Last updated on May 5th, 2025 at 11:52 am

Financial inclusion means ensuring everyone has access to basic financial services like saving, sending, and receiving money. This is especially important for the 1.4 billion people worldwide who don’t have a traditional bank account or don’t have access to reliable banking services. Without financial services, people face limitations in managing everyday expenses and planning for the future.

Blockchain technology and cryptocurrency have recently emerged as a possible solution to this problem. By offering decentralized platforms, crypto could allow people to access financial services without needing a bank. For example, with just a smartphone and internet connection, someone can use a digital wallet to save, send, and receive funds. These transactions are often cheaper than traditional banking methods, which could help people with limited resources save more and spend less on transaction fees.

However, there’s still a big question: does crypto really help improve financial access for those who need it most, or is it mostly used by people who already have some tech knowledge and resources?

Successes of Crypto in Advancing Financial Inclusion

Cryptocurrencies are helping to bring financial services to people who don’t have access to banks, especially in areas like Africa, Southeast Asia, and Latin America, where traditional banking is either limited, too expensive, or simply unavailable. In these regions, many people lack access to essential financial services due to economic instability, high banking fees, or geographic barriers.

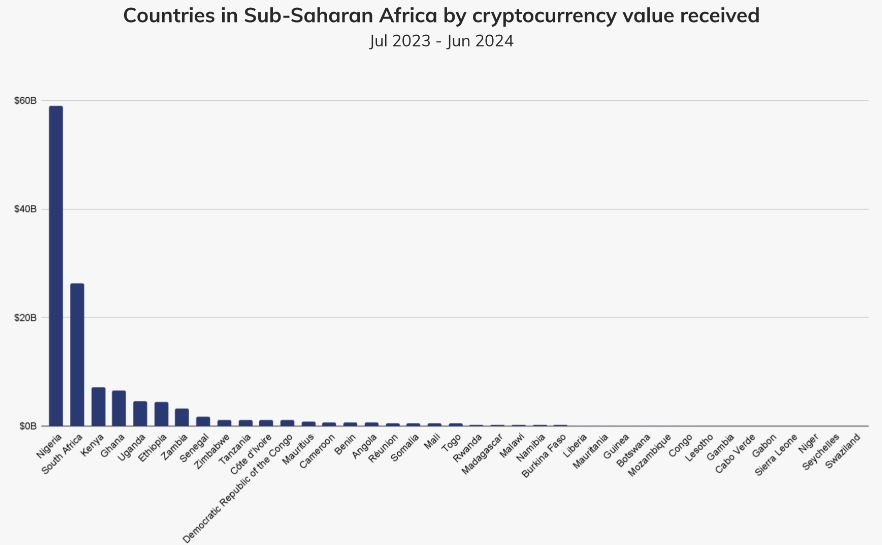

Crypto adoption is growing quickly in African countries like Nigeria, Ghana, and South Africa. Many people are turning to stablecoins because they hold their value more reliably, which helps protect against inflation and unstable local currencies. In 2024, stablecoins became especially popular in Nigeria; the country accounted for around 43% of all crypto transactions across Sub-Saharan Africa.

Since bank access is limited in many areas, people are turning to crypto for sending and receiving money across borders, something that’s essential in a region where traditional transfer fees are often high. Platforms like Korapay help users make cross-border payments using cryptocurrencies like Bitcoin, pegged to the U.S. dollar for stability, so they don’t have to worry about inflation or unstable local currencies.

In Southeast Asia, crypto adoption is rising fast in places like the Philippines and Vietnam, where tech-savvy communities and supportive regulations make it easier for people to use digital assets. Many Filipinos, for instance, use blockchain to send money home without the high fees of traditional remittance services. Similarly, people in Vietnam use crypto to save and transfer funds more efficiently, avoiding the long wait times and costs of conventional banking.

In Latin America, crypto has become essential for financial stability, especially in countries facing hyperinflation like Argentina and Venezuela. Here, people use crypto to avoid the rapid loss of value in their local currencies. In El Salvador, Bitcoin is even recognized as legal tender, which allows people to use it for everyday purchases and banking, highlighting how crypto can fill gaps left by traditional banks.

