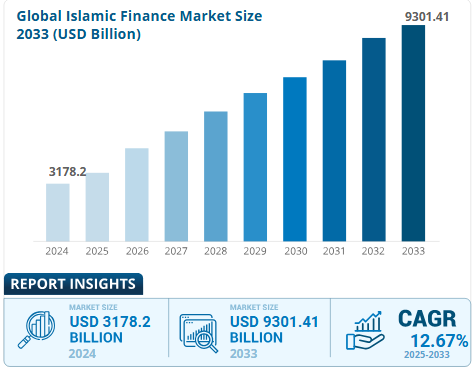

Islamic finance, rooted in principles of fairness, risk-sharing, and ethical responsibility, is increasingly finding common ground with blockchain in Islamic finance. Decentralized finance is redefining traditional banking, increasing the potential for a more transparent, secure, and inclusive financial ecosystem. However, aligning the foundational ethics of Islamic finance with the evolving blockchain sector presents unique challenges and opportunities. The Islamic finance market, valued at USD 3178.2 billion in 2024, is projected to grow to USD 9301.41 billion by 2033, meaning there’s a lot of room for innovation.

This article explores the intersections of these two worlds, addressing the ethical challenges, potential synergies, and technological breakthroughs that could reshape financial systems for billions of people worldwide.

The Clash of Principles – Understanding the Core Conflicts

Islamic finance, with its deep roots in principles of fairness, transparency, and social responsibility, stands on a foundation that might seem worlds apart from cryptocurrency’s fast-paced, roller-coaster system.

At its core, Islamic finance strictly prohibits riba (interest), gharar (excessive uncertainty), and maysir (speculative gambling) – pillars designed to promote ethical, risk-sharing, and asset-backed financial activities. This means that every transaction must have a clear purpose, tangible backing, and a fair distribution of risk and reward, aligning closely with real economic activity rather than speculative profit. This core approach reflects the main concept of Islamic finance, which emphasizes real asset backing and mutual risk-sharing.

In contrast, cryptos like Bitcoin and many of its digital siblings often thrive on speculative trading and rapid price swings, raising eyebrows in the Islamic finance community. The concept of riba is particularly challenging in this context. While a Bitcoin transaction itself doesn’t necessarily involve interest, many crypto-based financial products, such as lending protocols and staking mechanisms, generate returns that can resemble interest payments, potentially clashing with Shariah’s strict prohibition on unearned profit.

Gharar, or the prohibition against excessive uncertainty, is another tricky area. The crypto market’s notorious volatility, where prices can soar or crash within hours, introduces a level of unpredictability that can be unsettling from an Islamic perspective on cryptocurrency. This is especially concerning when speculative bubbles form, as seen during the 2017 and 2022 bull runs, where fortunes were made and lost in a matter of weeks.

Then there’s maysir – the prohibition of gambling, which adds another layer of complexity. For many, the speculative nature of trading meme coins or high-risk altcoins can feel uncomfortably close to placing a bet at a casino, making it challenging to reconcile such practices with Islamic ethics.

Related: Does Cryptocurrency Encourage a Gambling Mentality in Investments?

However, not all hope is lost…despite these conflicts, the divide is not absolute. The same blockchain technology that powers these speculative markets also holds the potential for creating transparent, risk-sharing financial systems that align more closely with Islamic principles.

The rapid evolution of blockchain in Islamic finance has sparked creative efforts to bridge these gaps, offering a glimpse into a future where the ethical finance principles of Islam and the decentralized ideals of crypto might find common ground. It’s a challenging but exciting path, one that requires innovative thinking and a commitment to upholding both transparency and fairness in a rapidly changing financial landscape.

Potential Synergies and Innovations – Sharia-Compliant Crypto Solutions

Despite the apparent philosophical clashes, there’s significant potential for synergy between blockchain in Islamic finance and Islamic finance itself. Both systems emphasize transparency, fairness, and decentralized control, creating a natural foundation for innovation. Blockchain’s ability to create tamper-proof, verifiable transaction records aligns well with the Islamic perspective on cryptocurrency, which demands transparent and honest dealings. This technological backbone can support the creation of Sharia-compliant financial products that address key ethical concerns while leveraging the efficiency of DeFi protocols.

One standout example is Islamic Coin (ISLM), which operates on the Haqq network —a project explicitly designed to align with Islamic ethics. ISLM takes a unique approach to balancing profit with purpose, allocating a portion of every newly minted coin to the Evergreen DAO, a DAO that funds charitable projects globally. This structure mirrors the Islamic principle of zakat, the obligation to give a portion of one’s wealth to support those in need. blockchain in Islamic finance can directly support ethical finance. This innovation also addresses the concern around riba, as the network discourages interest-based returns, aligning more closely with Islamic values.

