Quick Breakdown

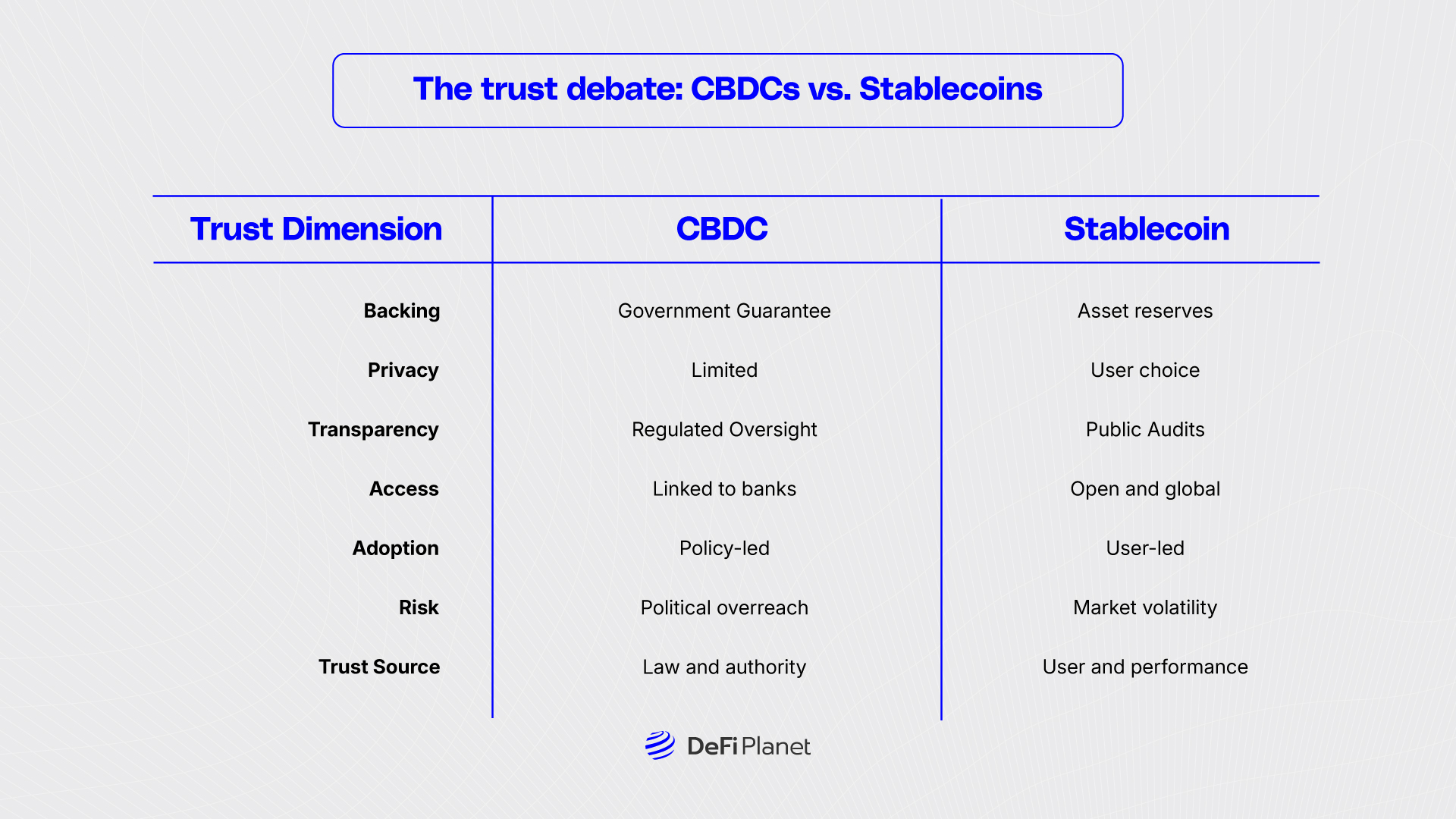

- CBDCs rely on legal authority and central bank credibility, promising stability but raising privacy concerns.

- Stablecoins thrive on real-world usage, liquidity, and transparency, but they also face regulatory uncertainty.

- Markets show higher revealed trust in stablecoins; CBDCs hold latent trust based on law and governance.

- The real battle: Can regulation balance control with innovation without breaking public trust?

Setting the Stage: When Money Loses Its Identity

Traditional money was once built on three invisible pillars: the authority of the state, the stability of banks, and the shared belief that our money would always hold value. Those foundations made the system feel natural and unquestionable. But the digital era has changed that. Today, new forms of money must earn trust on their own. This is where Stablecoins vs CBDCs come into play, each trying to prove that it deserves to be called “money,” not just code.

