Despite offering radical innovations in finance, ownership, and digital sovereignty, the cryptocurrency industry still grapples with a foundational issue: trust. While sensational scams often dominate headlines, the crypto trust issues go far beyond bad actors.

Regulatory uncertainty, technological opacity, and community governance failures have all played a role in undermining public confidence. Let’s explore how these challenges unfold and what’s being done to rebuild trust from the blockchain up.

High-Profile Crypto Scams and Their Impact on Public Perception

The trust deficit in the cryptocurrency world didn’t emerge overnight, it was carved out by a history of devastating scams, fraud, and high-profile collapses that have shaken public confidence to its core. These incidents have not only resulted in staggering financial losses but have also left a lasting stain on the industry’s reputation.

From the beginning of 2021 through June 2022 alone, the U.S. Federal Trade Commission reported that more than 46,000 individuals fell victim to crypto-related scams, collectively losing over $1 billion. The average loss per person? A painful $2,600.

One of the most infamous events in crypto history is the collapse of FTX. Once hailed as the world’s second-largest cryptocurrency exchange, FTX imploded in November 2022 after shocking revelations emerged: founder Sam Bankman-Fried aided by some company executives had allegedly misappropriated customer funds through his trading firm, Alameda Research. The aftermath was catastrophic—over $8 billion in customer funds disappeared.

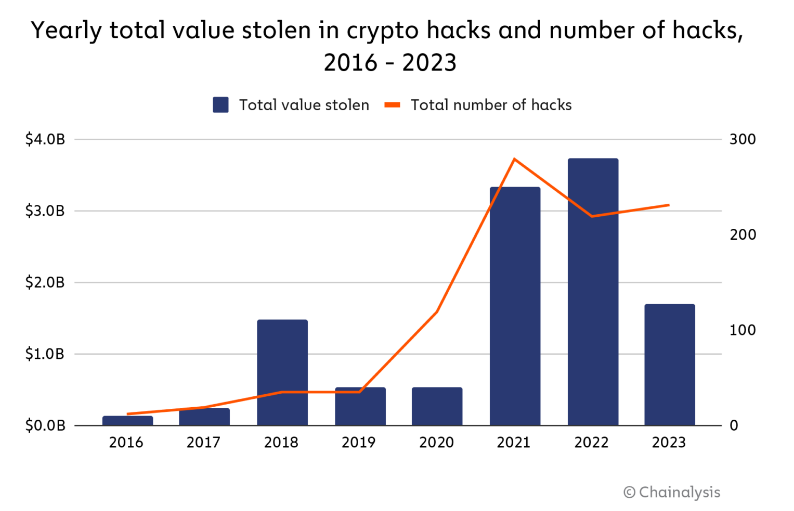

Adding to the woes, 2022 was marked as the worst year for crypto hacks in history. According to Chainalysis, a staggering $3.7 billion was stolen that year, primarily from decentralized finance (DeFi) protocols.

These breaches amplify the question on many minds: Why is crypto not trustworthy? The answer is rarely simple, but undeniably, these scandals worsen crypto trust issues, dragging down both perception and adoption. A survey by the Pew Research Center revealed that 75% of Americans familiar with cryptocurrency express little to no confidence in its safety or reliability. In a world where credibility is currency, these scandals continue to devalue crypto’s standing in the public eye.

RELATED: Are Scams Damaging Crypto’s Reputation?

The Role of Regulatory Uncertainty in Eroding Trust

When it comes to building trust in the crypto industry, few issues are as significant—or as persistent—as crypto regulation uncertainty. While the crypto ecosystem has evolved at an astonishing pace, regulation has struggled to keep up. This disparity has created a patchwork of rules and interpretations across the globe, where what is legal and encouraged in one country might be penalized or banned in another. The inconsistency doesn’t just confuse, it fundamentally undermines trust, especially among those considering long-term participation in the space.

