Last updated on November 18th, 2025 at 11:11 am

Cryptocurrencies are gaining traction across Africa, providing innovative solutions to persistent financial issues like inflation, currency devaluation, and limited banking access. Between July 2023 and June 2024, Sub-Saharan Africa received an estimated $125 billion in on-chain crypto value, showcasing the region’s active engagement with digital assets. Africa also leads globally in the use of DeFi platforms, as people seek accessible and efficient financial tools to manage finances, save, and invest.

Among African nations, Nigeria stands out as a key player in the crypto space, but other countries, such as Ethiopia, Kenya, and South Africa, are also making significant strides. This raises an intriguing question: which country is poised to lead the crypto revolution on the continent?

Nigeria: The Current Leader in Crypto Adoption

Nigeria’s prominence in the global crypto space is undeniable. The country ranks second worldwide for crypto adoption, driven largely by its economic challenges, including high inflation and the devaluation of the Naira. Cryptocurrencies, particularly stablecoins, have become a popular means for Nigerians to preserve wealth, bypass traditional banking systems, and participate in the global digital economy. From July 2023 to June 2024, Nigerians received approximately $59 billion worth of cryptocurrencies.

Nigeria’s large, tech-savvy population, paired with its burgeoning digital economy, positions the country as a potential leader in Africa’s crypto growth. The government has made strides to regulate the crypto market, but regulatory inconsistencies remain a challenge. Additionally, limited public financial education hampers broader adoption. Despite these obstacles, Nigeria’s achievements set a benchmark for others, while countries like Ethiopia, Kenya, and South Africa are rising quickly with their own advancements in crypto adoption.

Ethiopia: From Cautious Policies to Blockchain Ambitions

Ethiopia, Africa’s second-most populous nation, has shifted from cautious crypto policies to actively embracing blockchain technology. In February 2024, Ethiopian Investment Holdings (EIH) partnered with Hong Kong-based West Data Group in a $250 million project to develop Bitcoin mining and AI infrastructure. By October, Ethiopia contributed 2.25% of Bitcoin’s global hash rate, supported by 600 megawatts (MW) of energy from Ethiopian Electric Power.

Ethan Vera, co-founder of Luxor Mining, highlighted Ethiopia’s potential to expand its Bitcoin mining capacity significantly. Ranked fourth globally in mining hash rate, Ethiopia trails only the United States, Hong Kong, and Asia. This marks the nation’s ambition to position itself as a leader in Africa’s growing data centre sector, expected to reach $5.4 billion by 2027. Ethiopia’s strategic focus on technology and energy investments underscores its potential to lead crypto adoption in East Africa.

Ethiopia’s government has also prioritized the integration of blockchain technology into public services, including education and agriculture, which could have far-reaching impacts on the economy. These initiatives showcase Ethiopia’s commitment to using technology to drive economic transformation and its potential to play a pivotal role in Africa’s digital future.

Kenya: Leveraging Mobile Technology for Crypto Growth

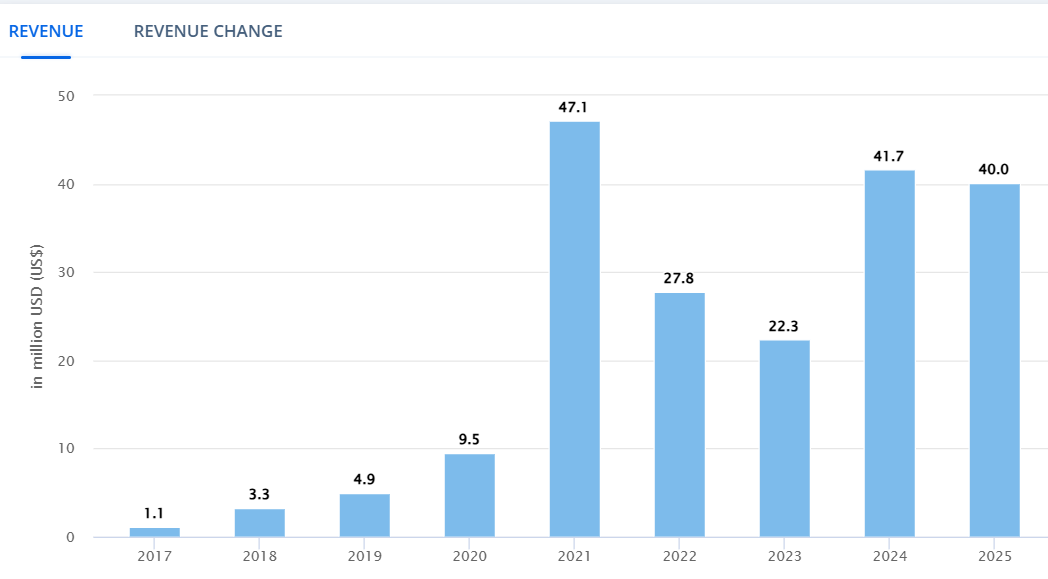

Kenya’s cryptocurrency market has witnessed explosive growth in recent years. By the end of 2024, the market is projected to generate approximately $41.7 million in revenue, with an average revenue per user (ARPU) of $57.2. This growth is fueled by Kenya’s tech-savvy population and the widespread adoption of M-Pesa, the world’s most-used mobile money service.

Kenya Crypto Revenue Forecast Source: Statista

Cryptocurrencies offer Kenyans a cheaper, faster, and more accessible alternative to traditional banking systems, which are often plagued by high fees and limited access. They are particularly useful for remittances, a critical source of income for many Kenyan families. With its robust mobile technology ecosystem and increasing crypto adoption, Kenya is well-positioned to become a leader in Africa’s digital financial transformation.