The debate now stretches beyond technology. It’s about who stands behind the promise of value, whether these systems can survive financial stress, and how much privacy users are willing to give up for efficiency. It also highlights a key question: what is the point of stablecoins? Are they simply digital dollars for traders, or are they shaping a new kind of financial inclusion? As both CBDCs and stablecoins evolve, the ultimate test will be where trust settles: with governments or with the marketplace.

The Tightrope of Control: CBDCs’ Promise and Paradox

A Central Bank Digital Currency, or CBDC, is the digital version of cash, fully backed by a central bank and recognized as legal tender. On paper, that gives it unmatched credibility. It could modernize payment systems, lower cross-border costs, and extend financial access. Yet this same authority raises tough questions about control and privacy.

If governments can monitor transactions, it could easily turn money into a tool of surveillance. That’s why many critics fear that CBDCs might sacrifice autonomy in exchange for stability. As Jerome Powell, Chair of the U.S. Federal Reserve, once warned, “We would not want a world where the government sees every transaction.”

CBDCs also introduce programmability, a feature that could be used to achieve policy goals such as automatic taxation or spending limits, but that also risks abuse. The difference between governance and overreach can be dangerously thin. This is where the tension between Stablecoins and CBDCs becomes clear. CBDCs may promise order, but without trust, even authority loses power.

Stablecoins: The Market’s Lean, Mean, Digital Dollar

Stablecoins didn’t come from governments; they came from market demand. As crypto trading grew, users needed a stable bridge between volatile assets and fiat money. Stablecoins provided that link. They are fast, borderless, and programmable. Their rise shows precisely what stablecoins are for: they give users a digital version of the dollar that works across platforms and countries.

According to Coinbase’s State of Crypto Q2 2025 report, stablecoin supply has reached $247 billion, a 54% increase in a year. The U.S. Treasury expects it could grow to $2 trillion by 2028, proving the scale of Stablecoin adoption. Yet trust remains the foundation. A stablecoin is only as reliable as its reserves. The collapse of Terra/Luna reminded everyone how fragile this system can be when the backing is unclear.

Also Read: Stablecoins in 2025: Still Depegging or Finally Stable?

The Bank for International Settlements (BIS) has been among the sharpest critics, arguing in its Annual Economic Report 2025 that stablecoins fall short on three essential monetary qualities: singleness, elasticity, and integrity.

Still, Stablecoin adoption continues to rise because the market rewards transparency and performance. Standard Chartered predicts that by 2028, up to $1 trillion could flow out of emerging-market bank deposits and into stablecoins, as citizens seek stability and digital accessibility that their local currencies can’t offer.

The Trust Gap: Authority vs. Authenticity

CBDCs gain trust through law. When a government says its currency is valid, most people accept that. But in the digital age, users want proof, not promises. That’s why Stablecoin adoption is growing — it relies on transparency, open audits, and real-time performance rather than authority alone.

Private stablecoin issuers have to earn credibility every day. Their value depends on how well they maintain their peg, even when markets shake. Meanwhile, CBDCs have the comfort of central backing, but that can also mean slower innovation. The core of Stablecoins vs CBDC lies here: one is built on legal trust, the other on user trust.

Regulation plays a middle role. Where oversight is clear, users feel secure. Where it’s vague or political, confidence weakens. In the end, both sides are learning the same lesson — trust cannot be legislated, it must be lived. And that is exactly the point of stablecoins: to prove that reliability and transparency can coexist with innovation.

Also Read: Stablecoins vs. CBDCs: Why Governments Are Picking Sides in the Future of Money

The Trust Debate: CBDCs vs. Stablecoins

Deciding the Winner: Trust as the Battleground

Trust is not fixed. It’s something built and tested over time. Right now, the market shows stronger revealed trust in stablecoins, driven by their liquidity and proven use. CBDCs, however, carry what could be called latent trust—faith in institutions and laws that have yet to be fully tested in the digital world.

This ongoing contest between Stablecoins and CBDCs is more than a policy debate. It’s a philosophical one. It asks whether the future of money should be led by authority or by authenticity. Stablecoin adoption suggests people increasingly trust what they can verify, not just what they’re told to believe.

Ultimately, both models may coexist, each serving different needs. But the one that wins in the long term will be the one that earns and sustains trust —not just through promises, but through performance.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you want to read more market analyses like this one, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

{kind=link}