In the United States, how regulatory uncertainty affects crypto trust is particularly clear. Authorities like the Securities and Exchange Commission (SEC) have often relied on a reactive approach, enforcing rules through litigation. This method—often described as “regulation by enforcement”—has created a climate of uncertainty for businesses, investors, and consumers alike. Companies find themselves operating in a gray zone, unsure whether their actions today might provoke legal action tomorrow. However, recent developments hint at a possible shift in strategy.

RELATED: Cryptocurrency Crackdown: A Timeline of the US SEC’s Enforcement Actions

On January 23, 2025, President Trump signed an executive order titled “Strengthening American Leadership in Digital Financial Technology,” which not only revoked Executive Order 14067 but also dismantled the Treasury Department’s earlier framework for international engagement on digital assets. This move appears to mark a departure from the previous administration’s stance and suggests a potential pivot toward clearer, innovation-supportive regulation.

Yet the impact of this uncertainty goes far beyond legal confusion. It directly stifles innovation. Startups, often the lifeblood of technological advancement, face significant hurdles in attracting investment or scaling operations when the regulatory playing field remains undefined.

Even well-established firms are reluctant to dive deeper into crypto, wary of becoming the next target of enforcement. This hesitation extends to institutional investors whose involvement is crucial to the industry’s maturation, many of whom stay on the sidelines due to the lack of predictable regulatory oversight.

The dangers of this regulatory limbo aren’t merely hypothetical. Rostin Behnam, Chair of the Commodity Futures Trading Commission (CFTC), has warned that unclear regulation not only suppresses growth but also increases the risk of financial fraud and systemic instability. In an environment without strong and consistent oversight, bad actors can more easily exploit loopholes, undermining whatever fragile trust the public may have in digital assets.

This fragmented regulatory landscape isn’t limited to the United States. Across the world, responses to crypto vary drastically. El Salvador made headlines by adopting Bitcoin as legal tender, a bold and controversial move that attracted global attention. In stark contrast, China has implemented sweeping bans on crypto-related activities, effectively driving the industry underground within its borders.

Meanwhile, the European Union is attempting to strike a middle ground. With the introduction of the Markets in Crypto-Assets (MiCA) framework in 2024, the EU has taken significant steps toward providing a unified, transparent set of rules designed to offer both investor protection and room for innovation.

Until there is a more globally coordinated, forward-looking approach to crypto regulation, trust will continue to be an elusive commodity. The current state of legal unpredictability does more than just slow progress, it endangers the foundational promise of crypto itself: to create a fair, inclusive, and transparent financial system. Without regulatory clarity, that vision risks being lost in the fog of uncertainty.

RELATED: MiCA Regulation Marks One Year—Successes and Challenges in the EU’s Stablecoin Space

Transparency Challenges in Decentralized Platforms

Transparency is one of crypto’s proudest promises. In theory, blockchain technology offers a radically open financial system—one where every transaction is traceable and every rule is embedded in code. But when we dig beneath the surface, a different story begins to unfold. Despite its transparent foundation, the decentralized world often operates in ways that are anything but clear.

Let’s start with Decentralized Autonomous Organizations, or DAOs. These entities were supposed to revolutionize governance by giving the power back to the people. But in practice? It’s often the whales and venture capital firms who pull the strings. While votes may happen on-chain, the true concentration of power lies in who holds the most governance tokens, and that’s rarely the everyday user. A striking example came in 2022, when Solend DAO, a lending protocol on Solana, controversially proposed taking over a user’s wallet to avoid a major liquidation crisis. The move sparked backlash, with many accusing the DAO of betraying its very ethos of decentralization.

