Last updated on December 29th, 2024 at 03:04 pm

The crypto industry is at a pivotal moment. Once hailed as a beacon of financial freedom, it now grapples with regulatory pressures that threaten to dilute its revolutionary ideals. Policies like Know Your Customer (KYC) and Anti-Money Laundering (AML) checks, once anathema to the crypto ethos, are becoming the norm.

For many, these measures feel like a betrayal of crypto’s original promises. The anonymity that once defined digital currencies is being eroded, replaced by layers of compliance that echo the traditional financial system’s bureaucratic control.

However, this tide of regulations focused on the crypto industry doesn’t look like it will stop anytime soon. This is prompting us to ask: is crypto losing its revolutionary identity and becoming merely an extension of the system it meant to disrupt?

Regulatory Pressure and the Push Towards Centralization

The rapid rise of cryptocurrency has brought concerns over illicit activities, consumer protection, and financial stability into the regulatory spotlight. Governments have responded with a patchwork of measures, from outright bans to carefully crafted compliance frameworks.

Many countries are actively pressuring cryptocurrency platforms to comply with stricter regulations. In the United States, exchanges must register with bodies like FinCEN and enforce KYC protocols, tying user activity to verified identities. The European Union’s Markets in Crypto-Assets (MiCA) regulation require platforms to adopt similar standards. Meanwhile, China has gone a step further, banning crypto mining and trading outright, citing concerns about financial risk and energy consumption.

Compliance to the regulations comes at a cost, especially for platforms committed to decentralization. Take the example of Uniswap, a leading decentralized exchange (DEX). Initially celebrated for allowing peer-to-peer trading without third-party oversight, it has faced growing pressure to implement KYC measures. Similar challenges confront SushiSwap and Balancer, platforms founded on ideals of user privacy. This trend has pushed cryptocurrency closer to the norms of centralized finance, undermining its promise of autonomy.

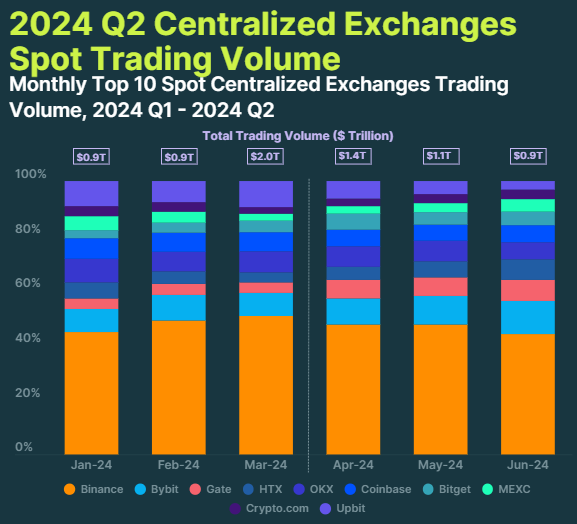

We can also see this in how centralized exchanges (CEXs) continue to dominate a large share of trading activity in the crypto market. Binance, Coinbase, and other major players accounted for a staggering $9.12 trillion in trading volume in March 2024 alone.

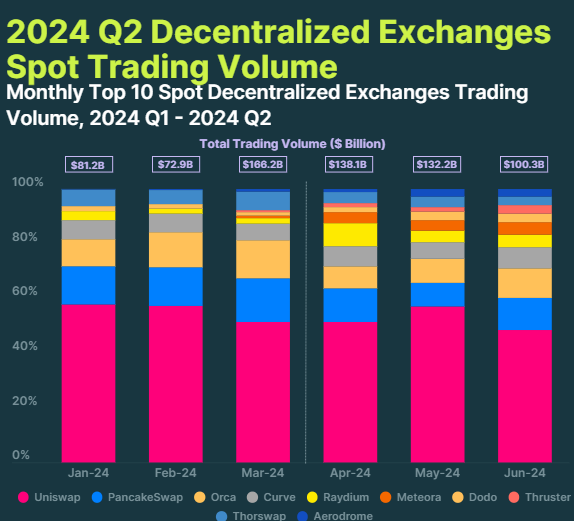

In contrast, DEXs—though promising—remain overshadowed. The top ten DEXs reported $370.7 billion in trading volume during Q2 2024, a notable 15.7% increase over the previous quarter but still dwarfed by CEX’s $3.40 trillion in the same period.

