Quick Breakdown:

- Crypto is forcing traditional banks to rethink their dominance, replacing institutional trust with transparency.

- Stablecoins and DeFi are cutting deep into banking’s core business, showing exactly why banks hate crypto.

- Many institutions are now adapting, proving that cryptocurrency and banking can coexist through innovation and tokenization.

- The key question isn’t destruction but evolution. Will cryptocurrency take over bank operations or redefine them entirely?

- Crypto is forcing traditional banks to rethink their dominance, replacing institutional trust with transparency.

Why Banks Can’t Ignore Crypto Anymore

For centuries, traditional banks held unquestioned power over money, deciding who could save, borrow, or send funds across borders. Then came crypto, flipping that system on its head. Instead of relying on institutional trust, it introduced a financial model that allowed anyone, anywhere, to transact without permission.

What began as a niche experiment has evolved into a $3.91 trillion market, according to CoinGecko’s 2024 Annual Crypto Report. This is a sign of maturity, not hype.

The approval of Bitcoin ETFs, the steady rise of institutional DeFi participation, and the growing number of CBDC pilots all point to one truth: digital assets are now embedded in global finance.

Crypto challenges banks at their core; in payments, lending, and custody. Cross-border transfers that once took days now settle in seconds on blockchain networks. DeFi platforms offer yields far beyond what savings accounts can match, while stablecoins process trillions in annual transactions, rivalling legacy systems.

This dynamic captures the new reality of blockchain and banking; a world where innovation meets regulation in real time. Banks can no longer afford to dismiss crypto as a speculative phase. A recent report shows 76% of financial executives now view digital assets as viable alternatives to fiat within the next decade.

Stablecoins and DeFi Eating into Banking’s Core Business

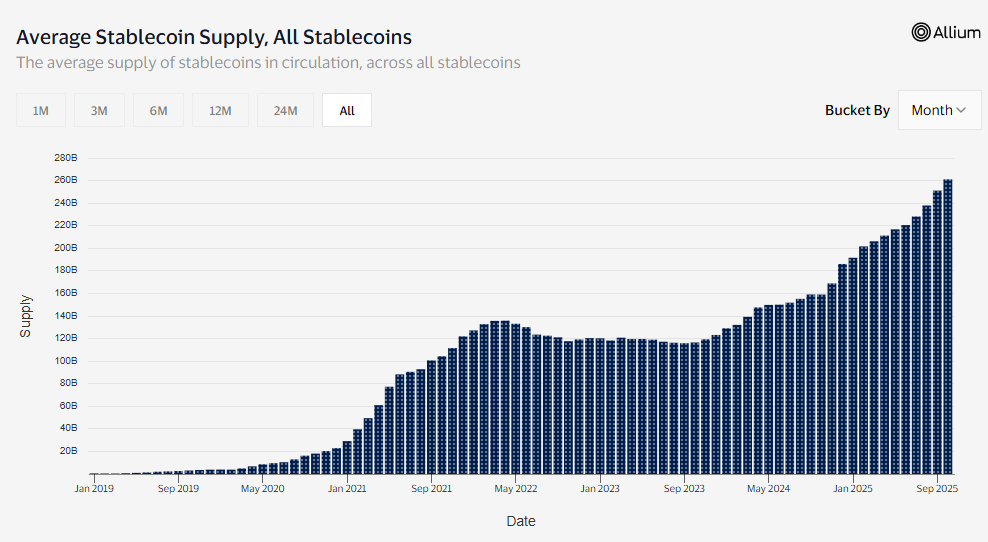

Stablecoins and decentralized finance (DeFi) are quietly reshaping the foundation of traditional banking. Acting as a bridge between crypto and fiat, stablecoins deliver what banks have long promised but struggled to perfect. Stablecoins offer instant, low-cost global payments. With over $240 billion worth of stablecoins in circulation, they are now powering remittances, business-to-business transfers, and even payrolls — moving money across continents in seconds, something banks can only dream of matching.