Lower Barriers for Cross-Border Transactions

Cryptocurrency has made cross-border transactions much easier and cheaper, providing a faster, low-cost alternative to traditional financial services. Sending money internationally through traditional remittance services often comes with high fees, especially for smaller amounts. For example, sending $200 this way usually costs around 6% in fees, which is double the United Nations’ target of 3% for affordable remittances. These fees weigh heavily on migrant workers and people regularly sending money back home to support their families.

In comparison, blockchain and crypto platforms enable users to send money almost instantly and at a fraction of the traditional cost. Many blockchain transactions reduce fees by up to 80%, which is a huge help for communities with limited access to banks, like those in parts of Africa and Southeast Asia, where demand for crypto has been growing.

Platforms such as Paxful and Luno have emerged as go-to services for these remittances, allowing people to convert crypto directly to local currency. This peer-to-peer exchange model can also provide more favorable exchange rates, helping some users receive up to 20% more value compared to traditional currency exchanges.

Empowering Financial Independence

DeFi is making it easier for people to take control of their money by removing the need for intermediaries or traditional banks. It’s done through blockchain technology, which runs on “smart contracts.” These are automatic programs that execute financial transactions transparently and securely.

A major benefit of DeFi is its potential to help people who don’t have access to traditional banks. For instance, DeFi platforms allow people to borrow money against their digital assets without needing a credit check. This opens up financial opportunities for people who, due to location, lack of credit, or high fees, can’t use regular banking services.

DeFi’s setup also lowers transaction costs, making it easier for anyone globally to participate in financial services. People in remote areas or underserved communities can use DeFi to save, access credit, and invest. This could boost financial independence and support small businesses in places where banking isn’t widely available. However, DeFi does come with some risks, like market fluctuations and regulatory challenges, so users should be cautious as the field continues to grow and change.

Challenges Limiting Crypto’s Role in Financial Inclusion

One major issue holding back cryptocurrency’s role in financial inclusion is the high transaction fees on popular blockchains like Ethereum. These fees, known as “gas fees,” can vary a lot depending on how busy the network is and how complex the transaction is. For example, sending Ethereum (ETH) can cost between $1 and $5 when the network is not busy, but during peak times, the cost can rise to $50 or more, especially when using dApps or smart contracts.

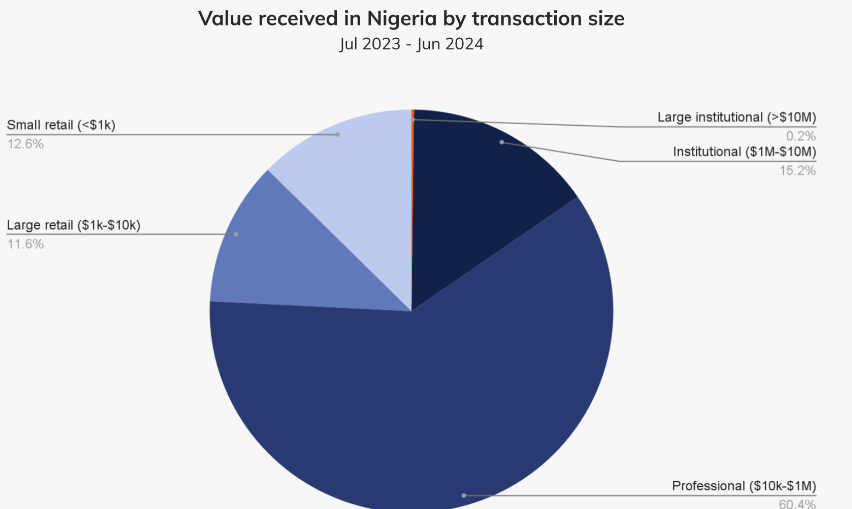

This creates a big problem for small transactions, especially in places like Nigeria where people rely on crypto for daily payments or sending money back home. In Nigeria, most crypto activity comes from smaller retail and professional-sized transactions. About 85% of the total value of transfers involves amounts under $1 million. The high gas fees make it expensive to send even small amounts, reducing the ability of crypto to help with financial inclusion.

Thankfully, there are solutions like Layer 2 networks that are helping fix this. Layer 2 technologies, such as Optimistic Rollups and zk-Rollups, work on top of Ethereum’s blockchain and handle transactions off-chain. This helps reduce the load on the main network and lowers costs. Other blockchains, like Binance Smart Chain, Solana, and Polygon, also offer cheaper and faster transactions compared to Ethereum. These developments are making crypto more accessible and affordable, especially for people in need of low-cost financial services.

