In the world of crypto, numbers can be deceiving, especially when it comes to how returns are advertised. Two of the most commonly used terms in decentralized finance and crypto lending are APR (Annual Percentage Rate) and APY (Annual Percentage Yield). While they may sound similar, they tell very different stories about how your money grows or what it costs you to borrow.

Whether you’re staking tokens, providing liquidity, or borrowing crypto assets, understanding the difference between APR and APY in crypto is key to making more informed financial decisions. In this article, we’ll break down the differences, how they’re calculated, and when one might be better than the other.

What is APR in Crypto?

APR, or Annual Percentage Rate, represents the simple interest you earn on a crypto investment or owe on a loan over the course of one year, excluding any gains from reinvesting the interest. In essence, it reflects the base percentage rate applied to your initial amount, giving you a straightforward yet limited view of your potential earnings or costs.

You can think of APR as the equivalent of the sticker price for borrowing or investing in the crypto space. It shows you the upfront interest rate, but it doesn’t consider how often the interest is paid out or reinvested. This makes it a straightforward metric, but not always a complete one, especially in DeFi, where compounding can significantly impact actual returns.

What is 10% APY in crypto? For example, if you lend $1,000 worth of stablecoins on a DeFi platform that offers a 10% APR, you would earn exactly $100 after one year, assuming there is no compounding involved during that period. The calculation is simple: $1,000 x 10% = $100.

While APR provides a precise and easy-to-understand estimate of your expected return or cost, it’s essential to note that it doesn’t reflect the actual growth potential of your funds if the interest is reinvested or compounded throughout the year. For that, you’d need to look at APY, which captures the impact of compounding over time.

And here’s another common concern: Does APR mean you pay more? The answer depends on the scenario. If you’re borrowing, APR is typically less costly than APY because it excludes compounding. But in investment contexts, APR might underrepresent potential earnings when compounding is present.

Understanding APR is useful for comparing offers and making short-term decisions. Still, if you’re aiming for long-term yield or managing risk across various DeFi products, it’s essential also to consider how and when returns are compounded.

What is APY in Crypto?

APY, or Annual Percentage Yield, takes interest to the next level by factoring in compound interest, meaning you earn returns not just on your initial principal, but also on accumulated interest. This is why, when comparing APR vs APY in crypto, APY often provides a more realistic picture of what your earnings will look like over time.

To put it simply, APY captures the true earning potential of your investment by taking into account how frequently your returns are reinvested and allowed to grow.

So, what is 10% APY in crypto? If you invest $1,000 at 10% APY with monthly compounding, your returns will exceed $100 by year’s end, amounting to approximately $104.71. That extra $4.71 is due to the effect of compounding. This makes APY more insightful for long-term investments.

To determine your yield, you’ll need to know how to calculate APY. The formula is:

APY = (1 + r/n)^n – 1,

Where r is the annual interest rate, and n is the number of compounding periods per year.

APY is widely used across several sectors of decentralized finance (DeFi), particularly in areas where compounding plays a significant role in yield generation.

In summary, APY gives you a more accurate picture of your earning potential in crypto investments than APR does. It helps investors compare opportunities not just based on base interest rates, but also on how often returns are paid out and reinvested. For anyone navigating the world of DeFi, understanding APY is crucial to making informed decisions about staking, lending, and yield-generating strategies.