DeFi pushes this disruption even further. Built on smart contracts, it lets users lend, borrow, trade, or earn yield, all without a middleman. No credit checks, no paperwork, and no waiting for approvals. Everything happens on-chain, governed by transparent code instead of institutional bureaucracy. What once required a bank branch or a loan officer can now be done with a few clicks.

RELATED: DeFi is Eating TradFi

This transformation explains why banks hate crypto; not out of hostility, but out of fear of obsolescence. Realizing resistance is futile, traditional banks are starting to adapt. Many are experimenting with tokenization, transforming conventional assets like bonds, funds, and real estate into digital tokens that can be traded or settled instantly. These tokenized real-world assets (RWAs) represent the next frontier of cryptocurrency and banking— where the same technologies disrupting banks might also redefine their future.

How Banks are Adopting Crypto’s Playbook

Rather than fighting crypto, many traditional banks are now learning from it, borrowing its innovations, adapting its principles, and blending them with their own regulatory and operational strengths. The shift in mindset is clear: instead of competing with crypto, banks are choosing collaboration. By merging their institutional trust, compliance frameworks, and customer reach with blockchain’s speed, transparency, and programmability, they’re carving a new role for themselves inside the digital finance ecosystem, not outside it.

This shift reflects the deeper ties between cryptocurrency and banking. In 2022, BNY Mellon launched its Digital Asset Custody Platform in the U.S., allowing select clients to hold and transfer Bitcoin and Ethereum. By 2025, both BNY Mellon and State Street were discussing stablecoins, tokenization, and digital asset custody in their earnings calls, signalling that digital finance is no longer peripheral but central to their strategy.

Standard Chartered’s Zodia Custody bridges regulated banking with crypto-native systems, while Visa now supports stablecoin settlements on its network. Mastercard, on the other hand, has gone a step further, collaborating with multiple crypto firms and successfully tokenizing 30% of its transactions in 2024, effectively merging traditional payment rails with decentralized technology.

Beyond partnerships, banks are building dedicated digital asset divisions, experimenting with blockchain-based settlement systems, and investing in advanced security tools. These moves reflect a deeper evolution. Banks are not just defending against disruption — they are co-opting crypto’s core mechanics like tokenization, on-chain settlement, and cryptographic custody to future-proof their relevance in a rapidly digitizing financial world.

Can TradFi and DeFi Coexist, or is One Bound to Consume the Other?

The relationship between traditional finance (TradFi) and decentralized finance (DeFi) isn’t a battle for survival — it’s becoming a delicate balance of coexistence. While DeFi challenges the foundations of centralized finance, many established institutions are realizing they don’t have to choose between tradition and innovation. Instead, they’re blending both worlds. Banks and asset managers are quietly adopting blockchain technology to enhance efficiency and transparency, but without surrendering the centralized control that defines them.

This evolution raises a pressing question: Will cryptocurrency take over bank operations entirely or merely force them to evolve? The reality is more nuanced. Collaboration, not competition, seems to be the emerging trend.

The collaboration between SWIFT, UBS Asset Management, and Chainlink on a pilot for tokenized fund settlements is a prime example. Similarly, BlackRock is testing tokenized fund initiatives that merge traditional asset management with blockchain infrastructure. HSBC has also integrated blockchain into its gold trading and trade finance systems, showcasing how legacy players can innovate while maintaining oversight and compliance.

What’s emerging is not a decentralized overthrow, but a hybrid evolution, a financial ecosystem where banks selectively adopt crypto’s efficiency and transparency while preserving the trust, regulation, and structure that have long defined traditional finance. In this new phase, blockchain doesn’t replace banks; it refines them. The future of finance may not be “TradFi versus DeFi,” but rather a fusion, where the reliability of the old world meets the innovation of the new.

Disclaimer: This piece is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you want to read more market analyses like this, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

{kind=link}