Additionally, Kenya’s government has shown a willingness to explore blockchain technology for various sectors, including land registry and healthcare. This proactive approach to integrating digital innovations further strengthens Kenya’s case as a potential leader in Africa’s crypto space. However, challenges such as regulatory gaps and cybercrime need to be addressed to sustain this growth.

South Africa: Regulation and Everyday Transactions

South Africa is another key player in Africa’s crypto revolution. The country recently granted 59 licenses to crypto businesses, officially recognizing digital currencies as financial products. This regulatory clarity makes South Africa one of the more structured markets for cryptocurrencies on the continent.

South African companies like VALR, Luno, and Altify are driving crypto adoption by facilitating investments and enabling stablecoin transactions for everyday use. Platforms such as Binance Pay and FiveWest have integrated crypto payment options, leading to a 26.5% increase in transaction volumes by mid-2024. The inclusion of stablecoins in official regulations further underscores South Africa’s commitment to fostering a secure and innovative crypto ecosystem.

South Africa’s approach to regulation has made it a role model for other African countries looking to create a safe and investor-friendly crypto market. By balancing innovation with consumer protection, the country demonstrates how regulatory frameworks can support the growth of digital finance while mitigating risks. As more South Africans embrace cryptocurrencies for everyday transactions, the nation is solidifying its position as a key player in Africa’s crypto future.

Other Rising Contenders: Ghana and Beyond

Ghana is another African nation making significant strides in crypto adoption. P2P trading has surged, with Chainalysis reporting that Ghana could soon rival Nigeria in crypto usage due to similar economic challenges like inflation and currency instability.

Ray Youssef, CEO of Paxful, sees Ghana as a rising leader in cryptocurrency adoption in Africa. He points to a 400% increase in trading volume on Paxful’s P2P platform over the past two years as evidence of growing interest. Youssef attributes part of this surge to the active involvement of Nigerians, many of whom visit Ghana and share their knowledge of Bitcoin and other cryptocurrencies with the local population.

Other countries, such as Uganda and Rwanda, are also making notable advancements. Uganda’s efforts to explore blockchain technology for supply chain management and Rwanda’s initiatives in integrating blockchain for public services signal their potential to contribute to Africa’s crypto landscape. While these nations are still in the early stages of adoption, their proactive approaches highlight the widespread interest in digital finance across the continent.

Challenges Hindering Crypto Adoption in Africa

While African countries are making notable progress, several challenges hinder the potential for widespread cryptocurrency adoption.

1. Regulatory Uncertainty

The regulatory landscape for cryptocurrencies in Africa remains inconsistent. Some governments embrace the technology, while others impose outright bans or restrictive policies. For instance, Nigeria has taken steps to regulate crypto exchanges but has also introduced conflicting policies that create uncertainty. This lack of a unified framework deters investors and startups, stalling the growth of the crypto market.

Governments need to develop clear, consistent, and supportive policies to foster a thriving crypto ecosystem. Collaborative efforts among African nations to create a Pan-African regulatory framework could accelerate adoption and reduce the risks associated with fragmented policies.

2. Infrastructure and Education Gaps

Despite booming fintech sectors in urban areas, many regions in Africa lack adequate digital infrastructure. Rural communities often have limited internet access and basic banking services. Additionally, a significant portion of the population lacks financial literacy, making it challenging for them to understand and safely use cryptocurrencies. Public education initiatives are essential to bridge these gaps and ensure that crypto adoption benefits all.

Efforts to improve internet connectivity and expand access to affordable smartphones could play a crucial role in overcoming these challenges. Partnerships between governments, private companies, and international organizations are necessary to address these infrastructure gaps and promote digital inclusion.

3. Security and Fraud Risks

The rise of cryptocurrencies in Africa has been accompanied by increased security concerns. Scammers and fraudsters exploit the decentralized nature of digital assets, with Ponzi schemes and fraudulent ICOs becoming prevalent. The absence of robust consumer protection laws exacerbates these issues, making it crucial to strengthen regulations and improve security protocols to safeguard investors.

Public awareness campaigns about the risks associated with crypto investments and the importance of using reputable platforms can also help mitigate security challenges. Additionally, governments and private companies must collaborate to develop advanced cybersecurity measures and legal frameworks for dispute resolution.

The Path Forward: Who Will Lead the Crypto Revolution?

Nigeria currently leads Africa’s crypto revolution, thanks to its large population, tech-savvy youth, and expanding digital economy. However, maintaining this leadership requires clear policies, robust infrastructure, and widespread public education to foster a stable and inclusive crypto ecosystem.

Ethiopia’s ambitious blockchain projects, Kenya’s mobile technology-driven growth, and South Africa’s regulatory advancements position these countries as strong contenders. Ghana’s rise in P2P trading further highlights the dynamic and competitive landscape of crypto adoption in Africa. Additionally, emerging players like Uganda and Rwanda illustrate the continent’s collective potential to drive global crypto adoption.

The next few years will be pivotal in determining which country emerges as the leader. A unified Pan-African approach to crypto regulation and innovation could accelerate adoption and ensure the continent’s prominence in the global digital economy. By addressing existing challenges and leveraging their unique strengths, African nations can collectively shape the future of cryptocurrencies and digital finance.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you would like to read more market analyses like this, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}

{kind=link}