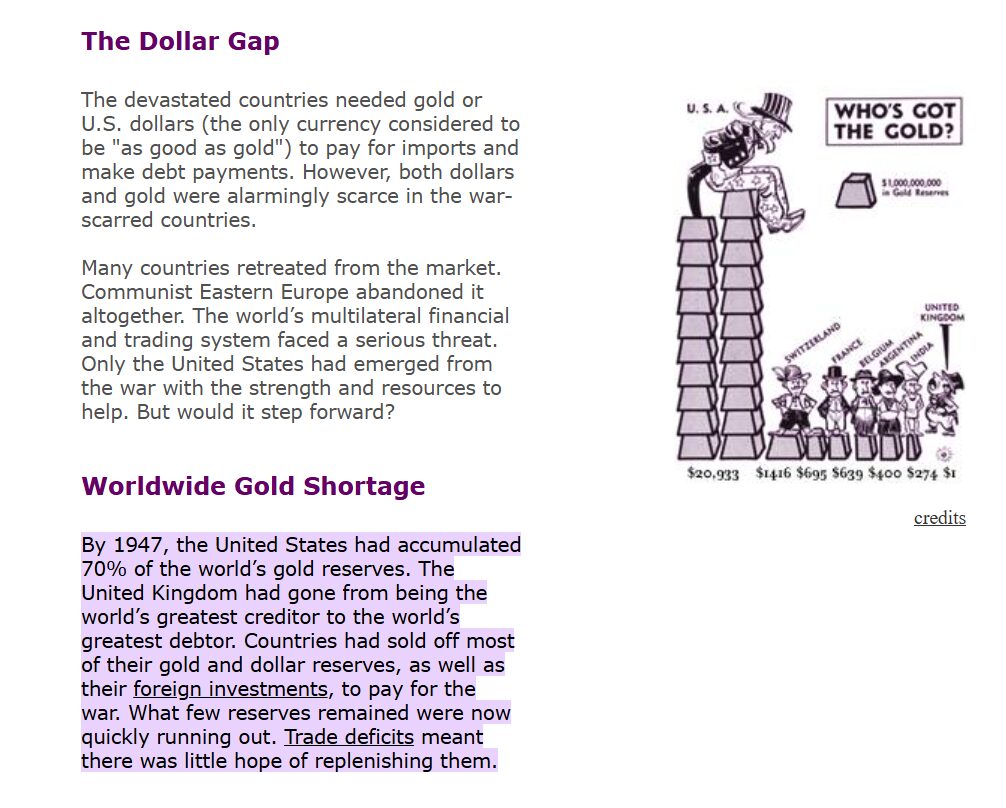

The result was the Bretton Woods agreement; it created a dollar-based system where currencies were pegged to the US dollar and the dollar was convertible into gold. It also led to the creation of the International Monetary Fund and the World Bank to support post-war reconstruction and stabilize global finance. According to historical data from the Federal Reserve and IMF archives, the United States controlled roughly two-thirds of official global gold reserves by the end of the war, which gave it enormous leverage in negotiations. That concentration of reserves shaped the currency hierarchy that has followed ever since.

In this case study, we envision a scenario where blockchain technology had existed during World War II. What if governments could instantly verify reserves using cryptographic proof? What if settlements between countries were transparent and programmable, instead of relying on paper records and trust in central banks? Would Bretton Woods have turned out the same way? Would the dollar still have dominated, or would the international monetary system look different?

To answer that, we need to understand what Bretton Woods actually solved.

The Problems Bretton Woods Was Trying to Fix

The interwar years were marked by competitive devaluations and protectionist policies, with countries trying to weaken their currencies to boost exports and revive what was falling apart of their wartime economy. The Smoot-Hawley Tariff Act in the United States worsened global trade tensions, and the gold standard collapsed in the early 1930s, with economists widely agreeing that currency instability deepened the Great Depression. Research from the National Bureau of Economic Research shows that countries leaving the gold standard earlier recovered faster, highlighting how rigid monetary structures limited policy flexibility.

By 1944, policymakers wanted stability without repeating the mistakes of the old gold standard, which is why at Bretton Woods, they designed a hybrid system where the dollar was tied to gold at $35 per ounce. Other currencies were pegged to the dollar but could adjust within limits, and thus, the IMF was created to manage short-term balance-of-payments issues. The World Bank was designed to fund post-war reconstruction in Europe and Japan, where these institutions shaped global finance for decades.