RELATED: Most DAOs Are Doomed to Fail—Here’s Why

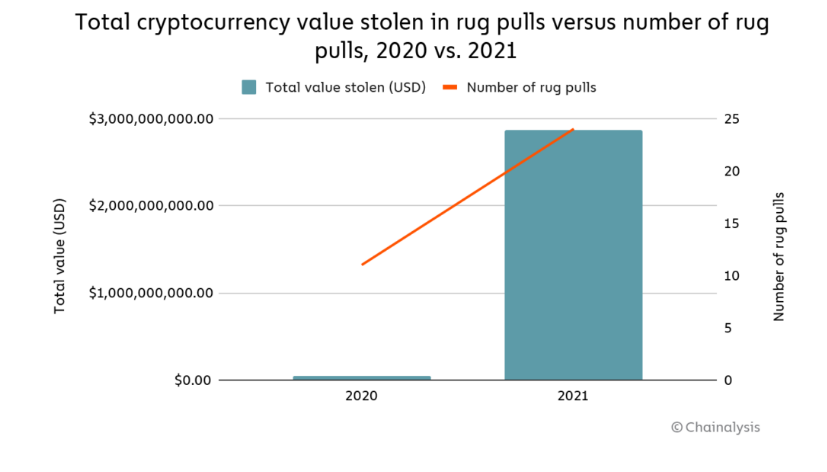

Similarly, smart contracts—the building blocks of DeFi—are visible but not easily understandable. Most users can’t read code, leaving them vulnerable to manipulation or coding errors. Exploits stemming from smart contract vulnerabilities are widespread. Rug pulls accounted for 37% of all scam revenue in 2021, often the result of deliberate backdoors in contracts. It’s a troubling statistic for an industry founded on the promise of trustless systems and decentralization.

READ ALSO: Can DeFi Insurance Products Solve the Problem of Rug Pulls?

Transparency also breaks down when it comes to data collection and analysis. Smart contracts rely on oracles to pull real-world information—like asset prices—into the blockchain. But when the data fed into these contracts doesn’t match the actual market, things can go sideways fast. This happened with the bZx protocol in 2020, when mismatched price data was exploited, resulting in over $8 million in losses. It’s a stark reminder that when off-chain and on-chain data don’t align, transparency and security suffer.

So yes, the blockchain is public. Yes, the data is technically there. But when governance is concentrated, code is inaccessible, data is fragmented, and scaling adds complexity, transparency becomes more of a tagline than a reality. If the decentralized future is going to earn the world’s trust, it has to do more than just promise transparency—it has to live it in practice.

Community-Driven Initiatives to Enhance Accountability

For an industry born from the desire to upend traditional systems, crypto has faced its share of backlash. Yet the response hasn’t been solely defensive. Communities are actively creating mechanisms to build a more trustworthy crypto landscape.

The post-FTX push for Proof of Reserves (PoR) is one such move. Platforms like Binance, BitMex, OKX and Kraken now offer independently audited statements to assure users that their assets exist and are accounted for. This initiative, although still maturing, directly addresses crypto trust issues and signals an industry moving toward greater accountability.

Security is another battleground. Projects now routinely conduct audits and fund bug bounty programs. These not only identify smart contract vulnerabilities before hackers do but also help instil user confidence. Platforms like Immunefi offer hefty bug bounty rewards for developers who catch vulnerabilities before malicious actors do.

Identity tools are also gaining traction. Blockchain-native platforms like BrightID and Gitcoin Passport aim to answer the question: Can we trust crypto users? These tools verify identity in decentralized systems without compromising privacy, creating a more credible Web3 experience.

Lastly, Regenerative Finance (ReFi) projects demonstrate that crypto can be a force for good. . As of 2024, projects like Toucan Protocol and KlimaDAO are using blockchain to address environmental and social challenges. Instead of just creating wealth, they’re channeling crypto toward sustainability and climate action. It’s an encouraging counter-narrative—one that suggests this technology isn’t just for profit, but for progress.

Conclusion: Trust as Crypto’s Next Frontier

The crypto industry is no longer in its Wild West infancy — but its trust issues remain a core barrier to mass adoption. While scams and hacks have played a significant role, the deeper, structural problems of regulatory uncertainty, technical opacity, and governance gaps have arguably done more to undermine confidence.

Still, progress is being made. From proof-of-reserve systems and decentralized identity solutions to more responsive regulatory frameworks in places like the EU and Singapore, the ecosystem is evolving. For crypto to truly fulfill its promise — as a tool for financial inclusion, autonomy, and innovation — rebuilding trust must become a central priority, not an afterthought.

Until then, the mantra remains: “Don’t trust. Verify.” But it’s time we made verifying a whole lot easier.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you want to read more market analyses like this one, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}