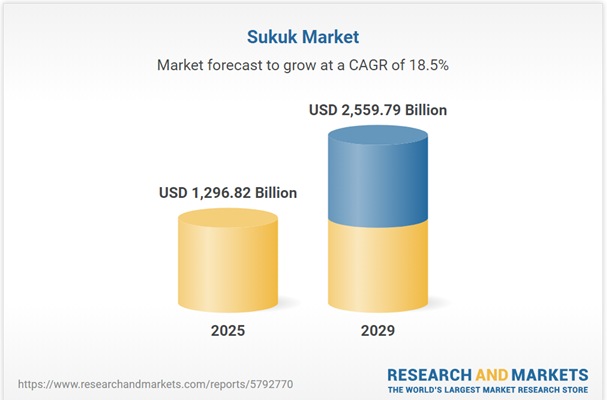

The global Sukuk market, on track to hit $2.55 billion by 2029, underscores the growing demand for ethical financial solutions.

Blockchain’s role in enabling more efficient and transparent Sukuk issuances further strengthens its potential as a key enabler of Islamic finance innovation. By tokenizing assets like real estate or gold, Islamic finance institutions can create asset-backed investment products, adhering to core Islamic principles and reducing speculation. This reflects blockchain’s capacity to bridge traditional financial ethics with modern technological solutions, creating new pathways for ethical investment.

The profit-and-loss sharing (PLS) models, which are central to Islamic finance, can be efficiently implemented using smart contracts. These self-executing contracts can enforce profit-sharing agreements, reducing the need for intermediaries and enhancing transparency. For example, a decentralized, blockchain-based Mudarabah (partnership) structure can automatically distribute profits based on pre-agreed terms, ensuring that investors share in both the risks and rewards, thus avoiding riba and speculative excess.

By blending these technological innovations with the foundational principles of Islamic finance, blockchain offers a pathway to create robust, transparent, and ethical financial systems.

The Role of Stablecoins – Balancing Stability and Shariah Compliance

Stablecoins offer a way to mitigate the volatility often associated with cryptocurrencies, directly addressing the Islamic finance prohibitions against excessive uncertainty (gharar) and speculative risk (maysir). These digital assets are typically pegged to stable, tangible assets like fiat currencies (e.g., USDT, USDC) or precious metals (e.g., gold-backed tokens), creating a more predictable and transparent financial instrument.

For instance, gold-backed stablecoins like PAX Gold (PAXG) or Tether Gold (XAUT) offer digital representations of physical gold holdings, providing investors with the security of a tangible asset while leveraging the transactional efficiency of blockchain technology. This approach aligns closely with the Islamic finance requirement for asset-backed transactions, ensuring that every unit of digital currency corresponds to a real, physical asset, reducing the speculative nature that often characterizes conventional cryptocurrencies. Such stable, asset-backed investments are not only more compliant with Shariah principles but also offer a clear audit trail, thereby further enhancing transparency and trust —critical elements in Islamic finance.

Stablecoins can play a crucial role in facilitating efficient cross-border transactions. With an estimated 1.9 billion Muslims worldwide, many of whom rely on international remittances, stablecoins offer a faster and more cost-effective alternative to traditional banking systems. This efficiency reduces reliance on interest-based financial institutions, addressing another critical Islamic finance principle. For example, UAE-based OneGram has developed a gold-backed cryptocurrency that aims to provide a Sharia-compliant digital payment solution, supporting cross-border commerce and financial inclusion within the Islamic world.

Regulatory Challenges and Ethical Considerations

Navigating the regulatory landscape for blockchain in Islamic finance is no small feat. One of the biggest challenges lies in the lack of standardized guidelines for integrating these technologies within the Shariah framework. Unlike conventional finance, where regulations are relatively uniform across major markets, Islamic finance faces a unique hurdle – the diverse interpretations of Shariah law across different regions. This variation can make it challenging to develop universally accepted financial products, as what is considered permissible (halal) in one jurisdiction might be viewed as non-compliant (haram) in another.

For instance, a blockchain-based financial product that complies with Malaysian Shariah standards might face challenges gaining acceptance in Saudi Arabia or Indonesia, where interpretations of Islamic law can differ significantly. This lack of standardization not only complicates product design but also increases the compliance burden for financial institutions looking to enter multiple markets. Without a clear, unified framework, the adoption of blockchain solutions in Islamic finance remains slow and cautious.

Regulatory uncertainty is also a significant barrier. Many Islamic financial institutions remain hesitant to embrace blockchain due to the absence of clear, supportive guidelines from regulatory bodies. This uncertainty can stifle innovation, as businesses are unlikely to invest in new technologies without confidence that their efforts will be deemed Shariah-compliant. It also creates operational challenges, as firms must constantly navigate shifting regulatory landscapes to remain compliant.

Beyond the technical and regulatory hurdles, there is also the critical question of ethical use. Islamic finance is deeply rooted in social responsibility and the promotion of the common good, making it essential that blockchain technology is not used to facilitate unethical or harmful activities. This includes ensuring that funds are not directed towards industries considered impermissible under Islamic law, such as alcohol, gambling, or interest-based lending. It also means leveraging blockchain’s transparency to prevent fraud, corruption, and financial crime, aligning the technology’s capabilities with the ethical principles at the heart of Islamic finance.

Despite these challenges, the potential for blockchain to transform Islamic finance remains significant. With the right regulatory frameworks, a commitment to ethical practices, and a focus on technological innovation, this emerging field has the potential to redefine financial inclusion and economic justice for billions of people worldwide.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you want to read more market analyses like this one, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}

{kind=link}