However, this system relied heavily on trust and opaque accounting because gold reserves were reported by governments, and currency pegs depended on central bank credibility. Cross-border settlements moved slowly and lacked real-time verifications, and smaller nations had limited insight into the true financial position of dominant powers.

Imagining Blockchain Counterfactuals

In this alternate timeline, governments record their gold reserves and foreign currency balances on a shared ledger. Every participating country can verify balances in real time, and instead of trusting paper audits, delegates at Bretton Woods view cryptographic proofs of reserves, changing negotiation dynamics immediately.

One of the most important facts about Bretton Woods was the imbalance of gold holdings. The United States entered negotiations with massive reserves, giving it bargaining strength. Economic historian Barry Eichengreen, in his book Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System, has written about how this imbalance shaped the final agreement and cemented dollar dominance in the post war order. If gold reserves were transparently verified on-chain, the imbalance would still exist, as blockchain would not magically redistribute gold; however, transparency could have reduced suspicion among smaller nations.

It could also have influenced negotiation dynamics at Bretton Woods itself, with blockchain transparency, smaller nations could have independently verified the dollar’s backing, which might have strengthened trust and allowed for more confident negotiations around exchange rate adjustments and stabilization support. This verification might have allowed them to negotiate better terms on exchange rate adjustments or stabilization support, knowing that the numbers were publicly auditable. In turn, this could have fostered a greater sense of fairness and trust, potentially reducing political friction between dominant and smaller economies and creating a stronger, more cooperative foundation for the international monetary system from the very start.

Transparent Reserves and Power Dynamics

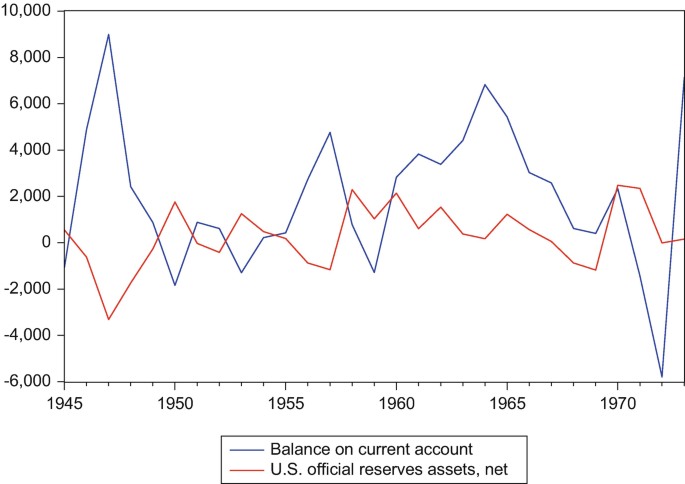

At the same time, blockchain transparency could have exposed structural weaknesses earlier. By the late 1960s, the United States was running persistent balance-of-payments deficits, and foreign governments began converting dollars into gold, draining US reserves. President Richard Nixon ended gold convertibility in 1971, effectively ending the Bretton Woods system.

If gold backing had been publicly verifiable through cryptographic audits, pressure on the system may have emerged sooner, and markets could have tracked reserve depletion in real time. Also, speculative attacks might have accelerated, and the collapse of dollar convertibility might have happened earlier than 1971.

In a blockchain-enabled international monetary system, informational advantage would have become smaller, and negotiation power would have been more closely tied to measurable reserves rather than political influence alone.

Blockchain and Settlement Efficiency in Global Finance

During the mid-twentieth century, international settlements were slow because they had to go through multiple intermediate correspondent banking networks. Blockchain-based settlement would have allowed near instant transfers between central banks, and this would have reduced counterparty risk and increased confidence in cross-border trade.

Researchers at the Bank for International Settlements have published studies on how distributed ledger technology could modernize cross border payments, with their findings suggesting that real-time settlement would reduce liquidity risk and improve transparency. If such infrastructure had existed in 1944, policymakers might have designed a less rigid peg system because settlement frictions would be lower.