When to Choose APR-Based vs APY-Based Returns

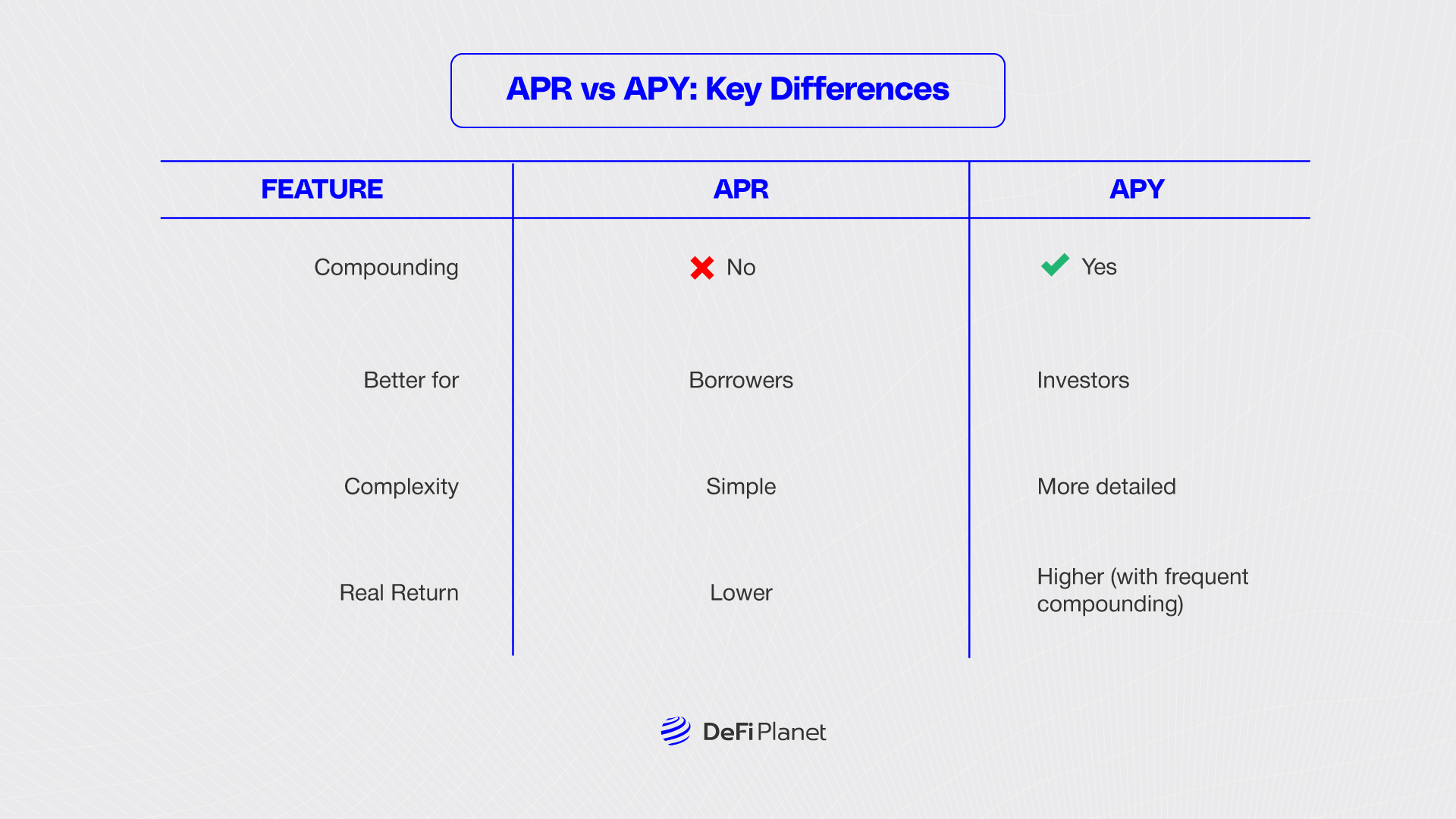

Whether APR or APY is better depends on your financial objective. Whether you’re looking to earn or borrow. A good rule of thumb is that APY is better for earning, while APR is better for borrowing, although the context always matters.

If your goal is to maximize returns, APY is the metric to watch. It’s most useful when:

- You’re staking tokens to earn rewards

- You’re providing liquidity to earn interest

- You want to grow your investment over time with the help of compounding

Because APY includes the effects of compound interest, it gives a more accurate picture of your real earning potential over a year. The more frequent the compounding, the higher your actual returns, making APY a valuable tool for long-term crypto investors.

On the flip side, if you’re planning to borrow crypto, then APR is the clearer, more practical metric. You should focus on APR when:

- You’re comparing loan costs between platforms

- You need to understand the base interest rate without any added complexities

- You prefer a straightforward estimate of what you’ll owe, without factoring in compounding

APR offers a transparent snapshot of borrowing costs, which is especially useful for budgeting and risk management.

In short, use APY to evaluate the full earning potential of an investment, and use APR to assess borrowing costs simply and clearly. So, again: Is it better to earn APR or APY? If you’re an investor, APY is generally better. If you’re a borrower, APR offers more transparency and predictability.

APR vs APY: Key Differences

Risks and Limitations of Advertised Returns

APR and APY in crypto may look attractive; some platforms advertise 20%+ APYs, but these numbers aren’t always guaranteed. Key risks to watch out for include:

1. Variable rates

DeFi platforms often adjust interest rates dynamically in response to supply and demand. This means a 15% yield today could shrink to just 4% tomorrow without warning.

Such fluctuations can significantly impact your expected returns, particularly in the short term.

2. Token volatility

High APY might look appealing, but if the token you’re earning crashes in value, you’re at a loss. Your returns are often calculated in crypto, not fiat, so that price swings can wipe out gains. It’s possible to end up with more tokens but less actual dollar value.

3. Impermanent loss

How does impermanent loss happen? When you provide liquidity to a pool, changes in the price ratio of the tokens can hurt returns. Even if APY is high, price divergence between paired tokens may reduce your end value. This “loss” isn’t realized until you withdraw, but it can offset earnings significantly.

4. Protocol risk

DeFi relies on smart contracts, which are vulnerable to coding errors or malicious exploits. If a protocol is hacked or fails, funds can be drained permanently within minutes. Even the most promising yields mean nothing if the platform loses user assets.

5. Misleading APY calculations

Some platforms advertise inflated APYs based on ideal compounding scenarios. They might not account for real-world limits like withdrawal fees or lock-up periods. Always check if the yield shown is realistic and achievable under your conditions.

Final Thoughts: Clarity Over Hype

APR and APY are like two sides of the same crypto coin—each telling a different part of the story. APR offers a straightforward, no-frills snapshot of the interest you’ll earn or owe over time, while APY gives a more complete picture by including the impact of compounding. In the fast-paced world of DeFi, that difference can significantly influence your returns or borrowing costs.

When exploring investment opportunities or taking out crypto loans, it’s important to prioritize clarity over hype. High APY figures may look attractive at first glance, but they can be misleading if you don’t understand how frequently interest is compounded or what assumptions are built into the projections. Always take the time to read the fine print, especially details about compounding frequency, and ensure you’re aware of any variables that could affect your actual earnings or liabilities.

Most importantly, don’t focus solely on advertised returns. The volatility of the underlying token can significantly impact your actual outcomes. A high APY isn’t worth much if the token’s value drops sharply. By looking beyond the surface and understanding both APR and APY in context, you’ll be better equipped to make smart, informed decisions that align with your financial goals.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you want to read more market analyses like this one, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}