Complexity and Accessibility Barriers

Using cryptocurrency can be tough, especially for newcomers, because of the complexity and various barriers to entry. Some of the biggest challenges include managing crypto wallets, keeping private keys safe, and understanding how DeFi platforms work.

Managing a crypto wallet isn’t just about picking a secure one. You also need to keep your private keys safe. If you lose your private key or it gets stolen, you lose access to your crypto forever. This can be a big issue for those unfamiliar with digital security. Securing and backing up your keys can be confusing, and storing them in insecure places can lead to a security breach. Any mistake with this can lead to permanent loss of funds, adding to the complexity of using cryptocurrency.

Using DeFi platforms and understanding cryptocurrency systems require a certain level of knowledge about blockchain technology and cryptography. For someone without a technical background, terms like “liquidity pools,” “slippage,” and “gas fees” can feel overwhelming. Platforms like decentralized exchanges (DEXs) require users to grasp these concepts to trade effectively, but for many, these ideas are not easy to understand.

Volatility and Security Risks

Cryptocurrencies are highly volatile, meaning their prices can change dramatically in a very short time. This makes crypto less reliable as a store of value, especially for users who want stability in their financial assets. For example, the value of Bitcoin or Ethereum can drop by 10% or more in just a few hours, which can be devastating for people who rely on crypto as their main source of money.

Along with this price volatility, there are also security risks. Since the cryptocurrency space lacks strong consumer protection, users are more vulnerable to scams and hacks. New users, in particular, are at risk of falling for phishing attacks, Ponzi schemes, and fake investment opportunities. These frauds often trick people who are unfamiliar with the space, causing them to lose their funds. Without knowing how to spot these threats, newcomers can easily become victims of malicious actors in the crypto world.

Who Benefits Most from Crypto?

When assessing who benefits most from crypto and DeFi, Individuals with a strong understanding of blockchain technology and the financial markets tend to have an edge. These individuals are often early adopters or those with the ability to understand complex concepts like smart contracts, liquidity provision, and yield farming, which can be lucrative but require a significant degree of expertise. Moreover, those who already possess capital, whether through traditional means or accumulated from crypto investments, are better positioned to navigate the space. They can take advantage of staking opportunities, trade on decentralized exchanges, and invest in DeFi projects, reaping the rewards of their early participation and larger portfolios.

On the flip side, for the underbanked and financially marginalized groups, significant barriers to entry exist. While blockchain technology and crypto offer promising opportunities for financial inclusion, the reality is that a large portion of the global population still lacks the necessary resources and infrastructure to participate fully in these markets. For example, while mobile wallets and cryptocurrencies can bypass traditional banking infrastructure, regulatory concerns, digital literacy, and access to stable internet remain significant challenges.

While the crypto markets have the potential to benefit all individuals, significant work is still needed to ensure they are accessible to everyone, especially the underbanked. The focus on usability and lowering costs could be pivotal in making crypto a true tool for financial inclusion, though this will require ongoing collaboration across the industry and regulatory bodies.

Final Thoughts

As we look toward the future of crypto and decentralized finance (DeFi), one key question remains: Can these innovations evolve to become accessible enough for everyone, or will they remain tools primarily for those with technical knowledge and financial resources?

For crypto to truly fulfil its promise of financial inclusion, several changes are needed. Lowering transaction fees, simplifying user interfaces, and improving education around blockchain technology are just a few steps in the right direction. Additionally, addressing security concerns and offering services that cater specifically to underserved communities could make crypto a viable option for the unbanked and those in developing regions. Partnerships between crypto projects, governments, and nonprofits will also be crucial in bridging the digital divide and ensuring that the benefits of DeFi reach all corners of society.

Ultimately, the evolution of crypto and DeFi will depend on the industry’s ability to balance innovation with inclusivity. Can the blockchain space simplify enough to allow everyday users to participate? Or will crypto remain a space where only the technically savvy and financially privileged thrive? It’s up to the community, developers, and regulators to determine how these systems can evolve to meet the needs of the global population.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

If you would like to read more market analyses like this, visit DeFi Planet and follow us on Twitter, LinkedIn, Facebook, Instagram, and CoinMarketCap Community.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

{kind=link}

{kind=link}