In today’s world, central banks are actively exploring digital currencies; the BIS and IMF both publish research on central bank digital currencies and cross-border interoperability. These modern discussions mirror questions that Bretton Woods delegates faced, but with digital tools instead of paper ledgers. Programmable money adds another layer to these blockchain counterfactuals, and with smart contracts, balance of payments adjustments could be automated. Instead of political negotiation every time a country faced a deficit, programmable rules could trigger stabilization loans or currency adjustments automatically.

On the other hand, automation reduces discretion, and governments typically need flexibility to be effective. The ability to suspend rules was one reason Bretton Woods functioned for decades despite pressures with a system that allowed adjustable pegs, meaning countries could change exchange rates under certain conditions. That political breathing room helped maintain cooperation inside the broader international monetary system.

Rigid smart contracts might have limited that flexibility. For example, during severe recessions, countries sometimes imposed capital controls or adjusted exchange rates outside agreed bands. A fully automated blockchain system might have made such moves harder.

There is also going to be the question of data quality, where smart contracts depend on accurate inputs. In the 1940s and 1950s, economic statistics were slower and less standardized than they are today. If programmable rules relied on delayed or inaccurate data, automatic responses could worsen instability rather than solve it. A stabilization loan triggered on the basis of outdated trade figures will signal deeper weakness instead of calming markets.

Another challenge is political accountability in that, if economic outcomes are determined partly by code, who takes responsibility when things go wrong? Governments could blame the protocol, which in turn could be blamed on its designers. Public trust was essential in those fragile periods of post-war construction where leaders needed to explain policy choices to their citizens. Handing too much control to automated systems might have created democratic tension, yet the benefits are powerful.

A programmable framework could have reduced moral hazard, and countries would know the exact terms under which support would arrive and the conditions attached to it. Instead of opaque negotiations behind closed doors, adjustments would follow visible rules, and that level of transparency might have strengthened confidence in global finance, especially among nations worried about unequal treatment.

In the end, programmable money would have shifted the balance between rules and politics. Bretton Woods succeeded partly because it blended both; it had formal structures like the IMF, but it also relied heavily on diplomacy and compromise. A blockchain-based version of the international monetary system might have been more rule-driven and less politically flexible, but whether that would make it stronger or more brittle remains an open question.

Post-War Reconstruction on Chain

Consider the Marshall Plan, which provided over thirteen billion dollars in US aid to Europe between 1948 and 1952. According to the US State Department historical office, this aid was crucial for rebuilding infrastructure, stabilizing economies, and restoring confidence in global finance, with much of the funding being administered through government agencies and coordinated with local European authorities, allowing for both oversight and flexibility in how the money was spent.

In a blockchain‑enabled scenario, these aid flows could have been recorded transparently, making it easier to verify that funds reached their intended projects. Smart contracts could, in theory, automate disbursements based on predefined economic milestones or reconstruction targets, potentially reducing errors or misuse, and transparency might have increased accountability by allowing donors and recipients to see where resources were going.

At the same time, full public visibility could have complicated diplomacy and strategic decision-making, with some allocations requiring discretion to address sensitive political situations or to negotiate with multiple governments. Too much transparency could have exposed negotiations or political priorities in ways that might have made coordination more difficult.

Would Bretton Woods Still Exist

So would Bretton Woods still exist in a world shaped by blockchain technology? The answer is complex, with the core goals of stability, reconstruction, and cooperation likely to remain. The trauma of war would still push nations toward coordination, and after two global conflicts in one generation, leaders were desperate to avoid another collapse of the international monetary system like the one that deepened the Great Depression. That political motivation would not disappear simply because better technology existed.

However, the structure of the international monetary system might look different; greater transparency could reduce reliance on a single dominant reserve currency, and if trust were embedded in code rather than concentrated in one nation’s balance sheet, smaller countries might demand a more distributed reserve structure. In 1944, the United States had enormous leverage because it held the majority of global gold reserves. We have seen from historical IMF data and US Treasury records that America’s gold position gave it unmatched negotiating power, and in a blockchain-based environment where reserves were cryptographically verified and visible to all, that leverage would still matter, but it would be quantified and continuously monitored rather than politically interpreted.

We might have seen a multi-currency reserve basket from the start rather than a dollar-centred hierarchy, and we might even have seen earlier experimentation with synthetic units of account similar to the IMF’s Special Drawing Rights, but implemented as programmable tokens. The IMF introduced Special Drawing Rights in 1969 to supplement existing reserves, as confirmed in the IMF archives. In a blockchain-enabled 1940s, such a basket unit could have been launched decades earlier and issued directly on a shared ledger, with transparent backing and automated rebalancing rules.