The Balance Between Privacy and Security

Cryptocurrency’s initial appeal stemmed largely from the privacy it offers.

Traditional banking systems require intermediaries and, by extension, monitoring and data sharing with third parties. Cryptocurrencies, however, were designed to give users control over their finances without surveillance or oversight, providing a way to transact outside the watchful eyes of governments and institutions. For many early adopters, this privacy wasn’t just a feature—it was a core value. By keeping transactions anonymous, crypto provided a degree of personal freedom and financial independence, especially valuable to those in countries with restrictive regimes or unreliable financial systems.

However, governments argue that unchecked privacy in financial systems can lead to severe risks, primarily by enabling illicit activities like money laundering, tax evasion, and financing terrorism. The anonymity of cryptocurrency transactions makes it harder for law enforcement agencies to trace transactions, identify suspects, and prevent unlawful behavior.

As a result, regulators are increasingly demanding that crypto platforms adopt measures like KYC and AML checks to ensure that transactions are secure and legal. For them, KYC/AML regulations are necessary to uphold security and maintain trust in financial systems.

Consider Tornado Cash, a privacy tool blacklisted by the U.S. Treasury Department for allegedly facilitating money laundering. Its ban has sparked debate about whether financial privacy tools should exist if they can also be used for illegal activities.

The Cost of Compliance

While compliance may enhance security and consumer trust, it imposes significant costs on the cryptocurrency ecosystem.

It’s important to consider how far-reaching regulations might influence innovation within the crypto space. Overly restrictive compliance measures could drive away developers and hinder the creation of new, privacy-preserving technologies. If governments enforce rigid standards without accommodating crypto’s unique features, developers may abandon projects or move operations to more crypto-friendly regions. Such a “brain drain” could stunt innovation, leading to a crypto landscape where only the most centralized or compliant projects thrive—an outcome that runs counter to the decentralization ideals at the heart of cryptocurrency.

Smaller projects and startups face prohibitive costs to meet compliance standards, reducing innovation in the space. For example, a blockchain startup in the United States must navigate a web of state and federal regulations, often requiring substantial legal and operational budgets to remain compliant.

Established platforms like Coinbase spend millions annually to comply with global regulations. This diverts resources away from product development and into legal compliance, slowing the pace of innovation. On the other hand, while their compliance with regulatory requirements reassures governments and mainstream users, it also reinforces centralization, making them gatekeepers of the crypto ecosystem.

In regions with limited access to documentation or financial infrastructure, KYC requirements can block users from accessing crypto services. For instance, individuals in war-torn or economically unstable regions often lack the identity documents required by major exchanges, excluding them from financial systems.

Can Crypto Stay True to Its Roots?

The future of cryptocurrency hinges on its ability to reconcile its revolutionary vision with the realities of regulation. But can cryptocurrencies maintain true independence and freedom within a regulated framework?

The challenge lies in developing oversight that protects users without stifling the innovation and freedom that make cryptocurrency revolutionary.

Industry leaders think it is possible with thoughtful regulatory evolution. PayPal’s Stephanie Desanges argues that decades-old regulatory frameworks cannot adequately address modern technology. Commissioner Hester Peirce of the U.S. Securities and Exchange Commission (SEC) says regulations can and should be tailored to cryptocurrency’s unique characteristics in a way that emphasizes user protection and market integrity while preserving decentralization.

However, the road ahead is fraught with challenges. Overregulation risks driving innovation underground or offshore, where projects may face fewer restrictions but also reduced legitimacy. Striking the right balance will require collaboration between regulators, developers, and the broader crypto community.

The stakes are high. As governments and platforms navigate this evolving landscape, the choices they make will shape the future of digital finance. Will cryptocurrency fulfill its original vision as a decentralized alternative, or will it become a mirror of the very system it set out to disrupt? Only time—and collective effort—will tell.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you would like to read more market analyses like this, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}

{kind=link}