That possibility becomes even more realistic when you consider how modern central banks think about digital infrastructure today. The Bank for International Settlements has argued in multiple research papers that distributed ledger technology can support multi-currency platforms where settlement risk is reduced through shared ledgers, but if that kind of architecture had existed during post-war reconstruction, delegates might have chosen a cooperative ledger for reserve management instead of a dollar gold peg.

A blockchain-based Bretton Woods might also have limited what economists later called the Triffin dilemma. The Triffin dilemma describes the tension that arises when a national currency also serves as the world’s reserve currency. To supply global liquidity, the issuing country must run deficits, but persistent deficits eventually undermine confidence in that currency; this dynamic contributed to the collapse of the original Bretton Woods arrangement in 1971 when President Nixon suspended gold convertibility. If reserve supply had been distributed across a programmable basket rather than dependent on US deficits, that tension might have been softened.

If every country could see another nation’s declining reserves in real time, markets might react faster and more aggressively, and this could have increased speculative pressure. In that sense, blockchain might have made the system both more honest and more fragile. Stability in global finance sometimes depends on delayed information and controlled disclosure, and radical transparency would have changed that balance.

Another change could have involved capital flows. Under the original Bretton Woods framework, countries were allowed to use capital controls to manage volatility. Economists such as John Maynard Keynes supported maintaining some control over cross-border capital movements to preserve domestic policy space. In a blockchain-integrated system where transfers settle instantly and globally, enforcing capital controls becomes more technically challenging, and governments would need programmable compliance layers built into the protocol itself, which means sovereignty would be partially encoded in software.

During post-war reconstruction, Europe depended heavily on coordinated funding and staged payments. In a programmable system, recovery funds might have been released automatically based on measurable economic indicators such as industrial output or trade balances. This could have strengthened accountability and efficiency, but at the same time, it could have limited political discretion, which was often crucial in rebuilding trust between former enemies.

Ultimately, Bretton Woods was a political compromise shaped by power, fear, and hope, with blockchain technology changing how information moves and how settlements occur, but it does not erase geopolitical realities. The United States would still have emerged from World War II as the strongest industrial and military power. Britain would still have faced exhaustion, and Europe would still have needed rebuilding.

What might have changed is the hierarchy of trust; instead of trusting primarily in the balance sheet of one country, nations could have trusted in a shared protocol. Rather than have gold sitting in vaults as the ultimate anchor, digitally verified reserves could have acted as the foundation of credibility; the psychological shift from trusting a nation to trusting a network would be profound.

So yes, some version of Bretton Woods would likely still have emerged, and the world would still have needed coordination, with its design being less centralized, more transparent, and more programmable. The reserve system might have been diversified earlier, and the tensions that eventually broke the dollar gold link might have surfaced sooner, forcing reforms decades earlier.

In that alternate timeline, the story of the international monetary system might not be one of a single currency rising to dominance and then struggling under its own weight; it might have been the story of a distributed architecture built at the very moment the modern era of global finance began.

Lessons for Today’s Global Finance

This thought experiment is not just about history, as it helps us understand current debates in global finance. Today, central banks are studying digital currencies, stablecoins operate across borders, and DeFi protocols settle transactions in minutes rather than days.

The Bretton Woods system eventually collapsed because of an imbalance between domestic policy goals and international commitments. Blockchain does not eliminate that tension, but it changes information flows and settlement speed.

By studying these blockchain counterfactuals, we see that technology can shift power dynamics but cannot erase economic fundamentals. Gold reserves, trade balances, and political strength would still matter, and what would have changed is the transparency of those factors.

If blockchain had existed during World War II, Bretton Woods may still have been created, but it likely would have been more transparent, more automated, and possibly less centered on a single currency. The global hierarchy that shaped the second half of the twentieth century might have been flatter.

History teaches us that financial systems are built in moments of crisis, technology shapes how those systems function, but politics shapes who benefits. As we design the next version of the international monetary system, we should remember Bretton Woods and ask whether transparency and programmability can create a more balanced form of global finance.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this piece? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

“Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}